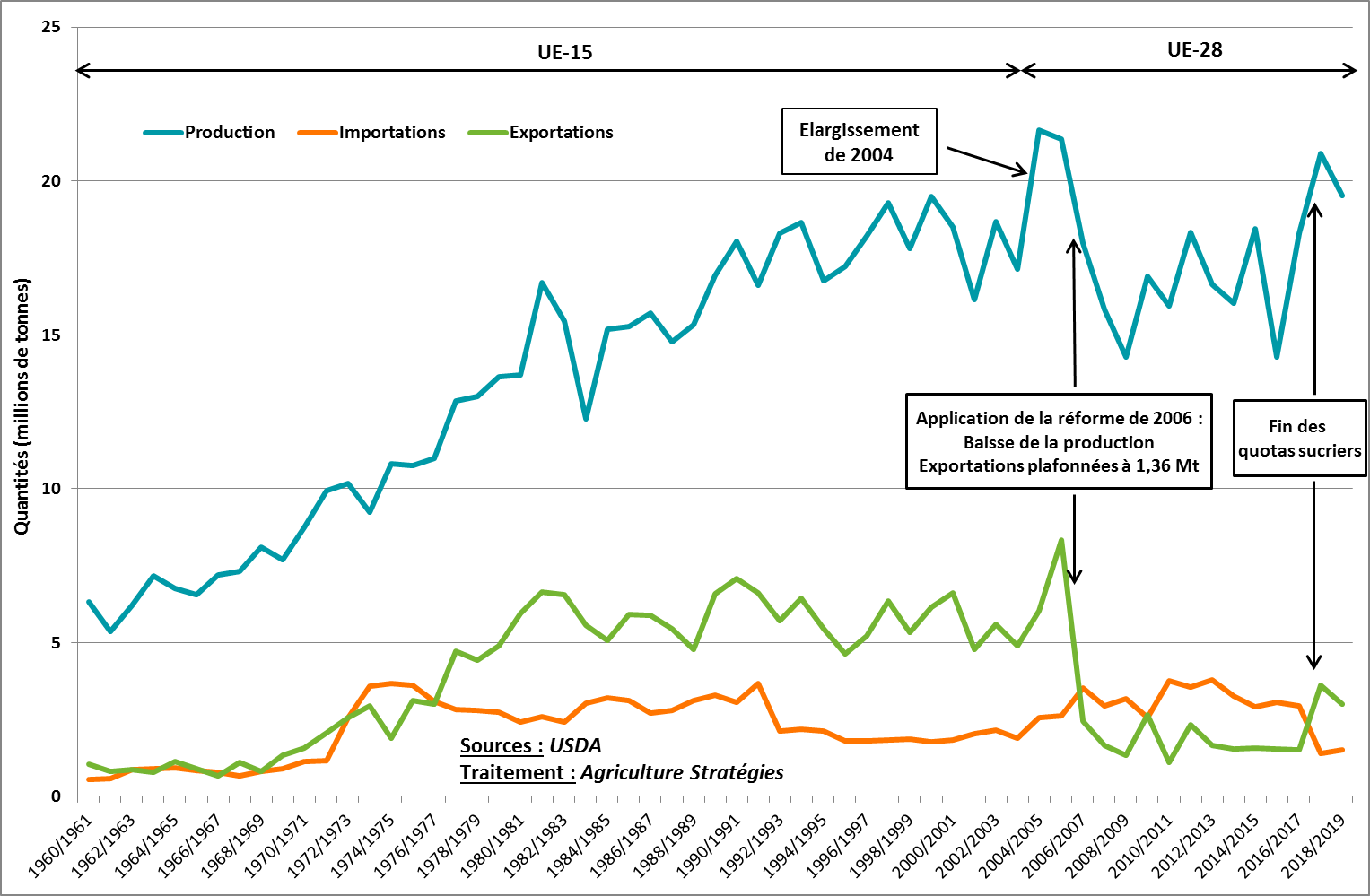

The abolition of the European sugar quota regime in 2017 did not have the expected results. The prospect of increasing European production to develop exports quickly turned into a drop in sugar prices and tensions in the governance of the sector, particularly in France. Heavy industry par excellence considering the transformation process, where the perishability and the heavy nature of the raw material explain the strong dependence between the links of the production and the first transformation, this sector also does not have important margins of maneuver to build a strategy of upmarket and “decommoditization”.

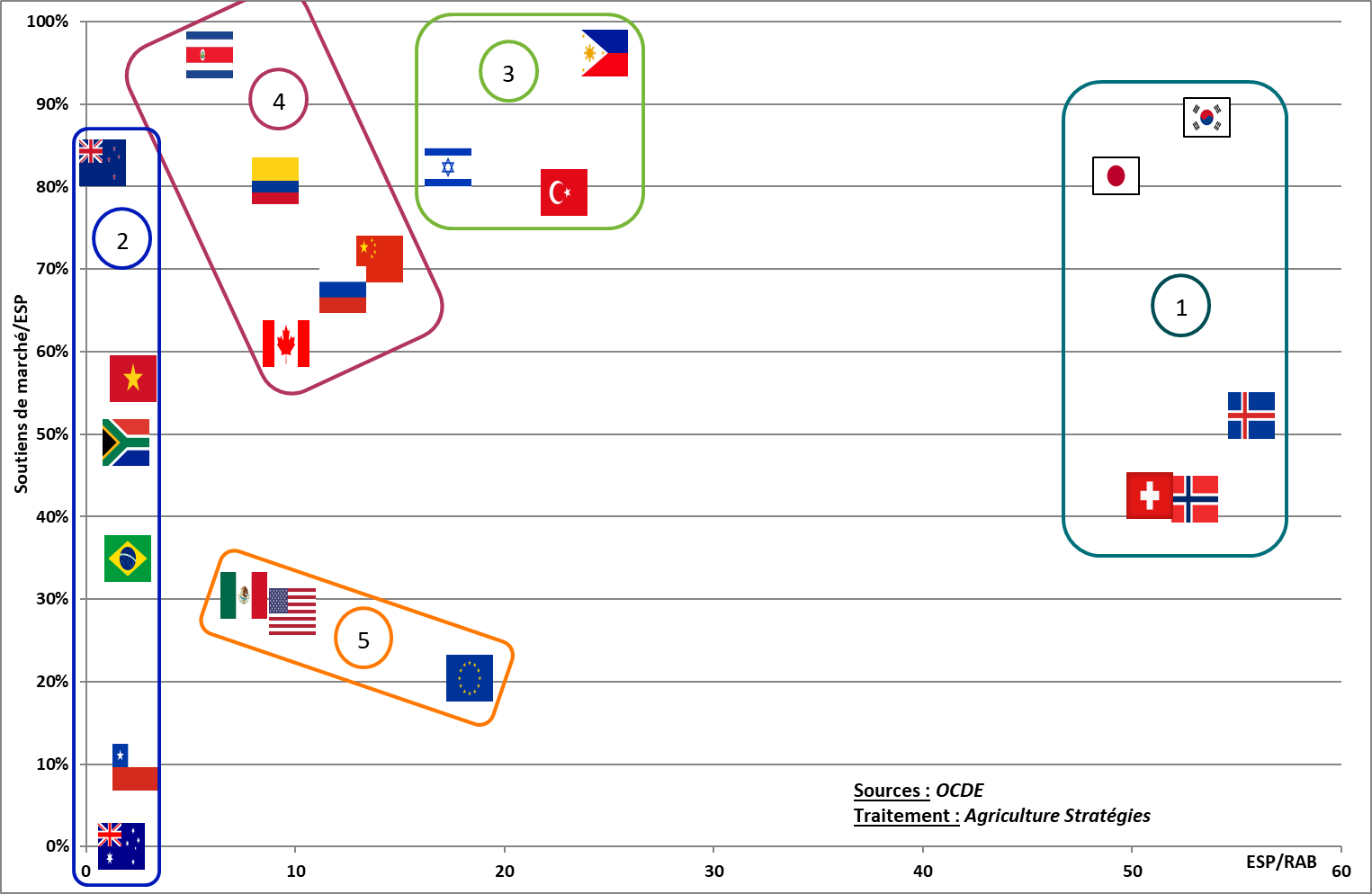

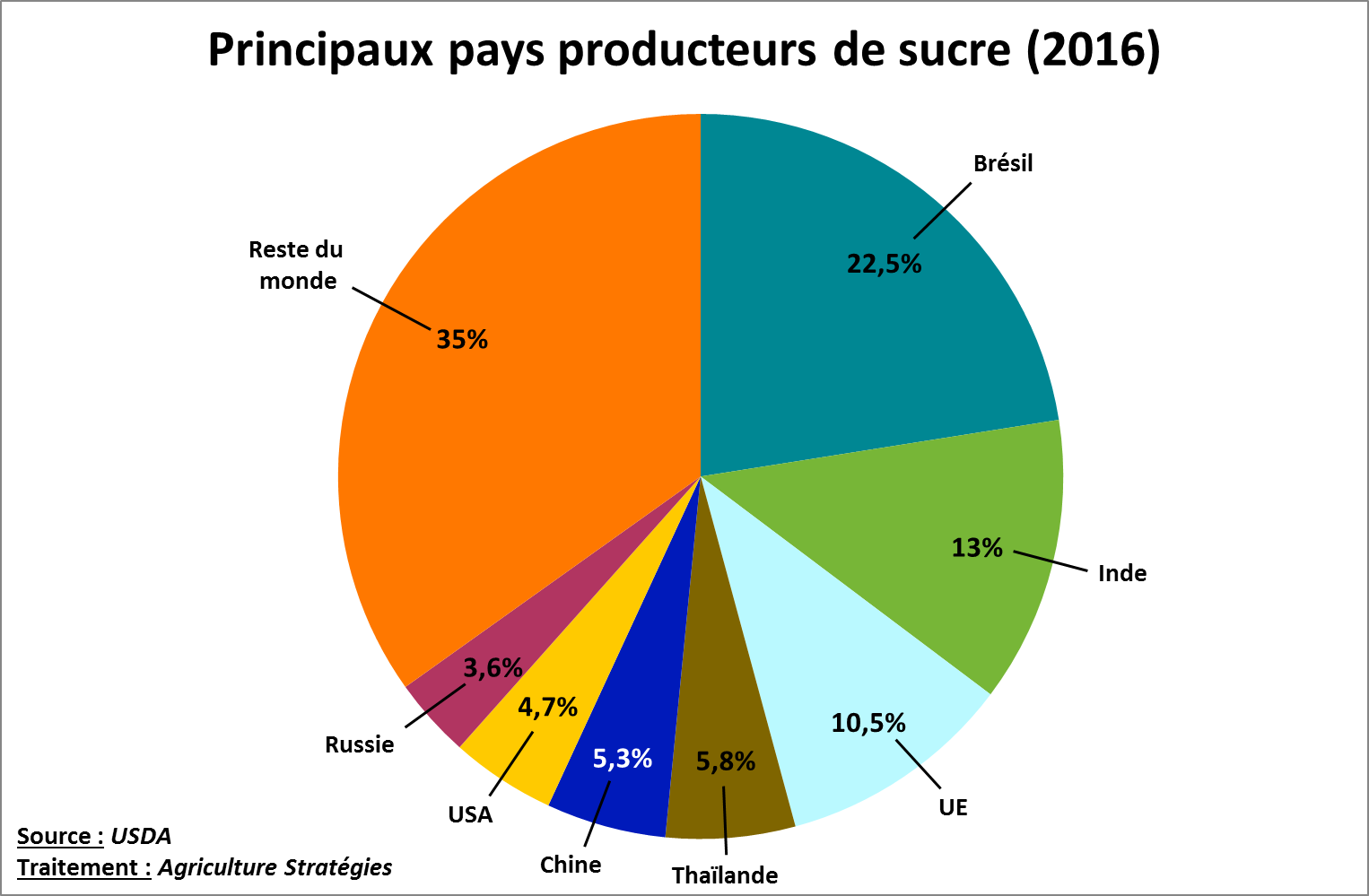

In these conditions, the exposure to the volatility of international markets, where the surpluses of the main producers are mainly exchanged, can undermine the entire sector because of a lack of strong public policy. In order to envisage a new regulatory framework for European sugar production, we propose a series of articles to study the different sugar policies of the main sugar producers. We will focus on Brazil, India, Thailand, China, the United States and Russia, which together with the European Union account for nearly two-thirds of world production (see Figure below). ). This panorama will allow us to conclude this series by constructing different scenarios of evolution of the European sugar policy.

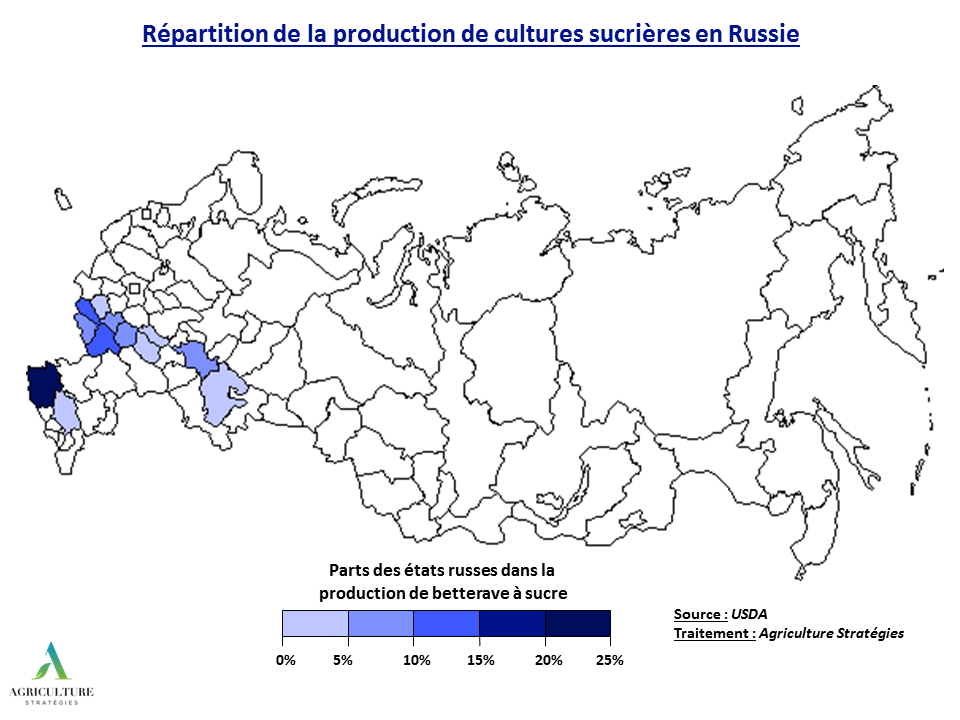

Russia is currently the world’s seventh largest sugar producer with about 6.2 million tonnes or 3.6% of world production in 2016. This production comes from the cultivation of sugar beets, whose production is located in the west of the country (Figure 1). Production is particularly important in the extreme south-west of the country and the Krasnodar region (20.6% of production)1. The sector is highly integrated: agro-holdings, a legacy of former Soviet collective farms, account for 89% of sugar beet acreage in Russia2 and more or less directly control processing units.

Figure 1: Distribution of sugar production in Russia

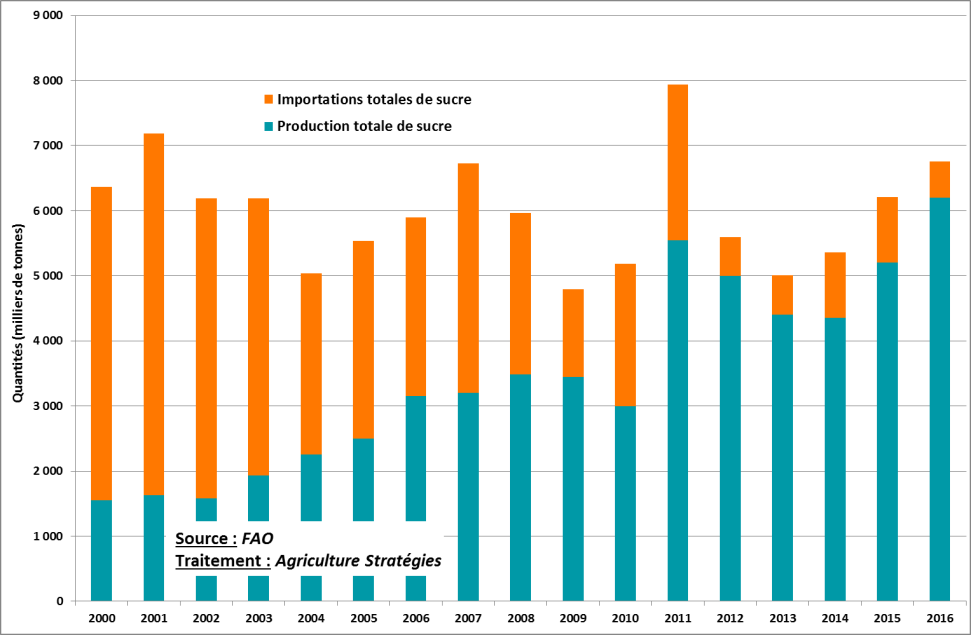

The sugar sector in Russia is currently experiencing a renaissance after a major decline. FAO statistics show a substantial production under the communist era: the USSR produced up to 69 million tons of sugar in the 1960s (almost a third of world production!). In 1993, Russian production was only 25 million tonnes (9.0% of world production) before reaching bottom in the early 2000s with only 1.5 million tonnes of sugar (1.2% of world production).

As shown in Figure 2, the sector seems to rise from the ashes under the impulse of a strong political strategy concerning all agricultural productions (for a detailed analysis see the article by Quentin Mathieu and Thierry Pouch in the journal Economie Rurale3). Indeed, from the mid-2000s, agriculture was established as a national priority, and following the 2008 food crisis, this priority was translated into political action with the “food security doctrine” adopted by decree in 2010 that sets self-sufficiency targets for all agricultural products4. Thus, for the sugar sector, a goal of 80% self-sufficiency was targeted for 2020, and has already been achieved: in 2016 less than 10% of Russian sugar was imported.

For the sugar sector, a $ 840 million program named “Development of the Sugar Complex of the Russian Federation for 2013-2015” was adopted in 2013 to support processors by providing assistance in the form of loans with a subsidized rate of interest5.

Figure 2: Evolution of sugar production and imports in Russia

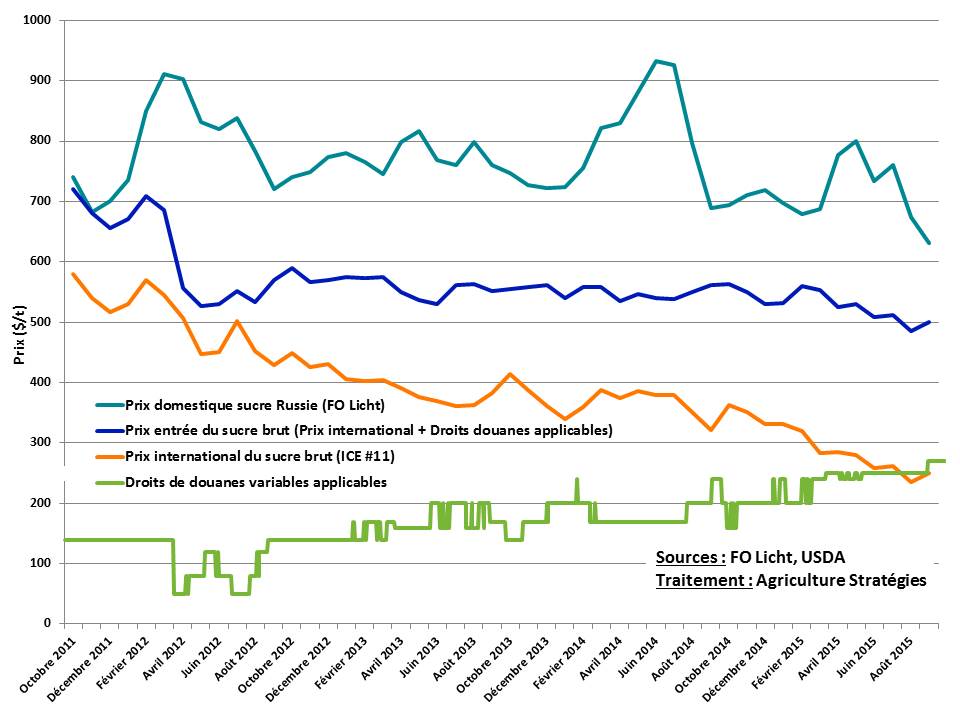

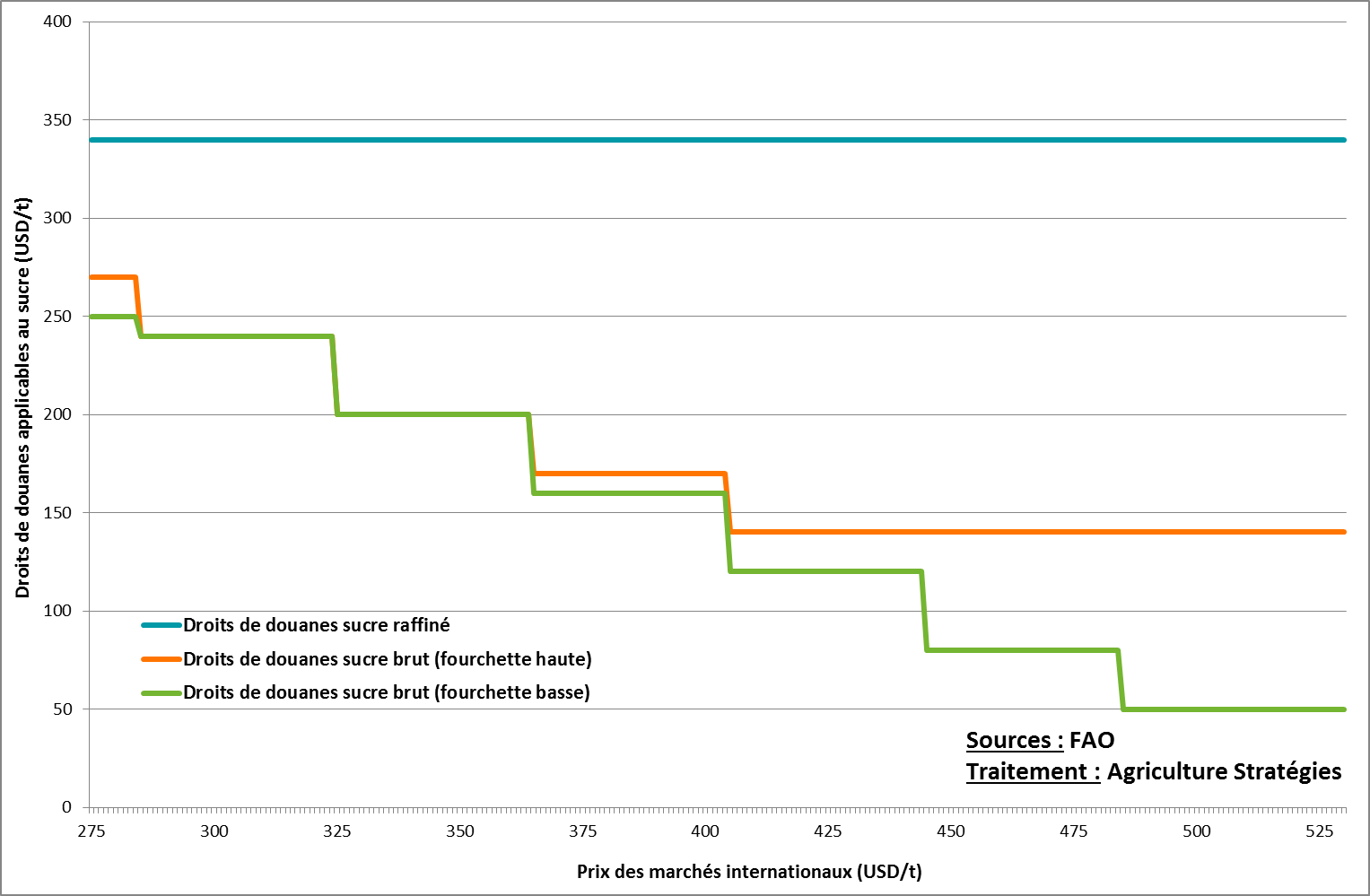

Beyond investment aid, it is mainly border protection that has allowed Russia to operate a real import substitution strategy. For sugar, tariffs are steered in such a way as to stabilize domestic prices at a sufficiently profitable level to encourage the development of production. Thus, refined sugar is taxed at an almost prohibitive level of $ 340 / t. Imports therefore take the form of raw sugar which is refined on the Russian territory. They are taxed at a rate that varies with the price of international trade: when international prices are high, taxes are reduced, and vice versa (Figure 3).

Figure 3: Variable customs tariffs for sugar entering Russian territory

During marketing periods (from 1 August and until stocks are considered low), tariffs range from $ 140 to $ 270 per tonne (high range). On the other hand, when imports are deemed necessary, a low range of between $ 50 and $ 250 per tonne is applied. Independent producers benefit directly from domestic price regulation because sugar factories are required to buy sugar beet at a price equivalent to 8% of the final processed sugar price6.

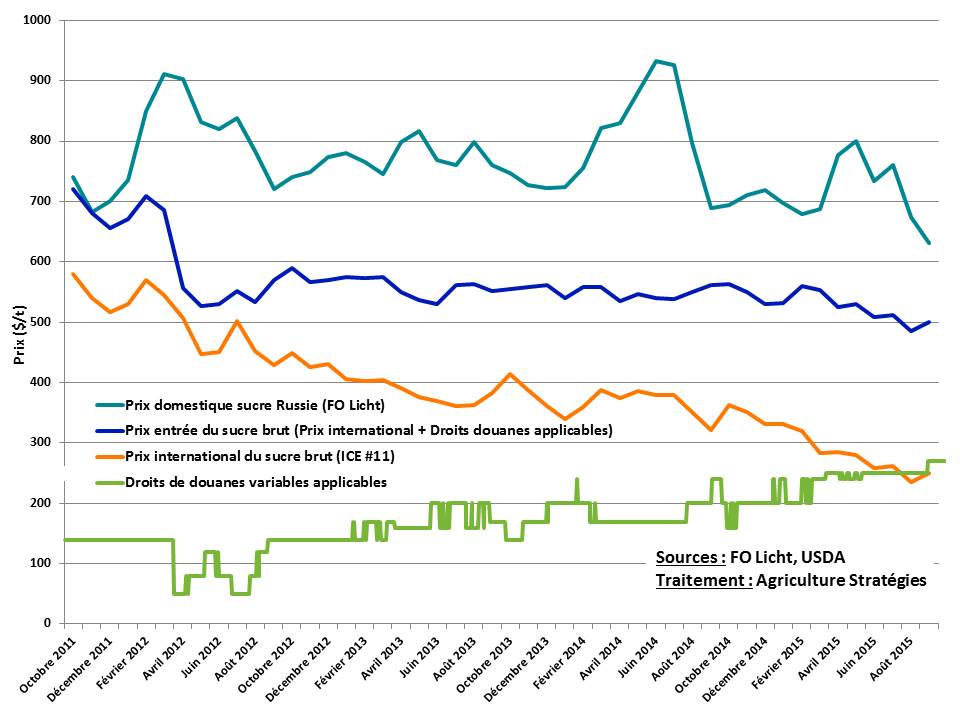

Figure 4 below gives an overview of the mechanics of variable customs duties over the period 2011-2015 during which the international price fell (orange curve). Under the assumption that the low range of rates is applied from April, the price curve for raw sugar raised with customs duties is established (transport costs should also be taken into account). Knowing that the cost of refining sugar is between $ 80 and $ 100 / tonne, it is explained that the domestic price of refined sugar in the Russian market is significantly higher than the international price.

Figure 4: Sugar prices in Russia, entering the territory and the international market

In the end, it appears that Russia’s sugar policy has boosted production to a record low in the early 2000s. Based on an import substitution strategy, changes may be coming as the Russian market is saturated. Given the Russian potential, it is not excluded that Russia will again become an exporter in the coming years.

Christopher Gaudoin, Strategic analyst for Agriculture Strategies

1 https://gain.fas.usda.gov/Recent%20GAIN%20Publications/Sugar%20Annual_Moscow_Russian%20Federation_4-19-2018.pdf

2 Source Rosstat : http://www.gks.ru/wps/wcm/connect/rosstat_main/rosstat/en/figures/agriculture/

3 Mathieu Q., Pouch T., (2018), « Russie : un retour réussi sur la scène agricole mondiale Des années 1990 à l’embargo », in Economie Rurale, 365, p.103-118

4 https://www.agriculture-strategies.eu/2018/01/la-resorption-du-deficit-commercial-agro-alimentaire-russe-consequence-de-lembargo-sur-les-produits-agricoles-europeens/

5 https://gain.fas.usda.gov/Recent%20GAIN%20Publications/Sugar%20Annual_Moscow_Russian%20Federation_4-14-2017.pdf