Télécharger le PDF

Futures markets have become an almost essential part of the marketing strategy of farmers and their cooperatives, and they also exist in order to attract financial organizations, which provide the necessary liquidity. But while speculative practices contribute to increased price volatility, the profits they generate in times of crisis attract criticism, as in a recent report from CCFD-Terre Solidaire and Foodwatch, who judge the current[1] regulations to be insufficient in terms of transparency. The Council and Parliament agreed on 29 June to revise the regulation in force. Sufficient provisions to limit excessive price volatility?

The interest of futures markets for farmers

Speculation consists of buying with the aim of reselling at a profit, without the intention of using or keeping the merchandise. However, the first users of futures markets (MAT) are the farmers themselves, as well as their cooperatives [2], who seek to ensure a minimum price for their harvest as soon as possible[3].

Thus, at the time of sowing, farmers can commit a portion of their harvest to the futures market where they will find a “virtual” buyer ready to buy the corresponding volumes at a price determined by the contract end date (of sowing therefore), and which corresponds to an estimate, a bet, on the price that the cereal will be worth during their harvest one year later. In fact, the buyer will not take delivery of the goods. One year later, at harvest time, the farmers will unwind their position by purchasing a contract on the futures market which will correspond to the volumes committed, at the price in effect at that same time.

Two scenarios can arise:

- Case number 1: The physical or spot market price of cereal that traders are willing to pay to take delivery of the goods at the time is higher than that at which he sold his commodity one year earlier on the futures market. In this case, the contracts that the farmer must buy to unwind his position are worth more than those he sold the year earlier, and he loses money on the futures market. But the value at which he sells his product on the physical market is higher than he had hoped to sell a year earlier, offsetting this loss and balancing out the income from the sale of his harvest.

- Case number 2: the selling price of cereal on the physical market is lower than that at which it sold on the futures market. The contracts that the farmer must buy to unwind his position have a lower value than those he sold a year earlier; he makes a profit on the futures market which then allows him to offset the actual sale of the cereal at an unsatisfactory price on the physical market.

Like revenue insurance in the United States, the use of the futures market allows the farmer to hedge against the risk of a price reduction occurring between sowing and harvest , but these two systems have limited interest in periods of sustained low prices. The existence of a futures market makes it possible to provide liquidity to finance this risk-taking, with cereal sellers having no difficulty finding a “buyer” for future harvests, even a year in advance.

This hedging operation is also carried out by grain collecting organizations (OS), the primary buyers of cereal. In most cases, when a cooperative or a dealer buys its harvest from a farmer, it has not yet found a customer (miller, industrialist) to sell this merchandise to. Thus, it assumes to pay the farmer at a certain price level and it must put in place a mechanism to protect itself from the risk of price variation while waiting to find a customer. The cooperative secures the future sale of its stock by selling a contract on the futures market (a short position in futures ). The mechanism is the same as described previously: if prices decrease between the time it committed to buying the farmer’s harvest at a given price and the time it sells to an industrialist on the physical market, it will pocket compensation on the futures market when it unwinds its position by repurchasing a cheaper contract on the futures market during the actual sale on the physical market.

Speculation amplifies market volatility, but it is not the cause

For futures markets to function, they must remain connected to the physical market (the price set at a given time by the futures market must be close to that of the physical market at the time of maturity, and converge at the expiry of the contract) and not have a significant risk of failure of the actors, who must maintain an ability to absorb losses and ensure deliveries, even theoretically (it is necessary that after harvest, the possibilities of physical delivery are sufficient to cover most of the already contracts traded). A mechanisms exist to ensure that players in the futures market have the capacity to cover their losses: the clearing house makes margin calls every day which correspond to the difference between the position taken and the day’s price and result to calculate a sum that the trader must pay into his account if it is negative. When the market rises, market participants who have taken sold at a lower price at maturity must therefore advance part of the cash difference to ensure the redemption of higher positions upon unwinding. In periods of high volatility, margin calls can thus cause difficulties for market participants, in particular cooperatives that might momentarily not have sufficient funds before delivery to a buyer covers the cost of having bought grain to the farmers.

The prices of futures markets and physical markets are therefore linked, but these “fundamentals” are the primary link between the prices of futures and physical markets:

- Supply, which depends on the quantities harvested in the different agro-exporting countries and its quality

- Demand, which depends on annual consumption and stock status

- Energy, which will weigh on transport prices

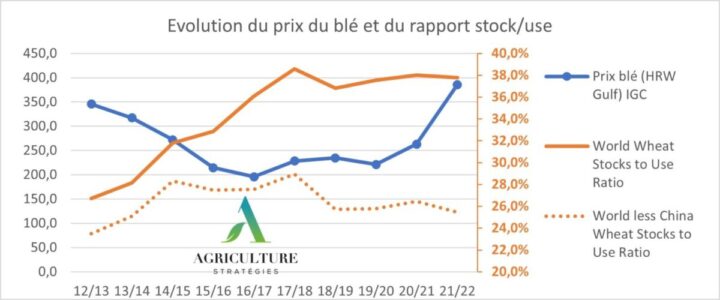

The lower the stock/consumption ratio is, the more reactive the markets are, because any lower harvest forecast will have a strong impact on the availability of countries that depend on imports for their food. However, this is not an exact science, and the distribution of stocks will also play a part. Since 2015, China has developed a very significant storage policy (it has wheat stocks which allow it to cover almost a year of consumption, when the EU has around 7 weeks of stocks), and now accounts for 45% of global wheat stocks over the recent period. We therefore must consider in the balance sheets the stock/use ratio of exporters.

Figure 1: Evolution of the price of wheat and the stock/consumption ratio for the world and the world excluding China, Source FAO/AMIS, Agriculture Stratégies processing

In the current period, geopolitical tensions will also have an impact on price formation. Decisions on whether or not to renew the Grain Corridor, which allows cereal to be taken out of the Black Sea, have recently had an impact on the price of cereal, as well as the increase in insurance premiums for maritime transport in these regions.

The very sharp increase in the price of wheat observed in 2022 can easily be attributed to the result of an accumulation of tensions on the market such as low stock/use ratio “excluding China”, fears of availability of Ukrainian and Russian cereal, and high insurance premiums in an inflationary context linked to rising energy prices.

Speculation is therefore not at the origin of the rise or fall in agricultural prices, but it might amplify the variations, because sale or purchase movements on financial markets will be rapid and dependant on the effects of economic announcements like harvest forecasts announced by the USDA or China, upcoming embargoes or political events.

Figure 2: Chronology of events and impacts on wheat prices by Arthur Portier, Agritel / Argus Media consultant (source Twitter: @PortierArthur)

In their report, CCFD and Foodwatch highlighted the increase in purchases made by financiers on the markets in times of crisis: the increase in wheat price would have attracted investors and contributed to a more rapid and significant change in prices. NGOs are calling for increased market regulation and more transparency.

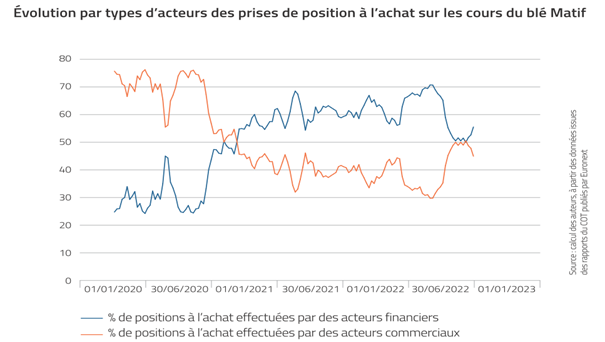

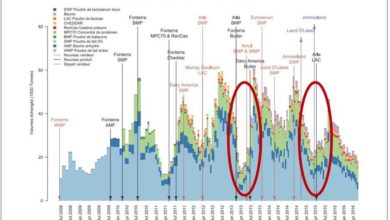

Figure 3: Evolution by type of actor of purchasing positions on Matif wheat prices, source CCFD/ Foodwatch

This graph shows the variation of purchasing positions (acquisition of purchase contracts) by financial players (credit companies, investment funds, etc., whose action on the markets is generally purely speculative) and by commercial players (storage organizations, manufacturers, farmers, merchant houses). This analysis must however be considered with caution because it is based on purchase positions (long positions). In periods of high prices, the interest of commercial players is to take selling positions, to hedge in the event of a price drop (we speak of short positions). They therefore hold a lower proportion of long positions.

A detailed report[4] from the French financial markets regulator (Autorité des Marchés Financiers, AMF) establishes several findings:

- On the European futures market, the weight of financial players is much lower on the wheat market than in the United States : between 2018 and 2021, commercial players held on a daily average 57% of positions, while financial players held the remaining 43% of positions. On Chicago wheat, salespeople hold 26% of the open position and financiers 74%.

- Until the 2019/2020 campaign, we observed a certain cyclicality for the commercials category with an alternation of long (purchase) and short (sell) positions. Since the 2020/2021 crop year, commercials have positioned themselves more and sustainably in selling positions while financial players and in particular investment funds have positioned themselves more in buying positions.

- The proportion of positions held by commercials decreased after the Ukrainian invasion, especially during the first 3 weeks, but this share then stabilized at a level also close to a year ago.

- Symmetrically in relation to commercial players, the share of financial players in positions increased following the Ukrainian invasion, but then stabilized at levels close to last year on the same date (after having decreased in December 2021 and January 2022).

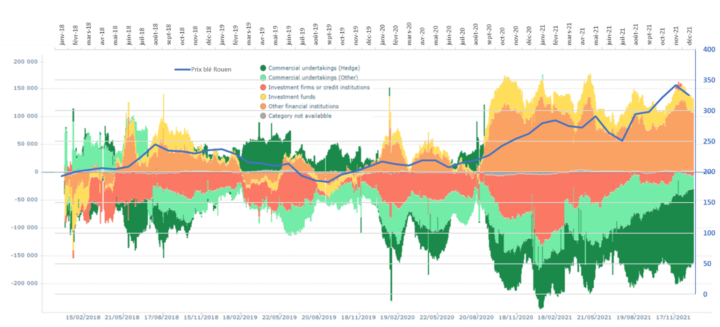

The graph below shows the evolution of the net positions taken by the different players between 2019 and 2021 and the price of wheat. Net position is the difference between a trader’s long (buy) and short (sell) positions at any given time. The upper part of the chart represents positive net positions which reflect a position orientation towards buying, while the lower part represents orientation towards selling. The green zones are those of salespeople, financiers are yellow, orange and red.

We can thus see the cyclicality mentioned in the AMF report for commercials: until the end of 2021, the green part is sometimes at the top of the graph, sometimes at the bottom, reflecting an alternation of purchase/sale position being taken depending on slight changes in wheat price. But the sharp increase in wheat price since the end of 2020 has led to an increase in transaction volume on the part of both commercial and financial players and a split market between commercials in selling positions and financials in buying positions.

Figure 4: Weekly evolution, between 2018 and 2021, of the distribution of net positions declared on Matif wheat contracts by category of actors, source AMF and price of wheat delivered to Rouen, source IGC (right scale).

European financial markets are increasingly regulated

Two regulations have already been passed in the EU to regulate the functioning of financial markets, ensure transparency of activities and transactions, and protect uninformed investors. The first dates back to 2004 (implemented in 2007), the second from 2014 (applied in 2018). These are the directives (known as Markets in Financial instrument directive or MiFID I and MiFID II) and the regulation (MiFIR) on financial instrument markets, transposed in the French law by the Mif regulation supervised by the AMF, the financial markets authority.

In particular, the MiFIR regulation imposes an obligation to declare transactions and to trade on regulated platforms[5]. The second version of the MiFID directive also regulated the development of high-frequency trading, managed by computers autonomously based on algorithms, capable of generating buy and sell orders intensely and quickly (in less than a second !). The directive now imposes a minimum price variation so that a contract can be bought or sold, we speak of “ tick size ” in English. For example, if the tick step is 1€, and a trader bought a contract for 200€, he cannot resell it for a different price before it has reached a value (quotation) of 199€ or 201€. This has the effect of reducing the number of orders that algorithmic trading can generate.

It also imposed limits on the number of contracts (position limits) that a single entity can hold with regards to agricultural raw materials, in order to prevent a company or group of companies from being able to disrupt the market [6].

Article 48 of the MiFID II Directive also provides for slowing down the market in the event of excessive price volatility (“Member States shall require a regulated market to be able to suspend or limit trading in the event of significant price fluctuation in a financial instrument on this market or on a related market over a short period” [7]). But while trading suspensions for a period can be applied on markets where company assets are traded (therefore where prices can be more easily exposed to manipulation), these suspensions should not be applied to agricultural markets. Agricultural markets are markets derived from agricultural raw materials, the price of which does not depend on the performance of a company but on the fundamentals that we described in the second paragraph (supply, demand, stocks, availability). No objective criteria have been clearly identified (a cap or floor price threshold, an amplitude of variation over a defined period) to justify that intervention was necessary in the market for agricultural commodity derivatives.

These provisions are insufficient for CCFD and Foodwatch, who call for an increased reduction in position limits, an exclusion of financial companies which speculate too much on agricultural raw materials, and increased transparency of markets to isolate the role of speculation from the formation of food prices. On June 30, 2023, Parliament and the Council agreed on an upcoming revision of the MiFIR Regulation and the MiFID II Directive. The upcoming changes will mainly focus on improving data transparency, and access to the consolidated market data which is necessary for investors.

But new future provisions could also more specifically concern the agricultural sector (and could also apply to wholesale energy products and emissions quotas). This would involve setting minimum contract holding periods [8], which would make buying and reselling over very short periods impossible and would neutralize the possibilities of high-frequency trading. It could also be a question of specifying conditions that would justify the suspension of the listing of agricultural raw materials.

Conclusion

Improving the functional landscape of agricultural markets without driving away the financiers necessary to support the ecosystem by providing liquidity is a challenge. If regulations become too restrictive and limit the prospects of profit or “wedge” investors by preventing them from reselling at the desired time, there is a significant risk that they will withdraw from the agricultural markets, or see a disconnect between futures market prices and the physical market if these cannot be sufficiently reactive.

The balance is subtle, and we must keep in mind that the future regulations will only cover European markets, while a significant part of the financial flows linked to agricultural raw materials will continue to pass through the American futures markets, establishing the main drivers in terms of price trends for agricultural raw materials listed on financial markets.

If the current review of European regulations is an opportunity to be seized so that the financial authorities can contribute to limiting the volatility of agricultural prices, it will not be able to replace the disarmament of the CAP intervention tools, and the chronic insufficiency of the strategic reserve to deal with market disruptions.

Alessandra Kirsch, Director of Studies at Agriculture Stratégies

September 18, 2023

[1]https://www.foodwatch.org/fileadmin/-FR/Documents/Rapport_final_inflation_speculation_CCFD_foodwatch.pdf

[2]To understand cooperative strategies on the subject, see this very good article on Terre-Net: https://www.terre-net.fr/actualite-des-marches/article/170692/la-commercialisation-un-processus-fortement -supervises-in-cooperatives

[3]For a more detailed explanation of how futures markets work, see https://agriculture.gouv.fr/vers-la-definition-dun-nouveau-cadre-de-regulation-des-marches-derives-de-matieres-premieres

[4]https://www.amf-france.org/sites/institutionnel/files/private/2022-07/Analyse%20des%20donn%C3%A9es%20MIF2%20sur%20les%20d%C3%A9riv%C3%A9s% 20de%20mati%C3%A8res%20premi%C3%A8res_0.pdf

[5]See this article from Les Echos to understand the contributions of the 2014 regulations: https://www.lesechos.fr/2018/01/mifid-ii-les-six-cles-dune-reforme-qui-bouleverse-les-marches -financial-981050

[6]For the thresholds imposed, see https://www.amf-france.org/sites/institutionnel/files/private/2023-05/Limites%20de%20position%20pour%20les%20instruments%20d%C3%A9riv%C3% A9s%20sur%20mati%C3%A8res%20premi%C3%A8res%20n%C3%A9goci%C3%A9s%20sur%20Euronext_0.pdf

[7] paragraph 5: https://eur-lex.europa.eu/legal-content/FR/TXT/HTML/?uri=CELEX:32014L0065

[8]https://www.europarl.europa.eu/doceo/document/A-9-2023-0040_FR.html

Thank you very much.

Several thoughts.

1st high frequency trading does not supply any functional traits to the ‘future-liquidity ecosystem’ that has benefit for ‘farmers’. Restricing its to a 1€ limit is a begninning, but nothing more. In the first three hours of today, global wheat commodity prices transgressed this limit already 3 times.

The basic financialization process in commodity futures markets which transformed commodities into an asset class is still ongoing and as a problem to food security and fair competition growing. Incorporated into the portfolio decisions of investors, commodity prices now behave like all asset prices, becoming more volatile and subject to periodic bubbles (just as with all other assetts the argument is always made, that they are funamentally linked to fundamentals, like real estate to land and cement). As commodity prices were driven higher since the 2000s, farmland is becoming more valuable (in fact the best performing assett in EU over the last 20 years), setting off a land grab by investors, nations, and corporations. This is combined, under the financialization food regime, slow growth and low returns encouraged merger activity driven by private equity firms, with food industry corporations as prime targets, leading to increased industry concentration. This is combnined with digitalization – seed to fork – which allows particular actors with immense information advantages – like Cargill – outperform all others in trading.

Do you have thoughts on how to counter these massiv and growin market imbalances?

Thank you!