In the first article of this series, we have shown that the effectiveness of private risk management tools depends on the type of price volatility. In the second article, an examination of the American experience has confirmed the limitations of income insurance benefits to manage market risks. In the third and last part of this triptych, we cover the relevance in developing futures markets for the European dairy sector, and draw up recommendations for public policy developments.

The European dairy sector has been faced with repeated crises for the past decade. The functioning of the various markets interfacing with the links in the chain is generally incriminated. The imbalance in negotiating powers is put forward to explain the sharing of added value, which is deemed inequitable by the upstream production steps. Exposure to hazards is also highlighted as breeders complain they represent the “adjustment variable” that must bear most of economic environment variations.

In this context, the functioning of the grain sector is a source of envy for dairy farmers, since the major grains have price quotations that must be followed by all operators in the sector. In particular, the reference for wheat is the Chicago futures market, which sets the tone for the whole planet. In fact, futures markets provide transparency on price formation for all operators. This transparency is clearly lacking in the dairy sector, where breeders find out a posteriori the prices paid for their production. In addition, this type of financial market provides tools such as futures contracts and options that allow farmers and all operators in the sector to design coverage strategies over one or two years. This way, growers can, if they wish, be directly involved in their marketing process, whereas breeders find out the price paid when opening the envelope of the milk payment.

Of course, it must be remembered that these tools are no remedy whatsoever when markets are durably depressed. Yet, developing them would unquestionably improve the current situation. However, it is important to keep in mind that developing futures markets in the dairy sector requires conditions that still do not seem to be met today. To meet these requirements, the stronger implication from public authorities is necessary. In addition, even by making dairy futures markets really take off, the added value sharing between production and first transformation would remain unresolved. In this article, we will outline the various analysis points leading to these conclusions, and we will again learn from the American agricultural policy to understand how the US collectively resolved the problems of value sharing, transparency and the development of futures markets.

The development of futures markets is not imposed by decree

A specific number of conditions are required so that economic players make use of futures markets and sustain their operations. Building collective trust in the futures market ability to provide representative prices of product marketing is fundamental1. There are scores of futures contracts that were closed down shortly after their launch due to a lack of participants. The most concrete symptom of futures market malfunctioning is the more or less temporary differential between price quotations on futures markets and those on the underlying physical markets (that is to say where goods are traded). This difference is called the base. The best way to prevent the base from over fluctuating is to connect futures markets and physical markets by allowing, when contracts are due, buyers and sellers of futures market to make a payment in nature for their commitments (physical settlement). Yet, payment in nature is not always possible, and requires the benefit of stockpiling capacities. As a result, there is another arrangement in which expiring contracts are paid in currency (cash settlement) according to a reference price set elsewhere.

Three conditions are generally mentioned to explain the development of grain futures markets. The first one is because wheat is a commodity that can be stockpiled, a fact that allows the connection between futures and physical markets at the above-mentioned contract expiration. Historically, futures markets were developed based on stockpiling certificates that were exchanged in advance. The second condition implicates the large number of operators involved, as there are many buyers and many sellers who agree on a commodity standard specification. The product’s origin and destination do not matter. The third condition is explained by the centralization of the underlying market. For instance, this is the case of the European export market, for which the port of Rouen historically occupies a key position. The most evident pattern is the stock market where securities are listed in a continuous and centralized manner. All operators thus have an excellent view of the price formation of the underlying, and the futures market of securities can therefore easily operate as a market derived from the underlying market. This is actually the source of the other name of futures markets––the derivatives markets.

The challenging emergence of European contracts of dairy products

Let us take a look at milk. It cannot, by nature, be stockpiled. Even refrigerated, it must be processed within 72 hours of milking. In addition, milk producers and the dairy plants that collect the milk are in a situation of mutual dependency: in general, there is only one collector by zone and dairy plants need milk from their collection zone to operate. As a consequence, there cannot be any continuous quotation for the milk bought from producers. Thus, we can understand why the development of futures markets for processed, storable and standardized products, such as dry milk, butter of whey powder, is more easily promoted.

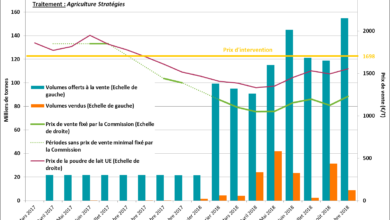

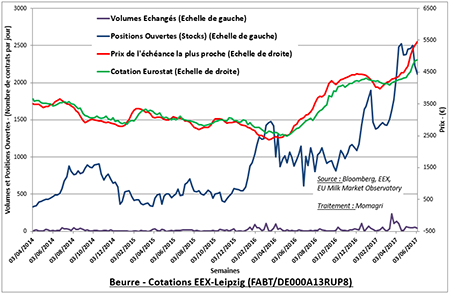

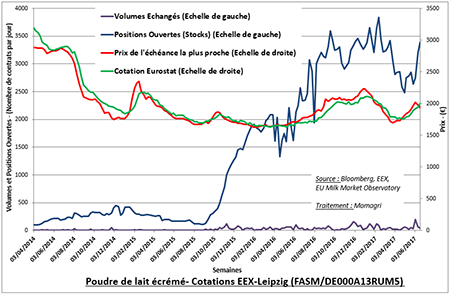

However, these conditions may not be enough. Euronext––the Paris exchange––has, on several occasions, launched quotations of futures contracts on these processed dairy products. The previous attempts have failed, and the most recent one seems to be doomed to the same fate. At present time in Europe, only the Leipzig-based European Energy Exchange (EEX) has actually activated contracts on dairy products. As show in the graphs below regarding butter and powder, business is growing, even if it is relatively low compared to physical production. In fact, we list an accumulation of 2,500 outstanding contracts for butter and 3,500 for non-fat dry milk. At a rate of 5 tons of butter or powder for each contract, all open positions account for 455,000 tons of milk equivalent, or compared to the European production of about 150 million tons, the equivalent of 0.3% of the annual European production.

Beurre – Cotations EEX-Leipzig

Poudre de lait écrémé – Cotations EEX-Leipzig

The number of contracts traded dairy also illustrates the poor level of development of European contracts. Over the past 12 months, a daily average of 34 contracts for butter and 47 for powder were traded. These futures markets were actually launched during the first half of 2014, and it is still too early to see if the momentum initiated will be sufficient to ensure an adequate activity level to reach a minimum depth (relative to the underlying physical market), and sufficient ongoing liquidity (enough operators to buy and sell so that one operator’s entry or exit does not destabilize the whole exchange).

In fact, so that futures markets can endure, operators must capture them, whether they are economic players in various sectors or financial operators providing liquidity. It is often needed, at the launch of a contract, that a market maker––generally a bank––guarantees the minimum liquidity. Subsequently, financial funds may also take over, but in proportions that must remain reasonable so that these operators––generally less informed on the actual shifts in market fundamentals––do not distort price formation, which would lead to a loss of trust by non-financial operators, and thus their withdrawal.

Quotation quality and trade transparency

When due, EEX contracts on dairy products are only payable in currency (cash settlement) et not in nature (physical settlement). This may seem inconsistent since the quoted products can be stockpiled. This option (of simplicity) is nevertheless risky because it requires having a quotation sufficiently representative, so that it is not contested. When the underlying market quotes continuously––such as securities––there is no problem. It is quite more complicated when underlying products are traded OTC, and occur among few traders, as it is the case for processed dairy products. The official quotation will then be made by interviewing a few physical traders, who are themselves swayed by the development of futures prices. We must also point out that official quotations on dairy products in France are directly made by the federation of dairy processors. The risk is then that the futures quotation and the physical quotation somewhat get into resonance and self-sustain upward and downward during sufficient time to reach levels considered as abnormal, which can lead to a loss of trust from operators.

The role of public authorities then becomes crucial. If trade is not transparent enough, they must be able to inflict a system to declare trade and prices within the various sectors. This is already the case for dairy products in the United States. In Europe, adding questions on product prices to the monthly dairy survey could already be an interesting foundation. In fact, overcoming the information asymmetry of economic agents must allow better market performance, including that of futures markets.

In the US, futures markets are progressing thanks to marketing boards

While the development of futures markets for dairy products provides an interesting outlook for a better performance of the whole sector, the fact of the matter is that it would only very partially resolve the issue of value sharing. Indeed, futures quotations can, by definition, only concern standard commodities. But the larger part of milk production is used to manufacture fresh products with a higher added value. This outlet entails milk production constraints that must be borne by breeders who are rightfully demanding a share of the added value. For instance, we can mention the seasonal adjustments of production, or the superior sanitary quality required for the creation of fresh products all year long. This also applies for distinct products, such as those covered by quality labels. In other words, European milk prices cannot be set solely based on processed product prices, which remain marginal valuations.

There are two patterns to integrate other components than marginal valuations into the formation of prices paid to producers. The first one is followed by the “giant” cooperative firms in Northern Europe. This type of vertical integration allows producers to integrate the share of added value resulting from fresh products in the formation of milk prices, which thus includes all outlets.

The second pattern brings us back to the American continent where, in the US or Canada, the collective marketing of the milk whole production of a region is based on negotiation rules on the sharing of added value according to the various dairy products2. In both cases, all producers in a same zone get the same basic price. In the United States, there are 10 milk marketing offices, or Milk Marketing Orders, that group the producers from 1 to 4 States. Under the aegis of the Federal Government, a precise monitoring of production and markets leads to price formulas for the various types of dairy products that are grouped in 4 categories. Thus, for each category, the amount of the added value to be returned to producers is determined. The monthly base price paid to all producers is therefore the same, and corresponds to the weighted sum of prices for each category. So that each processor can pay the same amount, an equalization system between processors is funded. Processors positioned on the best segments therefore finance those that are less well placed. These transfers are substantial and can account for 10 to 15% of production sales.

Overall, this mechanism of added value sharing also functions as a base for dairy product futures markets, which are far more developed in the United States than in Europe. The system of monitoring production and markets operates as a base for futures markets: on the due date, official quotations specifically serve as references for cash payments of futures contracts. The convergence between futures markets and physical markets is therefore guaranteed. Furthermore, contracts listing milk prices paid to producers for products included in two of the categories (III and IV) were launched for producers. This is why there are futures markets for liquid milk in the United States. This is not because American producers are more “open” to market operations, but because futures markets in the United States are fully integrated in the sector’s regulations.

In conclusion, we can only stress the deep meaning of this series of articles: Private tools to manage risks are not substitutes to public regulations. On the contrary, we must seek to reconcile these two types of tools! In the case of processed milk outlined in this latest article, the American example reveals a structuring rationale: by seeking to implement a stable framework to achieve a fair sharing of added value, it was possible to formalize transparency in the dairy sector and develop futures markets. An involvement for European agriculture may directly stem from the American model. Seeking to develop markets in Europe without improving transparency in price formation and dealing with the issue of added value sharing is really putting the cart before the horse. And ultimately with the risk of not moving forward in the design of a regulation framework to improve market operations. And consequently, to maintain the current situation where the price formation procedure and added value sharing are based on the activity tractors in the roundabouts near the milk processing plants.

Jacques Carles, Founder and chairman Agriculture Strategies

Frédéric Courleux, Director of studies of Agriculture Strategies

1 Sur les conditions d’émergence d’un marché à terme, voir en particulier

http://agreste.agriculture.gouv.fr/IMG/pdf/doctravail31109.pdf

2 Voir la partie 4 de l’étude suivante :

http://agriculture.gouv.fr/etude-sur-les-mesures-contre-les-desequilibres-de-marche-quelles-perspectives-pour-lapres-quotas