The abolition of the European sugar quota regime in 2017 did not have the expected results. The prospect of increasing European production to develop exports quickly turned into a drop in sugar prices and tensions in the governance of the sector, particularly in France. Heavy industry par excellence considering the transformation process, where the perishability and the heavy nature of the raw material explain the strong dependence between the links of the production and the first transformation, this sector also does not have important margins of maneuver to build a strategy of upmarket and “decommoditization”.

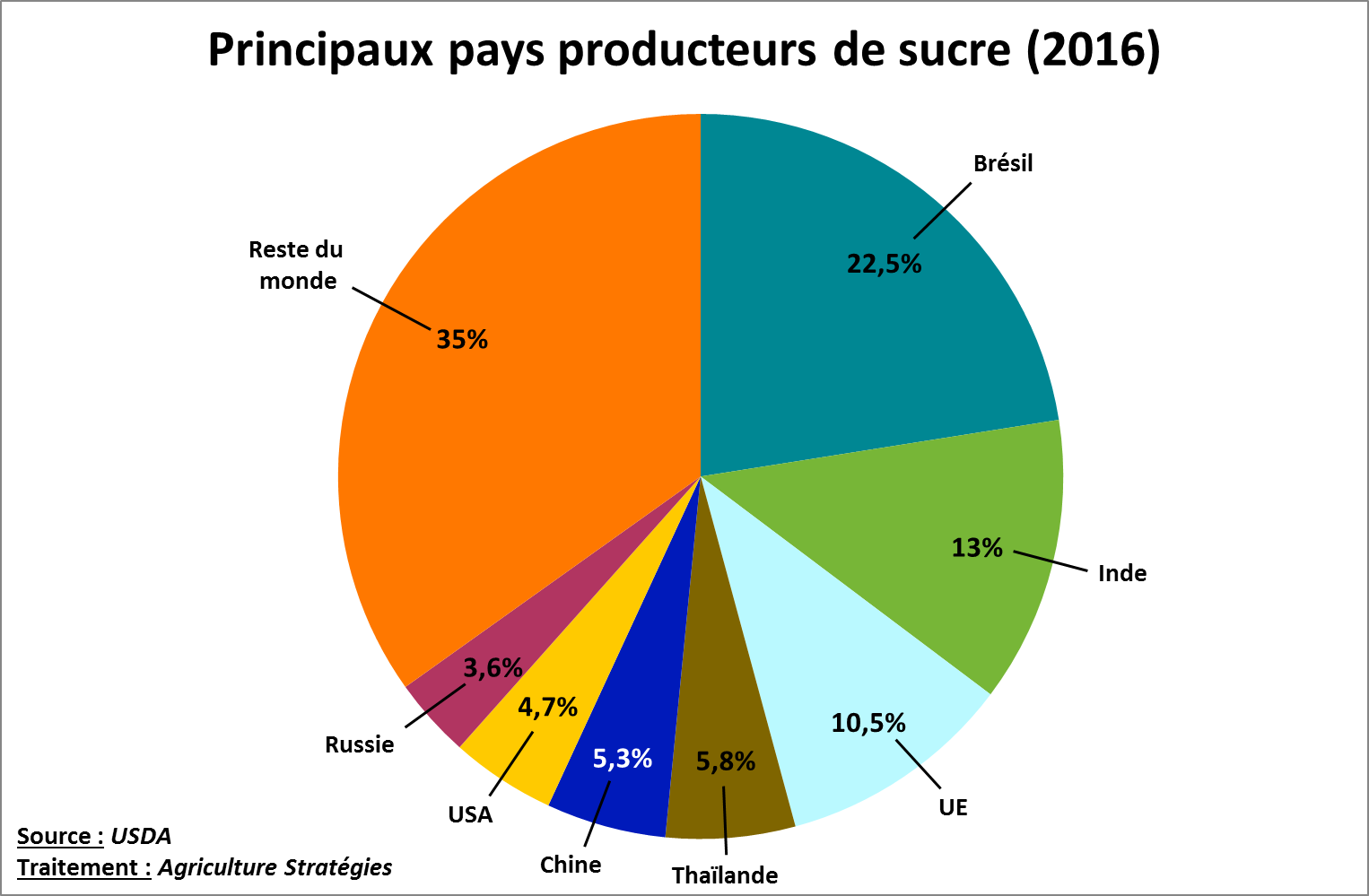

In these conditions, the exposure to the volatility of international markets, where the surpluses of the main producers are mainly exchanged, can undermine the entire sector because of a lack of strong public policy. In order to envisage a new regulatory framework for European sugar production, we propose a series of articles to study the different sugar policies of the main sugar producers. We will focus on Brazil, India, Thailand, China, the United States and Russia, which together with the European Union account for nearly two-thirds of world production (see Figure below). ). This panorama will allow us to conclude this series by constructing different scenarios of evolution of the European sugar policy.

Find in our series on sugar policies in the world our focus on: