Created in 2008 by the New-Zealand cooperative Fonterra, the auctioning platform Global Dairy Trade acts as a reference for the prices of international milk powder and butter trades. An extensive analysis was conducted by the Center for Studies and Strategic Foresight of the Ministry of Agriculture lays out in detail the shortcomings of this device. With the equivalent of one third of New-Zealand’s exports, which is about 1.1% of world production, the representativeness of the platform is questioned. Especially the asymmetry in favor of the main supplier which allowed him to drastically reduce the quantities during the spring of 2013 raises the question of a possible manipulation which translated into a raise of 2013’s prices and a loss of confidence from most stakeholders in the robustness of the device. More widely, this analysis leads to the conclusion that the European Union must adopt value sharing mechanisms, like the ones in place in the US or Canada, to limit the negative effects on dairy producers and the entire sector of this biased compass for international markets that Global Dairy Trade is.

For the last 25 years, the Common Agricultural Policy reforms aimed at increasing the connection between the European agriculture and international trade so that international prices can steer productive choices. This evolution naturally brings us to consider the reality of international trade’s price formation. If cereals and sugar profit from the futures markets place that are Chicago, London or Paris as price references for transactions, milk and dairy products do not benefit from such well-established negotiating platforms. To remedy this situation, the New-Zealand based cooperative Fonterra implemented, at the end of 2008, Global Dairy Trade (GDT), a digital auctioning center, considered by many as the reference market for international trade of dairy products. The prices from the platform being often used in the discussions on the price of milk in France and in Europe, including for locally consumed products, it is interesting to analyze this tool. This is what Jean Noel Depeyrot and Marion Duval from the Center for Studies and Strategic Foresight recently did.

Operating principles

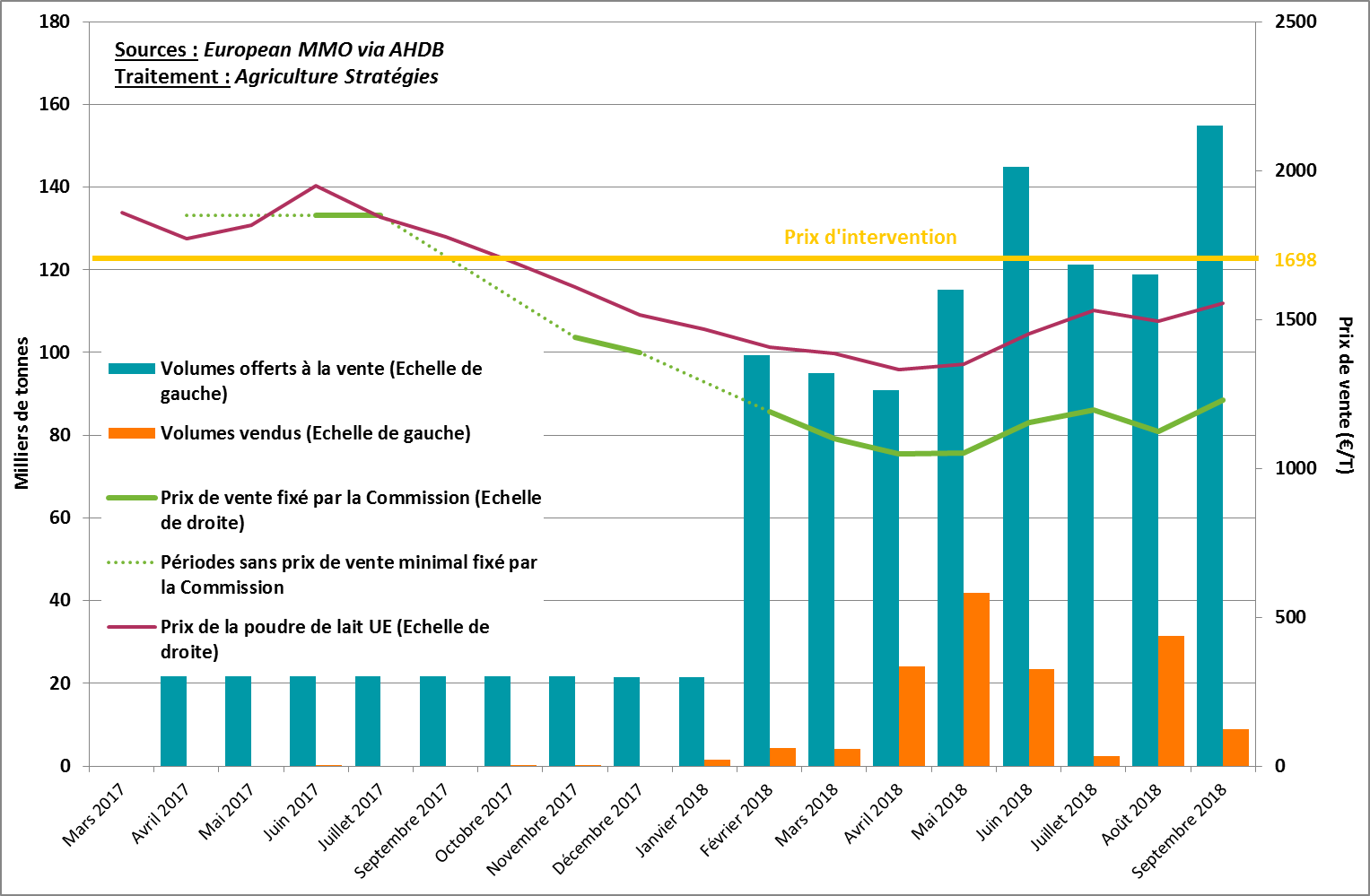

Biddings take place every 15 days. The sellers indicate the quantities they want to offer for sell and a minimum price for their merchandise. When the auction starts, the auctioneer announces the starting price, so the buyers can state the quantity they wish to purchase at that price. If the quantity of merchandise offered by the seller is inferior to the quantity the buyers wish to purchase, a second round is held with higher prices, and so on until offer meets demand. In the particular scenario where the demand is lower than the initial offer (which happens one third of the time when over 5% of the initial offer of skimmed milk powder doesn’t find a buyer), the products offered aren’t sold and the final price is the initial price.

Few participants

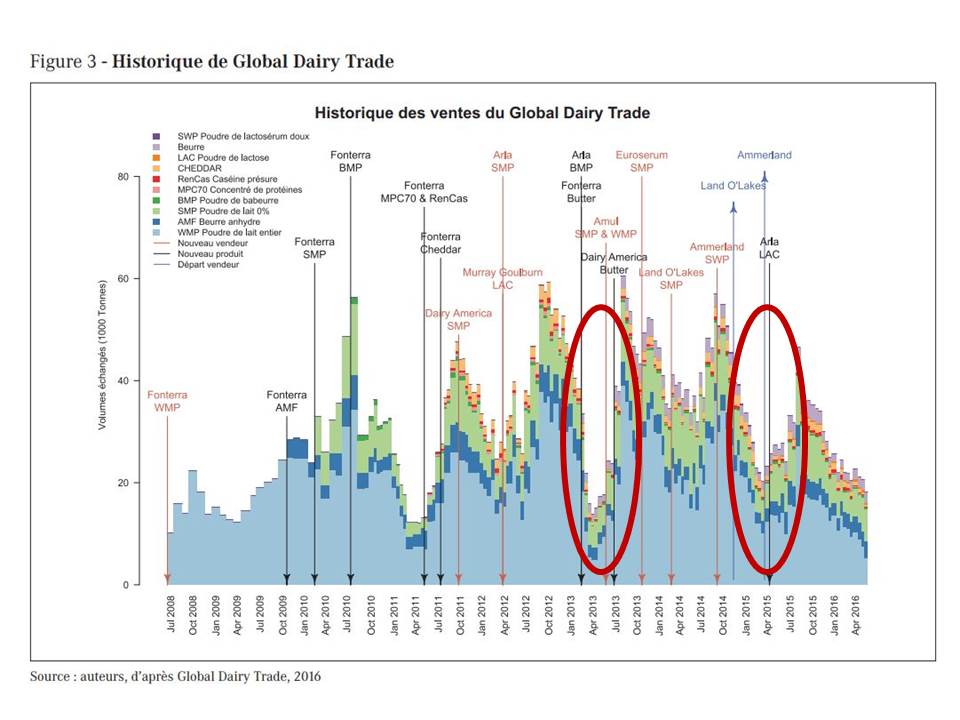

When GDT was created, Fonterra was the sole vendor. Then the New Zealand cooperative tried to attract other vendors, but the new participants, such as the Indian Amul, the American Dairy America or the French Eurosérum were only involved between 2012 and 2014. Nowadays only Fonterra and the Danish Arla regularly offer sales, Fonterra remaining the main vendor. Over 90% of trades on the platform are done off only 4 products: whole and skimmed milk powder (which represent over 90% of GDT’s activity), butter and anhydrous butter. Fonterra secures respectively 99%, 59.6%, 91.6% and 88.3% of those products’ sales. On the buyer side, there around 160 buyers for each auction.

16.3% of worldwide exports and 8.8% of worldwide production of milk powder

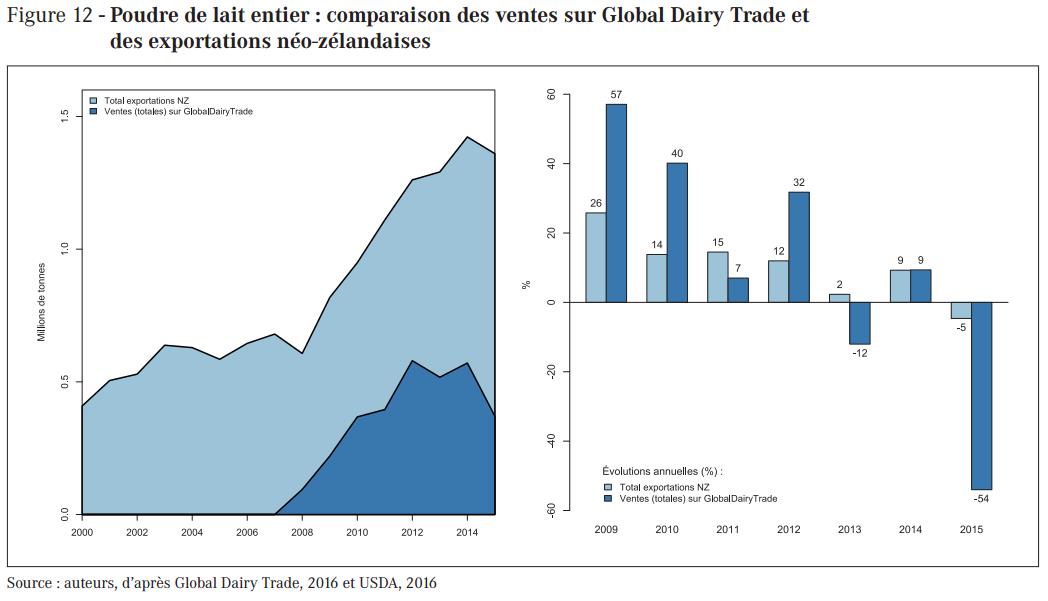

If milk powder was the main product traded on GDT, the quantities sold on the platform remain quite small. On average since 2012, 700.000 tons, the equivalent of 16.3% of worldwide exports and 8.8% of worldwide production of milk powder transited through GDT. Furthermore, the authors considered that only one third of New-Zealand’s exportations go through GDT, the rest going through bilateral contracts.

Moreover, the quantities sold on GDT are very variable through time. Even though the sale rates are high (more than 95% for milk powders), the authors emphasize on the strong fluctuations of the volumes sold, especially during the springs of 2013 and 2015. Admittedly, milk production in New-Zealand is characterized by a strong seasonality, the fact still remains that milk powder is a storable product. By comparing the variations of all of Fonterra’s exports and GDT’s volumes, it appears the latter are much more variable. Hence, in 2015 New Zealand’s exports have shrunk by only 5% whereas the GDT volumes were cut by half (-54%).

Given the way the auction works, with the volume offered by the vendor being critical, the severe drop in amounts offered for sale during the spring of 2013 begs a question. Knowing it lead to prices soaring, but that it globally did not affect exports over the year of 2013, one can wonder if Fonterra’s strong brake slam on volumes offered during the spring of 2013, under the pretense of bad production conditions, did not put off the buyers. If Fonterra had willingly wanted prices to soar, they would not have handled things differently.

More volatil prices and a weak predictive power

By comparing the prices from GDT with the prices of powder in the US or in Europe, the authors show that the prices from GDT are 2 to 3 times more volatile. Moreover, they brought to light that the movements happening on the platform have a very weak predictive power. In order to do so they studied the price differences in time (the ratio of prices at two different terms). They managed to observe that when the actors anticipated a rise, it only happened 57% of the time, from which they concluded the platform and its stakeholders had “more of a following role than one revealing trends”.

Did Fonterra break apart a laudable initiative?

Having information on prices and volumes of international trade are a necessity: the lack of information harms the proper functioning of markets. Fonterra’s initiative is inherently commendable in so far as it avoids having to force transparency on economic agents’ activities like in the US. However, insuring the development of a spot market takes time and requires building the stakeholders’ trust in order for the market to be considered a solid reference by all the participants. For financial markets, a “market maker” is usually the institution (often a bank) that insures the development of the trade platform by insuring a minimal liquidity. In our current example, Fonterra obviously failed in 2013 by not insuring sufficient liquidity and lead to the price increase of 2013. Moreover, it is for the least surprising that GDT doesn’t provide transparency on its market data anymore since the summer of 2015: the data is now chargeable. Five of the GDT vendors out of 8 left, and these might be elements to explain it.

Teachings for Europe

International markets are surplus markets in which international prices can be below the production costs of all the producers. This is even truer for dairy products where GDT is only representative of a fraction of international trade and the bidding rules allow the main seller: Fonterra, to have a role that is much too strong. Therefore, the “world price” of dairy products remains a fiction and wanting, no matter what; to make it a central reference for the European market is madness, which no great producing country is pursuing.

The transformation of milk powder only represents a fraction of total dairy products. And by definition it is the least differentiated the least qualitative, and the one that clears the least added-value. Unfortunately, the argument of low international price of milk powder is often used to impose price drops within the domestic market on products that have more added value. Therefore, if the European Union wishes to build its integration into the international market without driving its farmers to doom, it must necessarily develop, similar to the US or Canada, added-value sharing mechanisms between production and transformation in order to restrict the exposure of its interior market to this biased compass of international markets that GDT is.