In the first article of this series, we demonstrated that the effectiveness of private risk management tools depended on the type of price volatility.

Very effective when prices oscillate regularly around production costs, but no longer the case when market signals demonstrate “rare spikes and large troughs”.

In this second article, we give an analysis of the interests of the different promoters of private risk management tools based on the evolution of private risk management policy where it is most developed, the USA.

The United States are frequently cited as an example for the expansion of insurance in the agricultural sector, and in particular for turnover or income insurance.

As proof, the term “assurances revenus” frequently used on this side of the Atlantic corresponds to the approximate translation of revenue which actually signifies turnover in the US, whilst the term income is used for farmers’ income. However, this should not be really all that confusing, as both cases entail a combination of risks on production and risks on product prices (and possibly intermediate consumption).

While income insurance is highly developed in the United States, it should be pointed out that the government has played and continues to play a major role in this development. In addition, US agricultural policy is not limited to these tools alone, as is it is sometimes believed, but on the contrary it should be known that these tools are used with other support mechanisms, be it countercyclical aid or national solidarity programmes against natural disasters. Incidentally, it is the search for the right balance of these instruments, in a context of falling agricultural prices, which since the last US agricultural policy reform in 2014, has led to a decline in private risk management tools with a refocusing on countercyclical aid.

In this article we review the key stages for the expansion of insurance in the United States, in order to put a perspective on the new directions of this matter initiated under Obama and visibly pursued by Donald Trump given the recently announced cuts.

This perspective means we can objectify the positioning of the main promoters of income insurance companies in France and Europe, so as to refocus the debate on the future of the CAP which continues to turn a blind eye to any lessons already learned from the American experience.

Dusty beginnings

In the United States, agricultural insurance was developed at the end of the 19th century, on a mutual benefit basis by farmers and their professional organizations.

It was not until 1938 and the second version of the Agricultural Adjustment Act of 1933 that we saw yield risks truly integrated into the federal agricultural policy.

The Dust Bowl, which occurred between 1934 and 1937, was also seen as a good reason to develop yield risk insurance which went beyond damage caused by hail, which by definition was localised.

The Federal Crop Insurance Corporation (FCIC) was created in 1938 as an agency of the USDA, the US Department of Agriculture. With a much smaller budget than its older sister in charge of market regulation, the Commodity Credit Corporation, the FCIC’s original objective was offering insurance contracts to cover 50 to 75% of yield losses.

While mutual benefit insurance schemes were developing on hail damage, the success of the federal program didn’t quite meet expectations; the penetration rate did not exceed 10% of field crop land until the early 1980s.

The reason: competition with federal disaster payment programs and the absence of insurance premium subsidies. Indeed, it was not until 1981 that aid programs for natural disasters would be systematically triggered, that premium subsidies would appear (30% for subsidies) and that a logic of a public-private partnership would emerge to make insurance companies (derived for the most part from unions or trader subsidiaries) into private reinsurers.

The American Agricultural Insurance Company, a subsidiary of the Farm Bureau, is still one of the leading private reinsurers. Thus the functions of the FCIC are evolving: it is refocusing on the definition of contracts, the calculation of premiums and above all it truly takes on the role of public reinsurer.

Income insurance, a major part of the FAIR Act of 1996

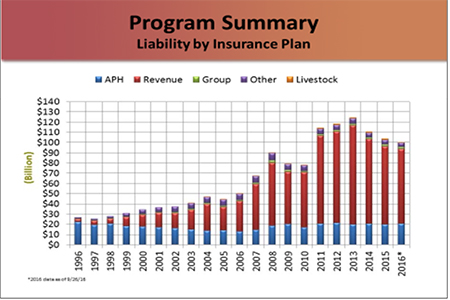

At this point in time, US agricultural insurance only concerned yield risks and not market risks. The latter were in fact managed by supply management programs until the mid-1980s and above all by countercyclical aid. It would be necessary to wait until 1996 with the reorientation of the American agricultural policy under the FAIR Act for income insurance to be given a high ranking. Moving away from market and income stabilizing mechanisms, this reform marked the implementation of the decoupling of aid. Income stabilization was then assigned to income insurance and the FCIC was reinforced to form the Risk Management Agency (RMA).

The graph below illustrates the rise in “Revenue” insurance beginning in 1996, expressed in value of insured crops. It is estimated that in 2016, more than 80% of US crops were covered through the federal insurance program involving a 1,117 million farms.

Value of Insured yields by type of cover, source USDA1

With this new orientation, insurance is clearly seen as a substitute for public intervention: it is a matter of no longer disturbing market function with distorting agricultural policies, the clear objective is to smooth incomes and not to support them, the subsidizing of insurance policies must be transitional and be justified by a phenomenon of adverse selection (premiums are very high for farmers with less risk)2.

A progressive calling into question

Unfortunately, the prise set-back observed in 1998 forced the government to re-establish emergency aid, and by 2002 countercyclical support programs had re-entered the Farm Bill, with in passing, a reduction in decoupled aid. And, above all, with the development of biofuels, the government is launching a new outlet to remedy surpluses.

But it is truly the reform of 2014 that will mark the end of decoupled aid, as well as a major evolution on income insurance. The reason being, the margins of insurers and therefore the low efficiency of the transfer of public money from the federal budget to the farmers were increasingly criticized.

The profit rates for reinsurers which vary between 10 and 25%, except for some years of loss such as 2012 and its severe drought, are difficult to justify.

Reinsurers remunerate the capital mobilized as collateral for the policies they manage risk for. And indeed, for the insurance policies they consider the most risky, it is even possible for them to have the contract signed by the RMA as a public reinsurer. In addition, subsidies are paid directly in proportion to the distribution of insurance policies.

Over the past 10 years, farmers have contributed an average of $3.7 billion and received $8.1 billion dollars in compensation, with a net balance of $4.3 billion.

By cumulating, subsidies to insurance premiums (to the order of 60% of the total premium) as well as subsidies for distribution and profits for reinsurers, the amounts paid out by public authorities amount to $8.7 billion.

The efficacy of the transfer of public funds to farmers does not exceed 50% for the period; the rest ($4.4 billion on average) is for the insurance companies. Finally, it should be said that in recent years, marked by lower prices and few climatic incidents, there has been a drop in compensation.

So in 2016, farmers will have received just under $3.6 billion in benefits, while having contributed just over $3.4 billion!

Hence farmers received only $0.2 billion while the cost to public finances exceeded $5 billion, which confirms that Insurance companies garnered $4.8 billion!

Beyond the low efficacy of transfer, the year 2016 demonstrates that income insurance is of no help when prices low long-term.

By introducing the Dairy Producer Margin Protection Program (DPP-MP), which gave dairy farmers direct aid to ensure a minimum margin level, the 20143 Farm Bill provided a major break in the development of insurance.

Indeed, this program, sometimes mistakenly called margin insurance, does not fall under the RMA and the insurance companies. It is in fact a flexible countercyclical aid with the participation of the farmers.

Moreover, raising reference prices for countercyclical aid (PLC and ARC) also reflects that confidence in insurance as an effective tool for income support over extended periods of low prices is shrinking.

Successive announcements for insurance budget cuts demonstrate this, such as those in 2015 by Tom Vilsack Obama’s agriculture secretary: “cuts in agricultural insurance can help offset the rising cost of new programs [countercyclical] ARC and PLC”4.

Additional cuts announced by Trump

The target of these budget cuts was primarily contracts based on the possibility of updating the guarantee level at the time of harvest in the event of higher prices.

With the election of Donald Trump, this calling into question of income insurance is amplified. The main cuts announced in May 2017 concerning agriculture, and which should be decided by Congress for the 2018 budget, relate mainly to the RMA5 budget.

The elimination of contracts based on the possibility of updating the price at harvest was proposed for 2018, with an average saving of $1.2 billion per year. Moreover, while a linear decrease in the subsidy rate at 40% was discussed, it is ultimately a ceiling of $40,000 of the amount of subsidies for insurance premiums per farm that is planned; for a reduction of annual expenditure estimated between 350 million (according to the Congress Budget Office) and 1.62 billion (according to the executive). Finally, the third measure, for a more modest reduction of $40 million, will exclude Farmers with an income of more than $500,000 per year from insurance subsidies.

These announcements were obviously received negatively by agricultural organizations. For them, this is a bad signal within the current context of low prices and these cuts would be added to those already seen during the last Farm Bill, although during the latter the price forecasts were much more optimistic, which contributed to underestimating the future costs of otherwise reinforced countercyclical aid programs.

In addition, agricultural organizations are heavily involved in the distribution of insurance (not just federal insurance) and private reinsurance. The future of these activities in connection with the federal program is also at stake.

For the past few years, we have witnessed a concentration of the private reinsurance industry, with the departure of players such as Wells Fargo, the 4th largest bank in the United States, or John Deere, and the arrival of Swiss or Japanese foreign insurers6.

What are the lessons for Europe? Decrypting the players’ game

So, does the evolution taking place in the United States with the abandonment of decoupling, the refocusing on climate risk insurance and the reinforcement of countercyclical aid for market risks feed the debate on the evolution of the CAP? No!

Promoting decoupling and income insurance are two sides of the same coin: the belief in the efficiency of markets, that is, the ability for prices to return by themselves to the level of production costs.

It is not surprising that the proponents of the status quo of the CAP showcase private risk management tools.

This is the case with a recent report by the RISE Foundation, whose recommendations were presented at the conference on the restitution of public consultation on the post-2020 CAP, organized by the Commission on 7 July7.

There are the usual arguments:

“government aid should only be temporary, for example, to help meet the costs of the organization of producers or during the launch of the private insurance markets when they are underdeveloped”;

“risk mitigation must primarily be based on private risk management measures”.

The part specific to risk management, signed by the economist Erik Mathijs (who has no publication to show on the subject), develops the classic argument to justify the withdrawal of government intervention: the insurance market would work be better!

Beyond those who defend the status quo and the experts, convenient for giving a touch of scientific authority, the stance of other types of players must also be discussed in order to complete the panorama of protagonists in the promotion of private risk management tools: Administrations in charge of agriculture, insurance companies and agricultural organizations. And this in particular from the US experience.

In those places where risk management mechanisms are truly developed in the broad sense (USA, Canada and Spain), it has resulted from a significant investment by the public authorities in the design and articulation of complementary tools.

Contrary to the RISE report, eliminating traditional public intervention tools to develop the offer for private risk management tools is not enough. The Risk Management Agency employs nearly 500 civil servants, experts on the subject. How many counterparts can be counted in the European capitals and in Brussels? The question is raised.

Faced with a decline in economic competence within the administrations in charge of agriculture and the usual procrastination, it is more than tempting to adopt the thesis which sees the solution to agricultural crises in the delegation of insurance markets.

Furthermore, who would not like to be seen as the saviour, with a hand on the CAP’s purse strings? No one.

Even if they are aware they have been given a role that they can’t keep, and say so with more or less force, insurance companies do not really have an interest in sending messages to limit their inflation expectations on economic risks. Insurance companies do not really benefit from sending messages to limit inflation expectations of them on economic risks.

They will be able, and this will be positive, to complete the offer of accessible insurance against climate risks. It is nevertheless troubling that we see little of them testifying in the different arenas discussing the boom in private risk management tools.

Finally, even if here also generalizations are always delicate, it is necessary to be aware that the DNA of small farmers is constructed in such a way that farmers most often look to solve their own problems, and are wary of statist abuses whatever they might be.

And it must be said that the cooperative movement’s refrain of “let’s do our own business” has been rather successful for them. Like American farmers, it is tempting to participate through their professional organizations in the development of new activities particularly if they are presented as solutions to their main problem, namely the instability of agricultural markets and incomes. Several major mutual benefit groups in banking and insurance are of course derived from this movement.

However, because this concerns insurance for market risks, this same willingness, which at first glance would make common sense, is simply another ingredient for staging Europe’s political impotence on agricultural matters, sending the CAP straight towards the renationalization of all the dangers for farmers and the building of European.

In short, comparing the trajectories of the Farm Bill and the CAP is an interesting exercise.

Faced with the discovery of the limits of decoupling and private tools for managing economic risks, it took less than a decade for the Americans to return to countercyclical aids.

Another decade would have been necessary to eliminate the latest decoupled aid and to challenge income insurance on its ability to cope with price volatility.

Conversely, Europe continues to see itself as a “virtuous but isolated leader” and for the time being cannot make a clear examination of the deadlock on the strategy adopted, conjointly with the United States at the beginning of the 1990s.

This is how the EU has become stuck in a logic that is catastrophic for farmers: decoupling + insurance-based risk management. A guarantee for the continuing collapse in incomes and richer operators, responsible for “placing” insurance … including certain intermediaries that could be linked to the unions, as is the case in the United States.

Errare humanum est, sed perseverare diabolicum.

Jacques Carles, Founder and chairman Agriculture Strategies

Frédéric Courleux, Director of studies of Agriculture Strategies

1 https://www.usda.gov/oig/webdocs/05401-0007-11.pdf

2 Voir en particulier le rapport du Congrès Budget Office rédigé par James Vertrees en 1983 pour une synthèse de cette nouvelle orientation. https://www.cbo.gov/publication/15263 On relève notamment que l’auteur omet complètement la question de la nature systémique du risque de marché : touchant tous les producteurs en même temps, le risque de marché n’est pas assurable par mutualisation. Voir du même auteur « Decoupling and U.S. Farm Policy Reform » publié en 1988 http://onlinelibrary.wiley.com/doi/10.1111/j.1744-7976.1988.tb03315.x/abstract

https://legacy.rma.usda.gov/aboutrma/budget/17cygovcost.pdf

3 Pour une présentation détaillée du Farm Bill 2014 :

http://agreste.agriculture.gouv.fr/IMG/pdf/analyse741410.pdf

4 Voir http://www.agriculture.com/news/policy/obama-budget-cuts-crop-insurce_4-ar47344

5 Voir https://www.obpa.usda.gov/25rmaexnotes2018.pdf

6 Voir http://www.insurancejournal.com/news/national/2016/04/01/404000.htm

7 http://www.risefoundation.eu/images/files/2017/2017_RISE_CAP_Full_Report.pdf