Download article (PDF)

Nearly four years after Russia’s invasion of Ukraine on 24 February 2022, agricultural commodities have asserted themselves more than ever as explicit instruments of power. By reshaping export routes, disrupting logistical chains and placing some of the world’s largest food importers in a situation of vulnerability, the conflict has revealed and accelerated a structural transformation of global agricultural trade.

As early as June 2023, Agriculture Stratégies analysed the first “cascade reconfigurations” generated by the war for global food security[1]. A little more than two years later, the conflict has stalled and food-related issues remain at the centre of concerns: the Kremlin has continued its strategy of weaponising agricultural commodities, notably by methodically targeting Ukraine’s export infrastructure. In this context, Africa, which is highly dependent on imports of Russian and Ukrainian grain and is facing a rise in food insecurity, has become a field of diplomatic and food competition. This article proposes to look back at four years of evolution of the conflict’s “food front” in Ukraine, and to explore its consequences for some of the world’s largest import-dependent countries.

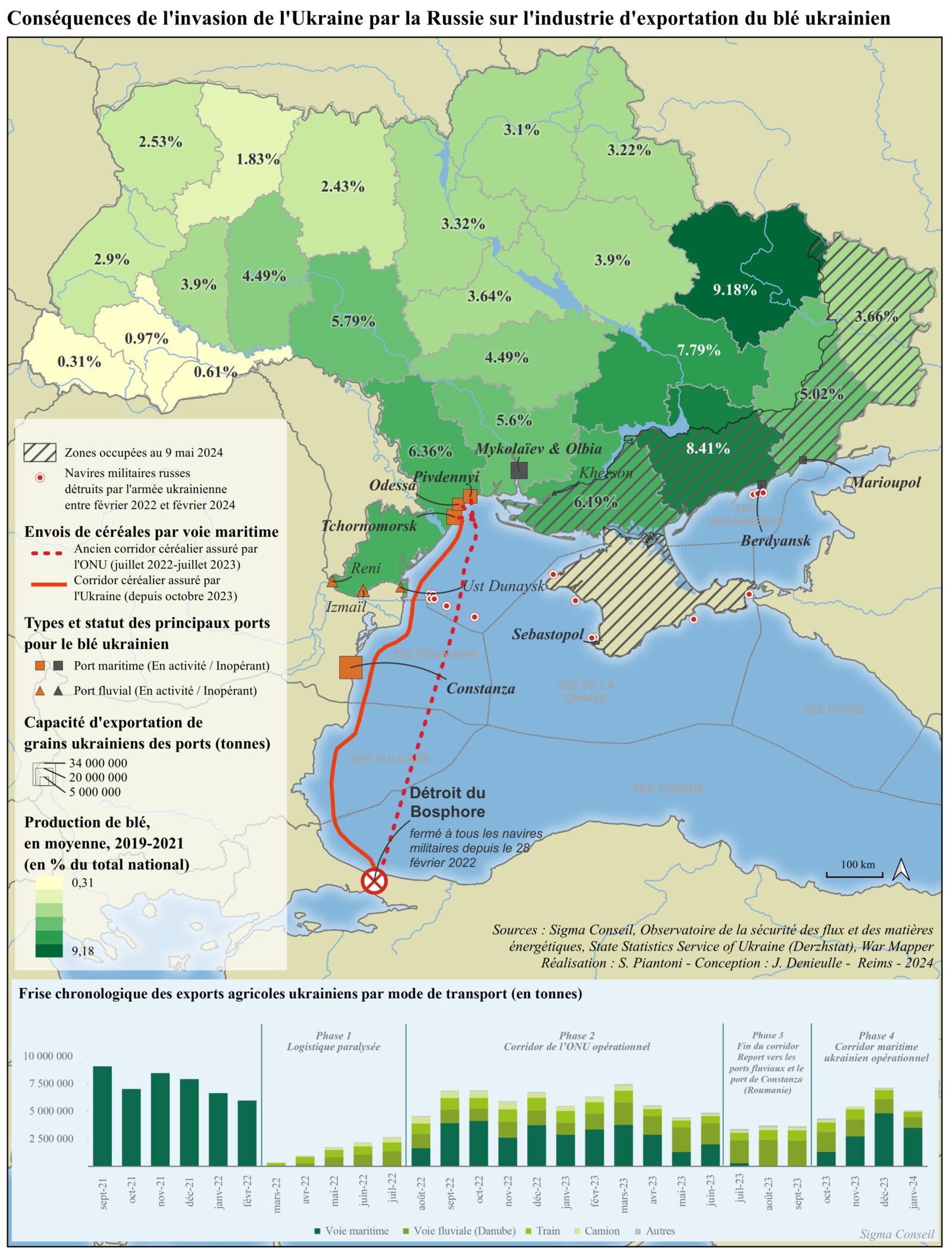

Map 1 : Consequences of Russia’s invasion of Ukraine on the Ukrainian wheat export industry. Realisation : S. Piantoni – Conception : J. Denieulle, 2024

Food as a Battlefield: Chaos, Adaptation and Workarounds

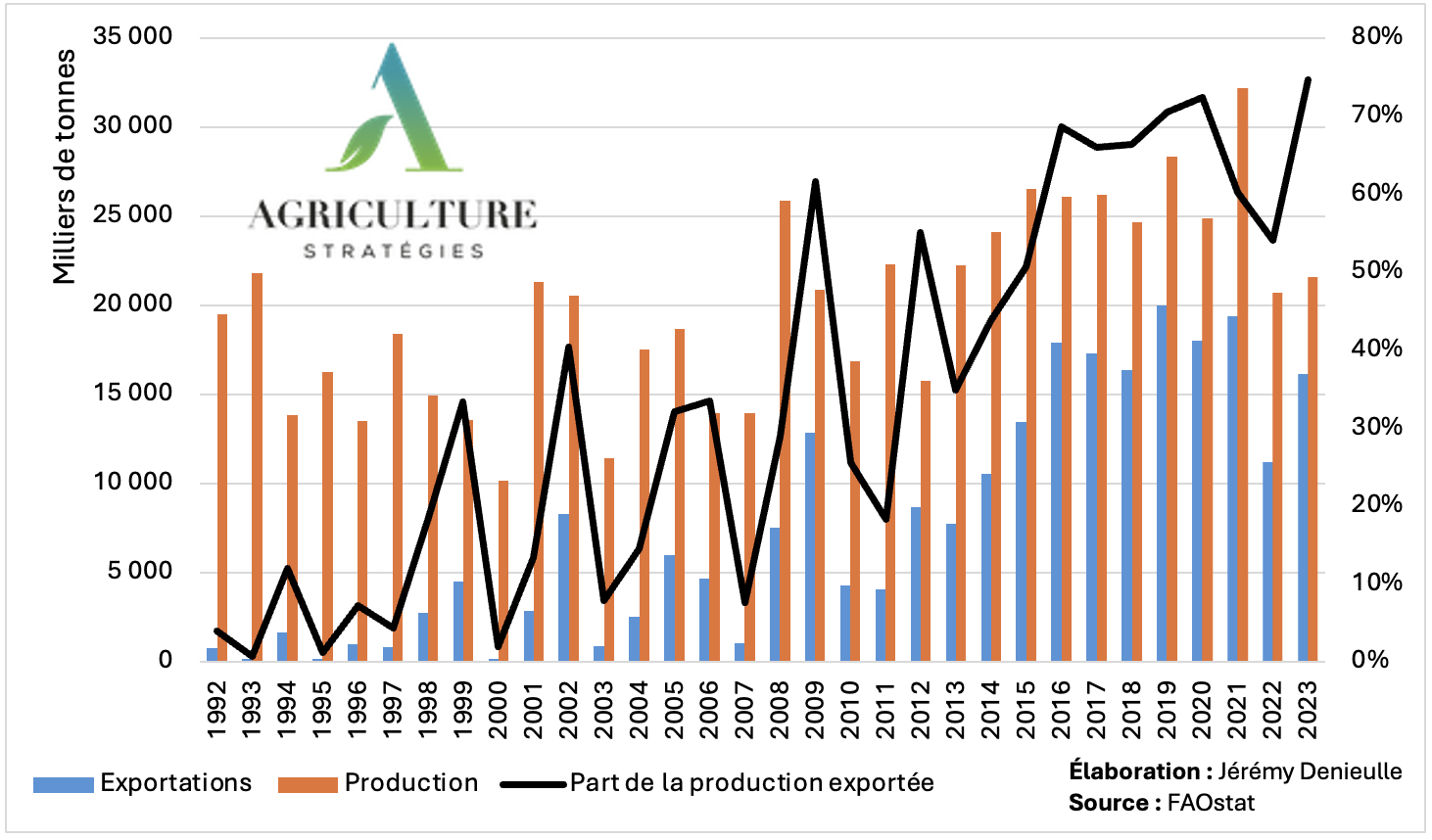

During Russia’s large-scale invasion of Ukraine in February 2022[2], beyond the military dimension, a food front immediately emerged as well. Here, we will focus on the example of wheat, a commodity at the heart of global power (im)balances[3]. On the eve of the invasion in 2021, both Russia and Ukraine held a central position in international geoeconomic equilibria, together accounting for nearly one quarter of global wheat exports in volume (respectively 13.6% and 9.6%). For Ukraine, in the aftermath of its independence from the USSR (1991), the agricultural sector became one of the drivers of the country’s economic recovery as well as of its integration into globalisation. Largely export-oriented, Ukrainian agriculture accounted for 15% of national GDP and 20% of employment prior to the invasion. In this respect, the country also occupied a central place in international trade for numerous agricultural products (Table 1). For wheat in particular, in 2020 more than 70% of Ukrainian production was exported (notably to Egypt, the rest of North Africa, or Southeast Asia) (Figure 1).

Table 1 : Ukraine’s position in global agricultural exports (2018–2019, by value. Source: French-Ukrainian Chamber of Commerce and Industry[4]

| Products | Rank |

| Sunflower oil, sunflower meal | 1 |

| Rapeseed | 2 |

| Nuts | 3 |

| Maize, barley, rye, sorghum, honey | 4 |

| Wheat | 5 |

| Rapeseed meal, butter | 6 |

| Rapeseed oil, poultry meat, soybeans | 7 |

| Oats, milk, oil and soybean meal | 8 |

| Skimmed milk powder | 9 |

| Cheeses | 10 |

Figure 1: Evolution of Ukraine’s wheat production and exports (1992–2023)

To facilitate a chronological reading of events since February 2022, we can divide them into four successive phases:

- A first phase, at the very beginning of the conflict, in which Ukrainian port logistics were rendered completely inoperative (February 2022 to July 2022);

- A second phase marked by the establishment of the Black Sea Grain Initiative under UN auspices and with the participation of both belligerents (July 2022 to July 2023);

- A third phase corresponding to the end of this grain corridor and the blocking of Ukrainian ports for the second time (July 2023 to September 2023);

- Finally, a fourth phase marked by the establishment of a new grain corridor by Ukraine without Russian participation (since October 2023).

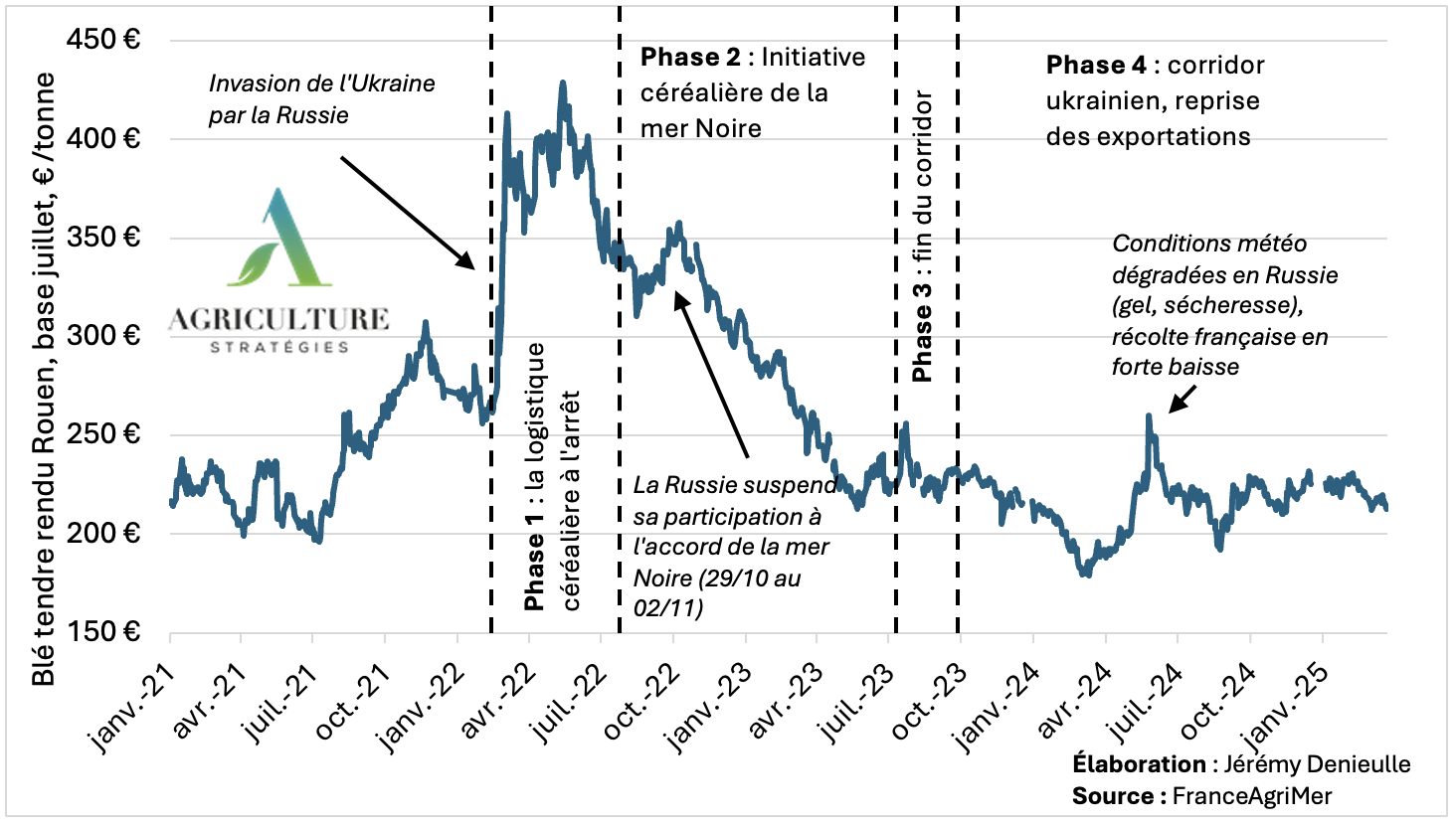

Control of the Black Sea is key: before the invasion, the entirety of Ukraine’s agricultural exports transited through this route, mainly via the ports of Mykolaiv and Olbia, Chornomorsk, Pivdennyi and Odessa (Map 1). Given the importance of the agro-export industry for the Ukrainian economy, and ultimately for its war effort, the first months of the conflict saw the Russian army methodically target agricultural infrastructure, paralyse the Black Sea ports[5] and carry out grain thefts that were then re-exported to allied countries (such as Bashar al-Assad’s Syria) via occupied Crimea[6]. Solutions were quickly sought in order to curb the inflation of commodity prices (Figure 2), such as the European solidarity corridors, which helped avoid a complete collapse of Ukrainian exports. But it was the establishment of the Black Sea Grain Initiative, from July 2022 onwards, that truly enabled the recovery of exports. It was also the only venue for direct exchange between the two belligerents since the invasion. In July 2023, after the Kremlin had repeatedly threatened to withdraw from the agreement in order to obtain relief from Western sanctions, the UN-brokered corridor finally came to an end. Since October 2023, and thanks to a shift in the military balance of power in the Black Sea in Ukraine’s favour, Kyiv has managed to secure its its own export corridor by sailing along the Romanian and Bulgarian coasts (Map 1).

Figure 2: Evolution of wheat prices (Rouen delivery) during the war in Ukraine (January 2021–March 2025)

These four sequences outline a common thread: since February 2022, agricultural logistics has become a central arena of strategic confrontation between Ukraine and Russia. These events reveal a war in which control over export routes matters just as much as, if not more than, control over territory. Beyond short-term fluctuations, one major lesson emerges: neither of the two belligerents can afford a total collapse of cereal flows. Russia uses its dominant position on global grain markets, and in particular on the wheat market, sometimes as an instrument of pressure (vis-à-vis Western countries) and sometimes as a tool of diplomacy (towards Africa, for instance, which is a major importer). Ukraine, despite weakened productive capacities, has on its side demonstrated its ability to adapt while also launching a diplomatic campaign focused on its agricultural exports – Grains from Ukraine[7].

After the Covid-19 crisis, the war once again revealed to what extent the security of supply — and ultimately the food security of regions most dependent on international trade — sometimes depends less on available volumes than on the ability to secure routes or to control logistical costs (in particular those related to the insurance of vessels and their cargo). The extreme price volatility observed after 2022 thus reflects the fragility of a globalised system in which a few corridors, in this case the Black Sea, concentrate a decisive share of commercial flows that are nonetheless essential for the sociopolitical stability of entire regions. In this context, the most import-dependent countries have seen their room for manoeuvre drastically reduced. Higher import costs, the unpredictability of the war and diplomatic tensions, heightened competition and the fragmentation of multilateralism have turned this shock into a structural crisis. Some African countries, whose food security relies heavily on wheat imports from the Black Sea, have found themselves on the front line of these reconfigurations since 2022.

African Vulnerabilities: Food Security Under Strain

In its 2025 edition of The State of Food Security and Nutrition in the World[8], the FAO notes that although global food insecurity declined between 2023 and 2024, Africa and Western Asia are the only two regions in which the number of people experiencing increased hunger. The reasons for this rise are obviously multiple and complex[9]. The FAO nevertheless identifies global food price inflation — driven since 2020 by the Covid-19 pandemic and then by the consequences of the war in Ukraine — as one of the main causes of the deterioration in food security.

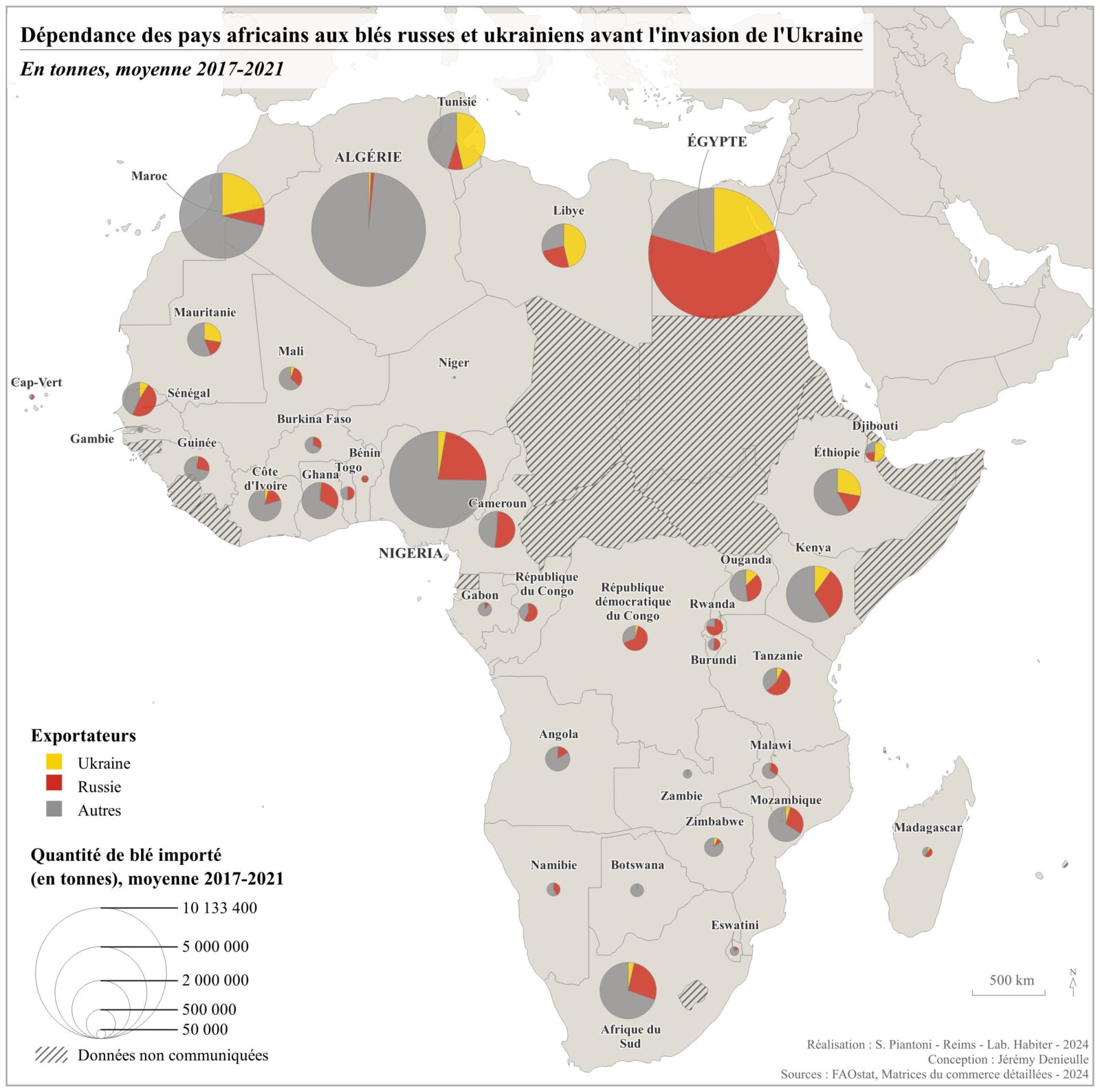

To better account for African vulnerabilities to the consequences of the war, it is useful to stay with the example of wheat. A first level of analysis therefore consists in observing the degree of dependence of each country on Russian and Ukrainian wheat before 2022. Map 2 thus highlights North Africa, which is a major wheat-importing region. In sub-Saharan Africa, although situations are more varied, Russian wheat has made inroads across the region over the past decade. It is important to stress, however, the considerable diversity of situations across the continent. Wheat-based products do not occupy the same central position in the diets of sub-Saharan African populations as they do in those of North Africa. In the latter region — the largest wheat-importing region in the world — bread is often at the heart of social contracts between populations and states. These states are moreover frequently directly involved in wheat imports and in the structuring of cereal value chains.

Map 2: Dependance of African countries on Russian and Ukrainian wheat before the invasion of Ukraine (tonnes, 2017-2021 averages). Realisation : S. Piantoni – Conception : J. Denieulle, 2024

This does not mean, however, that sub-Saharan African countries are not experiencing the food shock triggered by the war in Ukraine, particularly since the end of the Black Sea Grain Initiative[10].Even when wheat occupies a more marginal place in diets, as is the case in most countries south of the Sahara, the repercussions of the conflict have spread through other channels that are just as decisive.

The first of these is global prices, whose extreme volatility since 2022 has affected the entire subcontinent, already greatly weakened by the consequences of the Covid-19 pandemic. The war has caused a surge in logistical costs, an increase in maritime insurance premiums and, above all, a sharp rise in fertiliser prices — a crucial factor for sub-Saharan Africa, which relies heavily on fertiliser imports[11]. With Russia and Belarus together accounting for 37% of global potash trade and a substantial share of phosphate and nitrogen exports, disruptions in these markets have quickly been transmitted to African economies.

In Nigeria, for example, domestic prices of urea rose by more than 20% in 2022 while diesel, essential for the functioning of transport and agricultural operations, saw its price triple between 2022 and 2024. This increase in production costs has been passed on to food prices: food inflation exceeded 38% in 2024 and bread, although less central in Nigerian diets than rice or maize, saw its price rise by nearly 30% in 2022 alone[12]. Wheat also has a significant economic weight in Nigeria: the country covers almost all of its consumption through external purchases, which makes it one of its three main import expenditure items[13]. These purchases, whose volume has more than tripled since 2000, generate particularly heavy foreign-currency outflows for an economy that is structurally short of dollars.

In many East African economies, the rise in global prices has also led to an increase in the cost of the food basket: between January and May 2022, its average cost rose by 22%, and by more than 50% compared to the previous year. The dependence of these countries on global markets has thus acted as an amplifier, transforming an exogenous shock into a lasting crisis.

However, one must be careful not to read these vulnerabilities solely through the prism of economics or trade. As Pierre Blanc reminds us[14], exposure to food shocks depends as much on import data as on the capacity of states to absorb crises. Countries with significant budgetary margins, such as the Gulf States, can cushion the effects of price increases through massive subsidies. In North Africa, by contrast, several economies combine strong dependence on imported wheat, institutional fragilities, structural budgetary imbalances and acute household vulnerability. In these countries, a food shock can quickly turn into major social tension.

It is in this context that the Egyptian situation must be understood. The world’s largest wheat importer, dependent for nearly 80% of its wheat on Russia (60%) and Ukraine (19%) before the war, engaged in a social contract centred on subsidised bread and facing extremely tight economic and budgetary conditions, the country has seen its room for manoeuvre drastically and dangerously reduced. While wheat-based products account for 35% of the calories consumed by Egyptians and nearly 30% of households are living in poverty, the state decided to increase the price of subsidised bread, known as baladi bread, in June 2024. Amounting to nearly 300%, this increase is the first since 1989. Another sign of the regime’s nervousness: in December 2024, the state announced that the GASC[15] was relinquishing its public wheat-importing mission to an entity now led by the Egyptian Air Force, Mostakbal Misr (“the future of Egypt”). In line with the rest of the country’s most strategic economic sectors, Marshal al-Sisi’s regime continues to extend the military’s grip, at the cost of increasing opacity.

These vulnerabilities, whether they stem from trade dependencies, logistical shocks, budgetary and economic fragilities or internal political dynamics, outline a continental landscape that is deeply heterogeneous yet marked by a common fault line: the very unequal capacity of states to absorb an exogenous food shock such as the war in Ukraine. Above all, they highlight a broader phenomenon that is far from being confined to the African continent: these fragilities are embedded in a global food system whose equilibria were already precarious before 2022, and whose shock wave from the war in Ukraine has merely revealed the full extent.

A Global Food System Under Strain: Towards a New Balance of Power?

The war in Ukraine has not only disrupted agricultural and logistical flows: it has brutally revealed structural tensions already at work within the global food system. As T. Pouch and M. Raffray have shown in a recent article[16], the crises of 2007–2008 and 2011, the Covid-19 pandemic and now the current conflict should no longer be interpreted as anomalies, but as recurring manifestations of the fragilities of a system that has become profoundly unstable. The progressive erosion of multilateral mechanisms and of the rules that had structured trade openness since the 1990s thus appears to be shaping an environment in which conflictuality is becoming the norm rather than the exception. In this context, agriculture has (again) become one of the arenas in which power relations between nations are clearly expressed. Since the 2000s, the agricultural ambitions asserted by new actors such as Brazil or Russia have made this evident.

In the context of the war in Ukraine, the dynamics surrounding wheat make it possible to observe these reconfigurations in concrete terms. They help reveal how the return of the Black Sea to international wheat markets, initially a geoeconomic shift, has taken on a far more explicit geopolitical dimension. Since the 2000s, the rise of new agricultural export poles has led to a redefinition of global hierarchies. This rise has taken place even as traditional agricultural powers, the United States and the European Union, have entered a phase of relative decline. This is particularly visible in Africa, where Russian food exports have been gaining ground steadily for around a decade. While the continent is a particularly revealing case, it is not an exception: other regions, in Asia as well as in Latin America, are also seeing their food equilibria weakened by the succession of geopolitical, climatic and logistical pressures. The war in Ukraine thus highlights a broader shift: food has (once again) become an explicit instrument of power, mobilised to influence, stabilise or constrain. In an increasingly fragmented global food system, the control of flows, corridors and dependencies has again become a central element of international power relations.

Jérémy Denieulle, Director of Studies, Agriculture Stratégies

Quote this article:

Jérémy Denieulle, « Ukraine War, Four Years On: Anatomy of a Redefinition of the Global Food System », Agriculture Stratégies, 26 November 2025. https://www.agriculture-strategies.eu/en/2025/11/ukraine-war-four-years-on-anatomy-of-a-redefinition-of-the-global-food-system

This article was translated from French with the help of artificial intelligence.

[1] Alessandra Kirsch, Lore-Elène Jan, « Le conflit ukrainien : des reconfigurations en cascade pour maintenir la sécurité alimentaire mondiale », Agriculture Stratégies, 06/06/2023. https://www.agriculture-strategies.eu/2023/06/le-conflit-ukrainien-des-reconfigurations-en-cascade-pour-maintenir-la-securite-alimentaire/

[2] Let us keep in mind that the conflict in Ukraine began on 20 February 2014, following the Ukrainian Maidan revolution and Russia’s annexation of Crimea. Here, we will focus on the events that occurred after 24 February 2022, the date of Russia’s large-scale invasion of Ukraine, which marked a major new stage in this conflict.

[3] Jérémy Denieulle, « Géopolitique du blé : une céréale dans la mondialisation », Géoconfluences, November 2023. https://geoconfluences.ens-lyon.fr/informations-scientifiques/dossiers-thematiques/geographie-critique-des-ressources/articles/geopolitique-du-ble

[4] From Marine Raffray, « Guerre en Ukraine : les répercussions sur l’agriculture », Paysans & sociétés, 2022, vol. 392, n°2, p. 30.

[5] See for instance « Harvesting Conflict. Unlawful Attacks against grain and related infrastructure in the Odesa Oblast », Global Rights Compliance, May 2025. https://globalrightscompliance.org/wp-content/uploads/2025/05/Harvesting-Conflict_EN.pdf

[6] Nick Beake, Maria Korenyuk, « Tracking where Russia is taking Ukraine’s stolen grain », BBC, 27 June 2022. https://www.bbc.com/news/61790625

[7] Launched in November 2022, this programme aims to deliver grain to the poorest countries through partnerships with donor states (Germany, France, Japan, etc.) that finance transport and logistics. The diplomatic dimension of the programme is obvious, as Ukraine seeks in particular to counter Russia’s narrative on the African continent.

[8] See https://doi.org/10.4060/cd6008fr

[9] See Matthieu Brun, « Afrique : le retour de la faim ? », Politique étrangère, 2023/1. https://doi.org/10.3917/pe.231.0139

[10] See Joseph Glauber, Soonho Kim, Elsa Olivetti, Rob Vos, « End of the Black Sean Grain Initiative: Implications for sub-Saharan Africa », International Food Policy Research Institute, 7 août 2023. https://www.ifpri.org/blog/end-black-sea-grain-initiative-implications-sub-saharan-africa/

[11] On the West African example, see Thibaut Soyez, Matthieu Brun, « L’Afrique de l’Ouest face au défi de l’azote : dynamiques, dépendances et opportunités », Fondation FARM, 20 juin 2025. https://fondation-farm.org/lafrique-de-louest-face-au-defi-de-lazote-dynamiques-dependances-et-opportunites/

[12] Bread nevertheless remains an important product in the diet of Nigerians, especially in urban areas. See on this point Matthieu Brun, Jérémy Denieulle, « L’agriculture : talon d’Achille ou atout d’avenir du Nigeria ? », Le Déméter 2023, pp. 219-234. https://shs.cairn.info/le-demeter-2023–0011662119-page-219?lang=fr

[13] According to data from the Observatory of Economic Complexity, in 2023 Nigeria imported 2.97 billion dollars’ worth of wheat. This total is exceeded only by imports of tanks and armoured vehicles (9.17 billion dollars) and refined petroleum (17.6 billion dollars).

[14] Pierre Blanc, « Guerre en Ukraine et spectre de famine », Esprit, 2022/5. https://doi.org/10.3917/espri.2205.0031

[15] General Authority for Supply Commodities, a state agency responsible in particular for public wheat imports since 1968.

[16] Thierry Pouch, Marine Raffray, « Mondialisation, guerre et fin de cycle hégémonique agricole et alimentaire », Actuel Marx, 2025/1, n°77, pp. 190-208. https://shs.cairn.info/revue-actuel-marx-2025-1-page-190