Download the PDF

How can we better manage market crises in the European Union? This is the question that Agriculture Strategies answered in a study commissioned by MEP Eric Andrieu to feed his proposals for the reform of the CMO regulation, one of the three regulations of the Common Agricultural Policy. While the European Commission is pleased to finally have disposed of the last few tonnes of milk powder stored in Community stocks, this study provided an opportunity to assess the European Commission’s strategy to tackle the 2015/16 milk crisis.

When the “soft landing” strategy ends in a crash

The 2015/16 milk crisis is directly attributable to the abolition of milk quotas on 31 March 2015. Recorded in 2008, this decision was taken by the Council of European Ministers in the euphoria of the general rise in agricultural commodity prices observed from 2007 onwards. The Commission’s proposal included a strategy known as the “soft landing” strategy, which asserted that, by gradually increasing the production cap, prices would decrease until they reached their equilibrium level, at which point it would no longer be interesting for producers to produce their entire quota. Once this transition was completed, the “quota rent” would have disappeared and the quotas could be removed smoothly.

It is evident that things did not go as planned: the “soft landing” strategy will remain in the annals of economic policy errors in the agricultural sector. At issue are two main factors: the structural instability of international markets and the structure of production costs in dairy farming. The sharp rise in dairy product prices between 2012 and 2014, partly due to the artificial reduction of volumes sold on the New Zealand Global Dairy Trade platform, led producers to euphoria: Chinese stomachs were going to be insatiable. While quotas increased by 7% over the period, European production increased by 9.9% between 2008 and 2015, with some producers preferring to pay the fine for exceeding quotas.

Because once investments are made, farmers have no individual interest in reducing their production: the fall in prices initiated in 2014 and amplified by the Russian embargo had no effect on production dynamics. Undoubtedly, the spontaneous adjustment of supply based on prices does not work in agriculture and especially in the milk sector, which is why quotas were installed in 1984! And, as we press the accelerator to hope to break through the wall, the end of quotas has not been questioned, further exacerbating the crisis due to overproduction: in the first year after the end of the quota, European production increased by 4.9%!

The voluntary milk production reduction scheme, a definite but partial success

From July 2015, the fall in milk powder prices triggered public purchases, which rose to 350,000 tonnes, exploding the initial ceiling of 108,000 tonnes. Faced with producers’ consternation, in September 2015 the European Ministers of Agriculture started to reflect on the measures to be taken: a direct aid package of 500 million euros was released, without putting an end to the crisis.

As the European Union is one of the major exporting countries, overproduction had an impact on international prices, leading to complaints from other countries such as New Zealand. Reducing production was first considered when the Dutch cooperative Friesland-Campina announced support for its producers who would reduce their production, and it was not until April 2016 that the Commission proposed to activate Article 222.

This article allows all actors in the sector, from companies to producers and inter-branch organisations, to derogate from competition law and agree to limit overproduction. There was however no effect, or even the slightest initiative among actors.

The solution, which has been available since the beginning of the crisis, eventually emerged in July 2016: a voluntary milk production reduction scheme (Article 219). The Commission offered an envelope of 500 million euros to reward farmers who committed to reducing their production over a period of 3 months. The success was immediate: while the aid was to be deployed in four stages, 98.8% of the aid was requested during the first stage, and the price of powder rose as soon as the measure was announced because of its psychological impact on market players and their expectations.

Of the 500 million euros announced, 390 million euros were finally spent – some requests were not fully eligible – on a 2.2% reduction in European production in the last quarter of 2016. It was used by 8.3% of dairy farmers, with Belgium and Ireland leading the way. Given its success in rebalancing the market, it is a shame that it hadn’t been activated sooner: it would have made it possible to pile up less powder in public stocks.

A stock disposal strategy that leads to dumping prices for powder for over a year

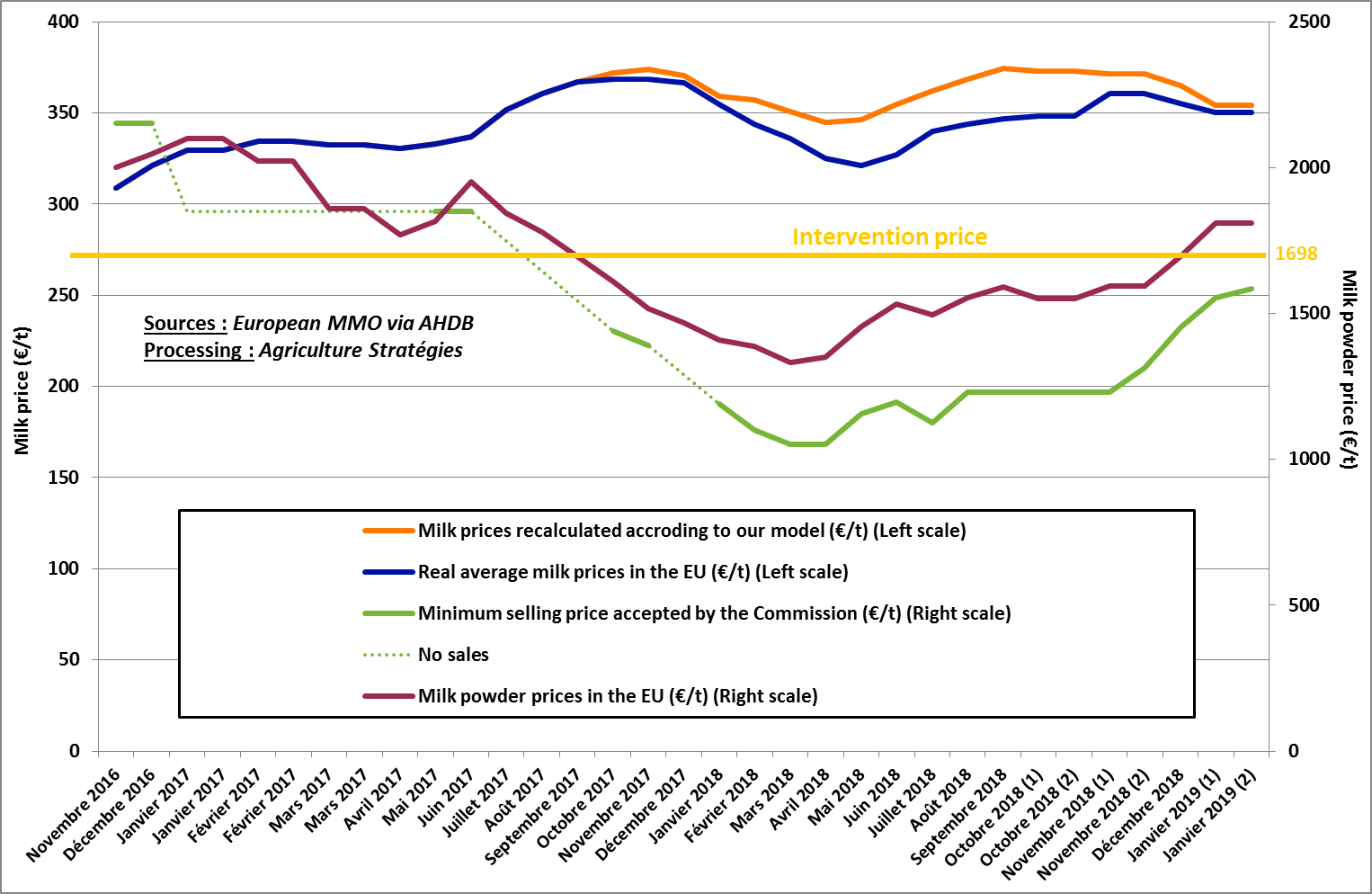

2017 was the year of recovery in milk prices, which came closer to the level of production costs. It was in September 2017 that the Commission decided to use an offensive approach to sell the 350,000 tonnes of powder stored. Yet, this volume is to be put into perspective: it represents about 2% of annual production in Europe. Unlike previous periods when stocks were released, where several tools were used – such as donations to charities or animal feed aids – the Commission chose to sell the powder only through calls for tenders. This measure offers the possibility of selling below the intervention price, which makes it possible to consider liquidating stocks very quickly by selling them off.

But here again, the Commission seems to have made a mistake in its analysis by assuming that economic operators would have an interest in buying these discounted volumes as quickly as possible. In the end, it appears that they preferred to take advantage of the dumping effect of tender prices on the price of powder and therefore of milk, thus defeating the Commission’s strategy. The latter went so far as to accept bids at €1,050/tonne, well below the European floor price of €1,698/tonne. And, if the stocks were eventually sold by the end of 2018, it is largely due to the drought that affected important production areas in the summer of 2018.

More than two years to sell the equivalent of a week’s milk production, it would surely have been better to use other instruments to reduce stocks and take advantage of the tensions on the butter price to play on the expectations of the market players as recommended then. Moreover, due to the drop in powder prices they caused, under-priced tenders had a dumping effect on the milk price.

By using an econometric model explaining 97% of the variation in milk prices by different variables including the price of powder, we tried to simulate the price of milk if the powder price floor had been respected. On the graph below, the actual observed price is represented in blue and the simulated price in orange. The difference thus corresponds to a shortfall for European dairy producers. According to our estimates, this shortfall amounts to €15/tonne on average, or 2.3 billion euros over the period in which the price of powder was lower than the intervention price. More than a loss for producers, it is a value transfer from producers to processors. This is how in the end, the disposal of a stock worth a bit less than 600 million euros will have cost producers 2.3 billion euros!

In addition, by buying the powder for less than €1,698, the powder market players as a whole generated a profit that can be estimated at €140 million in its upper range (purchases may have taken place at a price above the accepted minimum price). It seems that the Commission does not have information on the identity of the buyers, but it can be assumed that part of this 140 million subsidy corresponds to an export subsidy, an instrument that the European Union had however committed not to use again. Finally, to complete the balance sheet, it is necessary to mention the costs of public and private storage, for which we have not found any public information.

In the end, one can only remain doubtful when, with regard to the disposal of stocks, the Commissioner for Agriculture stated in January 2019: “I decided on this course of action with the clear aim that we would get rid of most stocks without putting pressure on prices”. At this stage, the Commission’s services have not published any work evaluating their actions during the milk crisis. This seems necessary both to initiate a process of progress in the management of the Community markets and to account for the public money spent. This work will also have to establish the reasons why, in the run-up to the abolition of milk quotas, not all Member States have implemented the provisions relating to the strengthening of producer organisations, whose role in matching supply and demand is all the more necessary in the milk sector, as supply does not spontaneously respond to falling prices.

Jacques Carles, President of Agriculture Strategies

Frédéric Courleux, Director of studies for Agriculture Strategies