Download the PDF

Direct sale and short food supply chains are on the rise, a trend which has been emphasized with lockdowns and the willingness of citizens and politicians to support more local consumption. Unlike long supply chains, which involve several middlemen between producer and consumers (collecting, processing, packaging, distribution), the short supply chain is defined by a limited number of middlemen (a maximum of one intermediary in France). Direct sale is part of short supply chains, but it does not involve any intermediary. In the mind of the consumer, this means the value goes directly to the producer. But does short supply chain guarantee a better revenue for the farmer?

Because it is therefore up to the farmer to assume all the stages necessary for production, possible processing, packaging, and selling to the consumer. In addition to being a farmer and manager of an agricultural business, he must then be trained in processing techniques, master health processes and standards, become a salesperson to find outlets, sometimes a webmaster. These steps lead to a considerable increase in working time, costs and risk taking for the farmer, which is never pictured on the consumer’s side. Let’s take a look at the preconceived ideas on the subject.

1) The short supply chain is the guarantee of a local product and a better ecological footprint

Not necessarily. Short supply chain is only a guarantee aimed at limiting the number of middlemen. Product can travel miles between its producer and the only middleman responsible for processing and/or distribution. This is why we now distinguish between short supply chains and local supply chain: the short supply chain takes into account the number of middlemen; the nearby supply chain takes into account kilometres travelled by the product between its place of production and consumption.

An Adème[1] study examines the environmental impact of short supply chains, which is considered better through this supposed reduction in kilometres travelled. It also details that the environmental impact considers the way of producing, regardless of the distance covered (for example heated greenhouse or not), and the logistics involved for transport. The pooling of transport made possible by the industrialization of the sector might be more economical than the partly empty round trips of multiple vans.

2) The short supply chain allows farmer to set his prices

Not completely. The farmer remains in a world of competitiveness where the price set must be acceptable to the consumer, and he must therefore respect a minimum and maximum price range, regardless of his additional costs. Given the complete or almost complete elimination of middlemen, the consumer expects a price close to that found in supermarkets, without considering the additional charges which cannot be crushed as in an industrial system.

And in the case of the short supply chain where the producer sells directly to a distributor, an agreement still must be reached. Supermarkets seek to promote a local product to attract consumers, but prices remain hardly negotiated. For example, the added value paid to the producer for a cow is about € 0.80 to € 1.20 / kg of carcass in addition to current market prices. It is a more profitable outlet but does not allow to sell many herds (a supermarket will sell about one heifer or one cow of this type per week). In the case of sale to butchers, only the best animals are selected, as well as in greengrocers, where the fruits and vegetables must be “beautiful”. Remember that in agriculture, generally, it is not the seller (the farmer) who makes the invoice for the product sold, but the buyer. The farmer receives a milk payment, a sales slip, but it is not the one who issues it.

3) It is profitable for the farmer

To this key issue, the answer is not obvious. In a consumer’s view, within a fair-trade logic, the prices paid to the producer are higher, and, in the absence of middlemen, they must therefore pay more the farmer. In this logic, the consumer does not expect prices radically different from what he can find in supermarkets. But behind these slightly higher prices there are also a lot of additional charges. This will differ depending on the production, the need for processing or not, the kilometres to go to the slaughterhouse or to meet the consumer and will generate a significant working time that it would be normal to be able to pay. In agriculture, however, this question of labour is often overlooked. Since it is a passionate profession, it often seems “normal” not to count the hours spent. Is it “normal” that the farmers are ready to work always more to hope seeking only a result which would be not negative?

There are many forms of short supply chains: marketing in vegetables baskets, markets, stores or groups, choice of investing in a processing laboratory or resort to a service provider, etc. These choices will result in a different workload and additional costs. We can thus note that in the field of breeding, the added value allowed by the sale in short supply chain compared to the traditional supply chains remains low (Cf box).

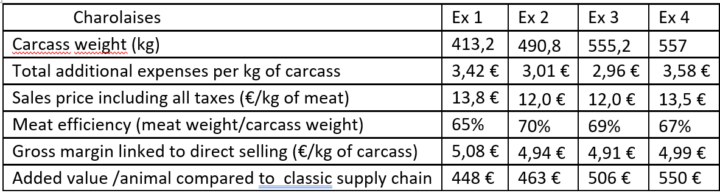

Box: quantified examples of the profitability of direct sale in breeding

For example, in breeding, the short supply chain often involves more demanding specifications which increase breeding costs. Then come the costs of transport and slaughter, then cutting, possible processing and vacuum packing; while the cooperative comes to take delivery of the animals alive. Finally, farmer must succeed in enhancing the whole carcass, while the consumer is more easily interested in noble pieces.

In the case of direct sale, the meat/carcass yield is essential: while in the case of a sale to a cooperative or distributor the price is negotiated in € / kg of carcass, in the case of direct sale, it is the pieces of meat that are sold, and the margin is therefore made on the meat yield of the animal. Only animals with the best conformation are chosen to enter this system; they therefore cost more in finishing (as in every agricultural production, it is the last kilos of live weight, the last pounds or the last litres of milk that are the most expensive to produce).

For breeders who can claim it, the calculation remains interesting: in the four examples below made from real situations, the breeders control the additional working time by resorting to a service provider for processing and vacuuming. The gross margin given by direct sale earns around € 1 in addition to the current market price (around € 4 / kg of carcass). The margin thus gained depends on the selling price, the conformation of the animals and the selected processing services (sausage meat, etc.). It allows an added value per animal of 450 to 550 € compared to the traditional supply chain and represented 1 to 1.5 days of work outside breeding. Depending on the farms and the number of interested consumers, 2 to 3 animals per year can be valued in this way.

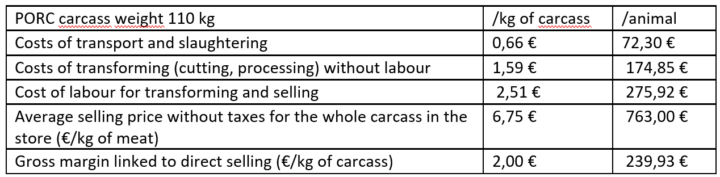

In the case of a breeder who seeks to develop this activity, and to internalize the cutting and processing activities, profitability becomes more difficult to find, especially when considering the workloads. In the example below, made from real figures of a farm, which raises pigs on straw and in outdoor and lambs, and which has a direct sale store near a consumer area, and therefore a rather favourable situation. The fixed costs of the transformation workshop and direct sale store (in particular the working time for transforming and the selling of the 2.5 FTE of qualified labour and an annuity for the laboratory and the store of 18 000 €) are spread over 300 pigs and 125 lambs. Once these working hours are paid, the margin allowed by direct sale is 2 € / kg of carcass for pigs. But when the breeding costs specific to this type of production (around € 1.86 / kg of carcass excluding labour) are deducted, there is not much left to pay the breeder and his work. Pig production does not get huge amounts from the CAP, paid mainly per hectare, because it usually uses only a small amount of land. However, compared to examples of selling price of farm pork under label of 1.62 € / kg of carcass, which would not even cover the cost of production linked to breeding, the exercise remains economically interesting.

The cost of labour, when it’s taken into account, therefore strongly penalizes the margin, since these on-farm processing units do not benefit from the economies of scale of industrial models, and the time dedicated to sales is significant in the case of direct sale. For market gardeners, there are fewer additional processing steps, but it is still necessary to condition the products, and take time to sell them. The transport costs to meet the consumer (markets, drives, community-supported agriculture) weigh on the charges. According to a study by the Loire Chamber of Agriculture, the production part represents only 36% of the working time of a specialized market gardener. Harvesting, sorting and preparation represent 35% of working time, and selling 30%, for an annual working time of 4,650 hours / year (2.76 FTE). The average working time of the market gardening manager is 56h / week[2] , to be paid between one and two annual minimum wage. In these systems, which often rely on volunteers and family labour, it is not possible to remunerate the working hours spent by the self-employed.

In addition, the short supply chain and direct sale imply new investments for the farmer. Storage or even sales premises, equipment for transporting animals or finished products, cold room, processing workshop, etc. Depending on the product targeted, the costs can be significant, and it is not always possible to pool these investments. In niche markets, the customer base is not always large enough to allow equipment to be shared with a potential competitor. And once the investments are made, it becomes necessary to maintain an activity. This has led a certain number of farmers to embark on expensive tours in terms of working time and transport costs during lockdown to ensure the sustainability of their outlets and sell their perishable production.

Finally, we must not forget that the initiatives which allow the farmer to benefit from an existing distribution network have a cost, usually deducted from the turnover of its suppliers. The producer must still organize himself to carry out the delivery and packaging.

4) We can feed cities with peri-urban agriculture in short supply chains

No. While problems of changing land use linked to the expansion of cities are increasing, due to the pronounced taste for residential homes with gardens, metropolises are showing ambitions to reconnect with local agriculture. There are many examples of purchases by communities of agricultural land to supply collective catering with fruit and vegetables, which are part of territorial food projects. The latest example is that of the city of Grenoble, via the farm “Mille Pousses”, established on a plot of 2700 m2 provided and serviced by the city, which allows its mayor, Eric Piolle, to congratulate himself on moving forward towards food self-sufficiency.

However, as a journalist demonstrated using a simulation tool[3], 2700 m2 can feed 6 people annually with vegetables and 8 with fruits, if the surfaces are only dedicated to this. To feed the 160,000 inhabitants of Grenoble, it would be better to rely on 56,600 hectares (standard diet)…

If the idea of providing a remunerative outlet via collective catering to local farms is quite interesting, as is that of convey agricultural real estate by communities, we should therefore not be lulled into illusions as to the degree of self-sufficiency that peri-urban farms can provide. They can effectively bring a useful complement or strengthen the territorial links but cannot make it possible to move towards food autonomy.

5) All farmers can get started in a short supply chain

No. To enter into short supply chain and exit (at least in part) from traditional circuits, it is necessary to have a sufficient consumption pool nearby, which is far from being the case for all rural areas. Depending on the type of production, some infrastructures are also necessary (slaughterhouses in particular). In addition, if this mode of marketing is possible for products requiring few or no processing (honey, fruits and vegetables and to a lesser extent dairy products and meat), for other sectors it is more complicated. For example, regarding cereals, if there are a certain number of farmers who have tried flour milling, the outlet remains limited in relation to the amounts of wheat supplied by a farm. In these productions, short supply chain can only concern a small part of the operating turnover.

According to the latest data available from the French Ministry of Agriculture[4], 21% of French farms sold part of their production in short supply chain in 2010. 50% of farms with areas with vegetables or beehives used short supply chains, but the share of turnover resulting from this was very variable.

Short supply chains are generally seen as an excellent initiative, able to bring producer closer to the consumers, to restore the seasonality of products and to give back value to production. During the lockdown, farmers have shown a great ability to adapt and to find new outlets for their production, in order to avoid unsold goods. But the researchers noticed that consumers then quickly returned to their habits, and the demand for short supply chains, although remaining above its previous level, then fell. The organization developed by farmers to cope with this flash increase in demand must then once again demonstrate agility.

For consumers who continue to use short supply chains over the long term, through this act of responsible citizen consumption, the feeling of participating in a form of fair trade, gainful for farmers, dominates; but the reality is that most of this value is consumed by an increase of charges that the consumer does not perceive. If the short supply chains continue to be supplied, it is because the self-employed farmers (managers, family workers) are for the most part not paid in accordance with their workload.

The choice of the short supply chain therefore stems from a desire not to depend only on market prices, greater involvement in the chain towards consumption, a hope of “making a better living from one’s profession” which takes precedence over the burden of additional work, sometimes even on economic rationality.

While the role of middlemen was precisely to crush the costs linked to logistics and transformation, isn’t the advent of short supply chains just further proof of the failure of the distribution of value? Would they not rather be the glaring demonstration of the weakness of the farmers in the weight of the traditional trade negotiations which leads them to have to appropriate new trades and to work always more hours to hope to preserve a semblance of profitability? While short supply chains and direct sale can only be partial solutions, in France let us hope that the upcoming electoral periods with the Regional (June 2021) and the Presidential (May 2022) will lead politicians to learn the lessons of the diversions of the spirit of the Egalim law to really rebalance the distribution of added value.

Alessandra Kirsch, Director of studies of Agriculture Stratégies

March 17, 2021

[1] Adème is the French Agency for ecological transition. Here is the report (in French) : https://www.ademe.fr/sites/default/files/assets/documents/avis-ademe_circuits-courts_201706.pdf

[2] https://extranet-loire.chambres-agriculture.fr/fileadmin/user_upload/Auvergne-Rhone-Alpes/120_Extr-Loire_img/Pages_thematiques/Elevage/doc_diagnostic_maraichage_2009.pdf

[3] https://parcel-app.org/

[4] http://46.29.123.56/IMG/pdf_primeur275.pdf