Despite the high hopes placed in them since the end of milk quotas, European dairy futures markets struggle to develop. The sharp drop in activity observed on Leipzig EEX’s dairy contracts since early 2018 could be a sign of a fatal loss of trust that may lead to the abandonment of the contract. One cannot just decide to launch of a futures market and there are certain conditions that need to be respected for its proper functioning. Lack of connection with real markets and use of price references directly stemming from historic actors of the sector can be considered as important brakes for new actors susceptible of bringing the liquidity needed. In spite of the recommendations of the Task Force on the functioning of markets, the Commission has not yet taken initiatives to improve the transparency of the dairy products markets. Also, thresholds imposing the publication of reports by categories of actors which just have been implemented thanks to the reform of the financial directives (Mifid2) are too high and do not supply the minimal transparency. If the futures markets of milk powder and butter are not helpful at all in case of durably depressed markets and in case of failing milk price formation, their development would nevertheless allow improvement in the global functioning of the sector. That’s why increasing transparency of these markets is an absolute necessity.

The markets of butter and milk powder have been making the news for two years, the first one reaching summits while the second was at its lowest. This unprecedented difference makes us wonder about the role of futures markets in the price formation of these products. Contrary to the various attempts of Euronext which ended in failures1, the contracts of the stock exchange EEX (European Energy Exchange) of Leipzig saw their activity grow since 2014. Following previous analysis2, we study in this article the activity of these two contracts and look for teachings as to the conditions of their sustainability and their utility as risk management tools.

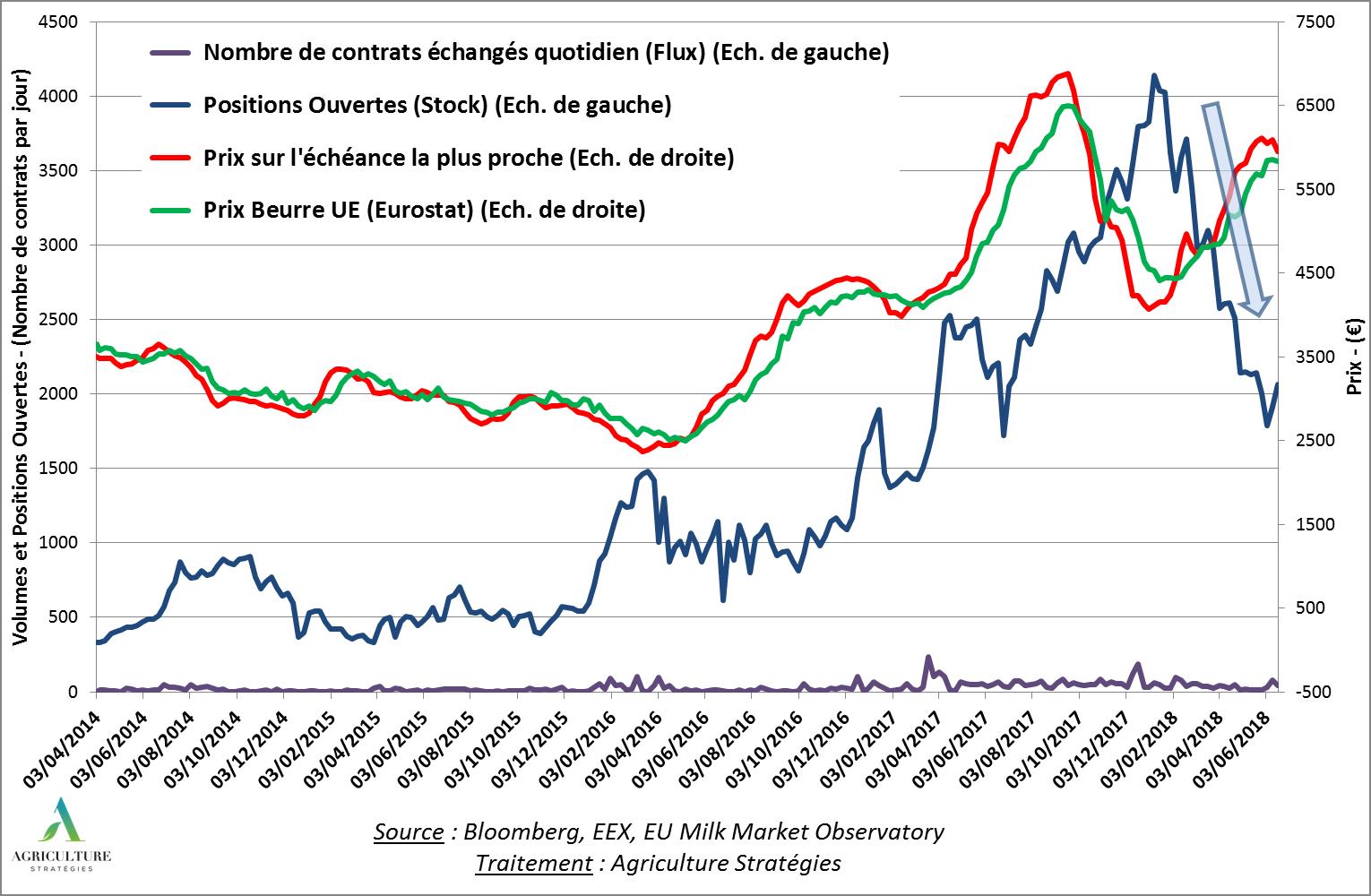

A marked reduction in the opened interests since December 2017

Figure 1

Figure 1 above represents the main information relative to contracts on butter: the very low flow of daily exchanges (27 contracts per day on average) and the number of opened interests (the stock) are associated on the left scale; the price of the closest term of contracts as well as the official European butter quotation are to be read from the right scale.

We can see an acceleration of the stock of contracts (“open interests”) from spring 2016 when we count near 1000 contracts, until December 2017 when they exceed 4100 contracts. At the same time, the prices of butter went slightly up with a sensitive increase from 2500€/ton to more than 6500€/t. The price drop that began in September 2017 is as strong as the increase which preceeded it, but since February 2018 a bounce can be observed. Regarding the number of contracts in stock, a maximum was reached 3 months after the summit of prices and since the number of contracts is in free-fall going from more than 4000 to 2000 within 6 months.

Figure 2

For milk powder (figure 2), the rise in importance of open positions was more sudden before reaching a ceiling of approximately 3840 contracts in March 2017. Since then, contracts stocks have been halved with no more than 1700 contracts in March 2018, before starting to bounce again over the last months. The prices profile is completely different from the butter one: they stayed at a relatively stable and low level, around the level of European intervention price, mostly because powder stocks were accumulated during the crisis consecutive to the end of dairy quotas.

For both butter and powder, a number of open contracts experienced an important decrease since the beginning of 2018. However, even at their highest, it represented only a fraction of the European production: for 5 ton contracts, butter and milk powder committed in the stock exchange of Leipzig represented only approximately 100 000t and 33 000t of milk equivalent respectively, which is the equal to 0,08 % of the annual European dairy production. The reduction in the number of contracts cannot find an explanation in the evolution of production. On the contrary, knowing that the quotation of Leipzig is based on a fraction of the European production, we can legitimately wonder about his representativeness and its place in the price formation.

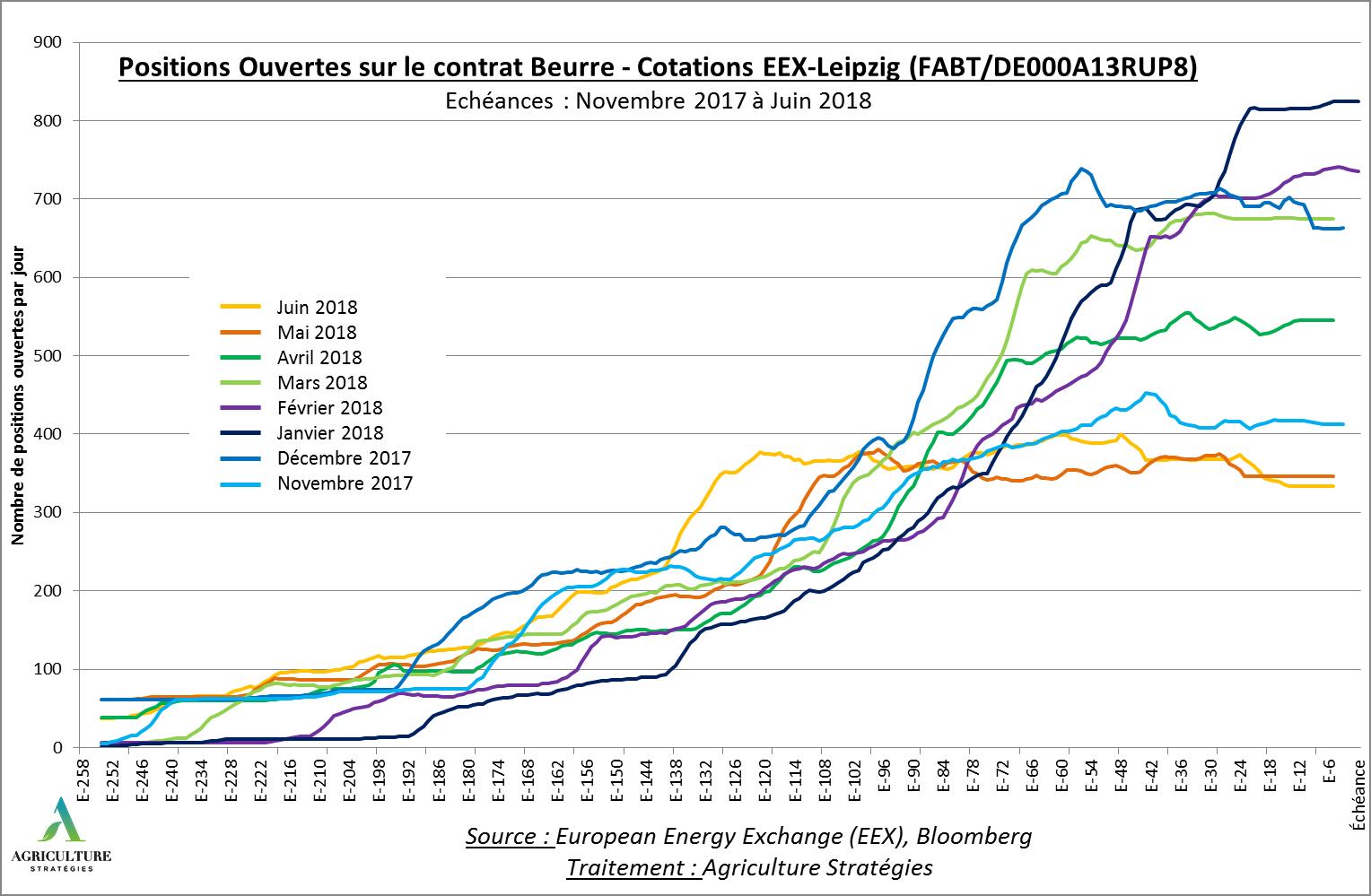

Contracts which all run until term

Figure 3

To characterize the reduction in the open positions, it is useful to look at the evolution of open interests for each of the contracts that have reached their term. The figure 3 represents the number of contracts for the last 8 terms, from November 2017 until June 2018. Two elements can be highlighted: on one hand, the more recent the contract is, the more early and at a low level it reaches a ceiling; on the other hand, the number of contracts does not decrease at the approach of term. The reduction in the number of opened positions observed since the end of 2017 explains logically the first evolution. However, the absence of reduction in the number of contracts before the term characterizes a completely abnormal usage coming from actors on raw materials futures markets.

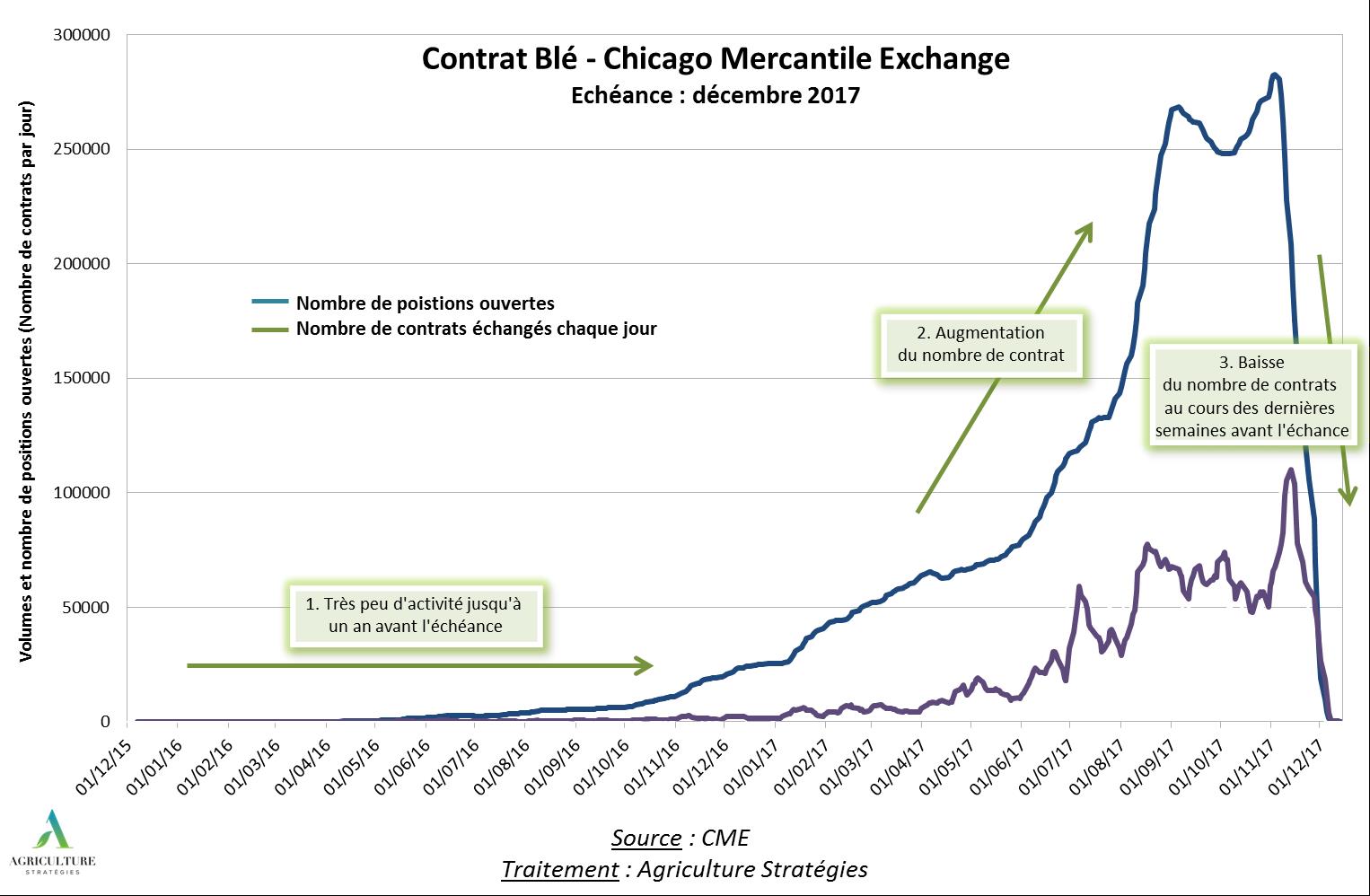

Figure 4

Indeed, as represented in figure 4 for wheat contracts in Chicago (SRW-CME), the number of opened positions normally has two phases: a phase of growth where the economic players take a stand to cover themselves by positioning in purchase or in sale, and then a phase of decrease where they are going to unbuckle their position in order to register the earnings or losses induced by price changes. So when due, contracts stock is almost nil which means that a much reduced number of actors chooses to operate a physical delivery of wheat. Furthermore, as shown in figure 4, the number of exchanged contracts every day (the flow) is relatively important compared with the number of opened positions (the stock). For wheat contracts, ratio is 1 to 5, which characterizes a market with high liquidity where contracts are unbuckled regularly.

Let’s go back to Leipzig contracts. Besides the very low liquidity (less than about thirty contracts a day), another peculiarity allows us to understand why most of the contracts run until term: they are contracts which’s release is done in cash and not in nature like the Chicago wheat contracts for example. So, this link with the real economy which allows payment in nature does not exist anymore and the release of the contract is cash settlement.

It has two main consequences:

- On one hand, the contract cash settlement is based on a reference quotation which must be undisputable so that actors keep their confidence in the contract capacity to reflect the economic reality of the market. And, in this case, quotation used as reference for dairy products does not rest on a system of centralized reporting but on information provided by traders and collected by the dairy industry itself.

- On the other hand, unbuckling before term offers more information in price formation, because every actor operates two decisions, that to take a stand and that to liquidate his position.

In the end, if cash settlement contracts are supposedly more attractive for institutional investors, we have to admit that it is not the case. And conversely we can think that the absence of link with the physical market using delivery in nature can be considered as an additional uncertainty for new participants who would face with actors’ better mastering of the fundamentals of dairy products markets.

What should we draw from this ?

While the futures markets are potentially useful tools to run against a regular volatility around production costs, Leipzig dairy products contracts seem dedicated to disappear in the short run if the confidence in their proper functionning is not restored.

Indeed, reduction in opened positions (contracts stock) and collapse of the number of exchanged contracts every day (the flow) indicates a loss of trust. Launching and perpetuating a futures market cannot be just decided and certain conditions must be respected for its smooth functionning.

Deficiencies in terms of transparency in dairy products exchanges are the main factor. As we indicated previously, wanting to launch a futures market without improving the transparency of linked physical markets is to put the cart before the horse3. In these conditions, where the quality of quotations raise numerous questions among which possible interference phenomena where both prices –physical and financial- feed each other in increasing or decreasing, the possibility of a physical delivery is likely to reassure the actors.

Task Force’s report on the agricultural markets functioning had well identified this subject and pleaded in its recommendations for an improvement of dairy products quotations in particular4. But the European Commission, nevertheless initiator of this report, did not yet impose changes on dairy industry practices to improve transparency.

Finally, trends in butter and powder contracts observed in 2017 would have probably suffered from the lack of information about the stock exchange itself. On very specific markets where industrial actors have information connected to their activity, it is risky to commit for financial actors even though they are promoters of a better liquidity. And, in this particular case, if recently reformed financial directives aimed to increase information on actors on markets, weekly activity reports by actors categories thresholds (Commitment of Traders) are too high for developing markets to be concerned. Indeed, there have to have more than 20 actors involved on the contract at the same time and open positions have to represent more than 4 times the volume of underlying market so that these reports are made public.

Like a snake biting its tail, low transparency on small markets while launching does not enable a better trust allowing actors to try it … which strongly limits their development! The possibility of physical deliveries when due and reduction in categories of actors reports (Commitment of Traders) threshold would help restoring their attractiveness and incite participation of new actors. If the futures markets of powder and butter are not helpful at all in case of durably depressed markets and in case of failing price formation of milk, their development would nevertheless allow improvement in the global functioning of the sector.

Frédéric Courleux, Director of studies for Agriculture Strategies

Christopher Gaudoin, Strategic analyst for Agriculture Strategies

1 Après un premier échec sur une série de contrats lancée en 2010, les contrats Euronext sur produits laitiers initiés en 2015 sont au point mort et devraient logiquement être bientôt arrêtés.

2 Cf. https://www.agriculture-strategies.eu/2018/01/les-marches-a-terme-et-les-assurances-revenus-ne-sont-pas-des-substituts-aux-regulations-publiques-3-3/ et https://www.agriculture-strategies.eu/2018/01/les-vraies-causes-du-desequilibre-des-marches-des-produits-laitiers/

3 https://www.agriculture-strategies.eu/2018/01/les-marches-a-terme-et-les-assurances-revenus-ne-sont-pas-des-substituts-aux-regulations-publiques-3-3/

4 https://ec.europa.eu/agriculture/sites/agriculture/files/agri-markets-task-force/improving-markets-outcomes_en.pdf, cf. page 18