The abolition of the European sugar quota regime in 2017 did not have the expected results. The prospect of increasing European production to develop exports quickly turned into a drop in sugar prices and tensions in the governance of the sector, particularly in France. Heavy industry par excellence considering the transformation process, where the perishability and the heavy nature of the raw material explain the strong dependence between the links of the production and the first transformation, this sector also does not have important margins of maneuver to build a strategy of upmarket and “decommoditization”.

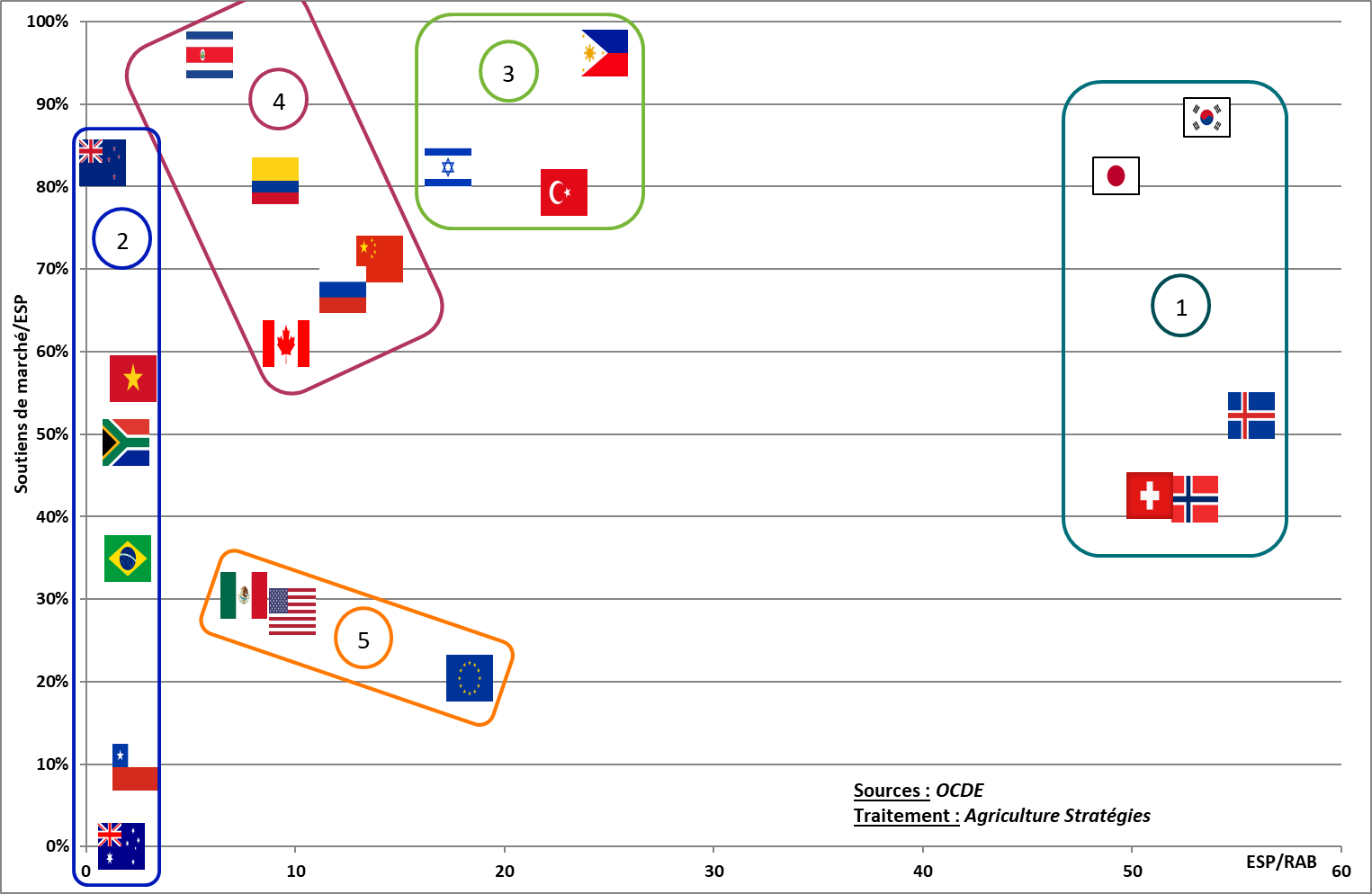

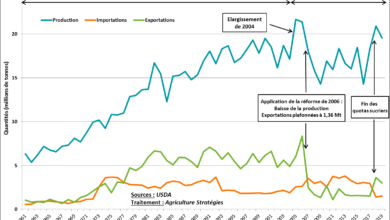

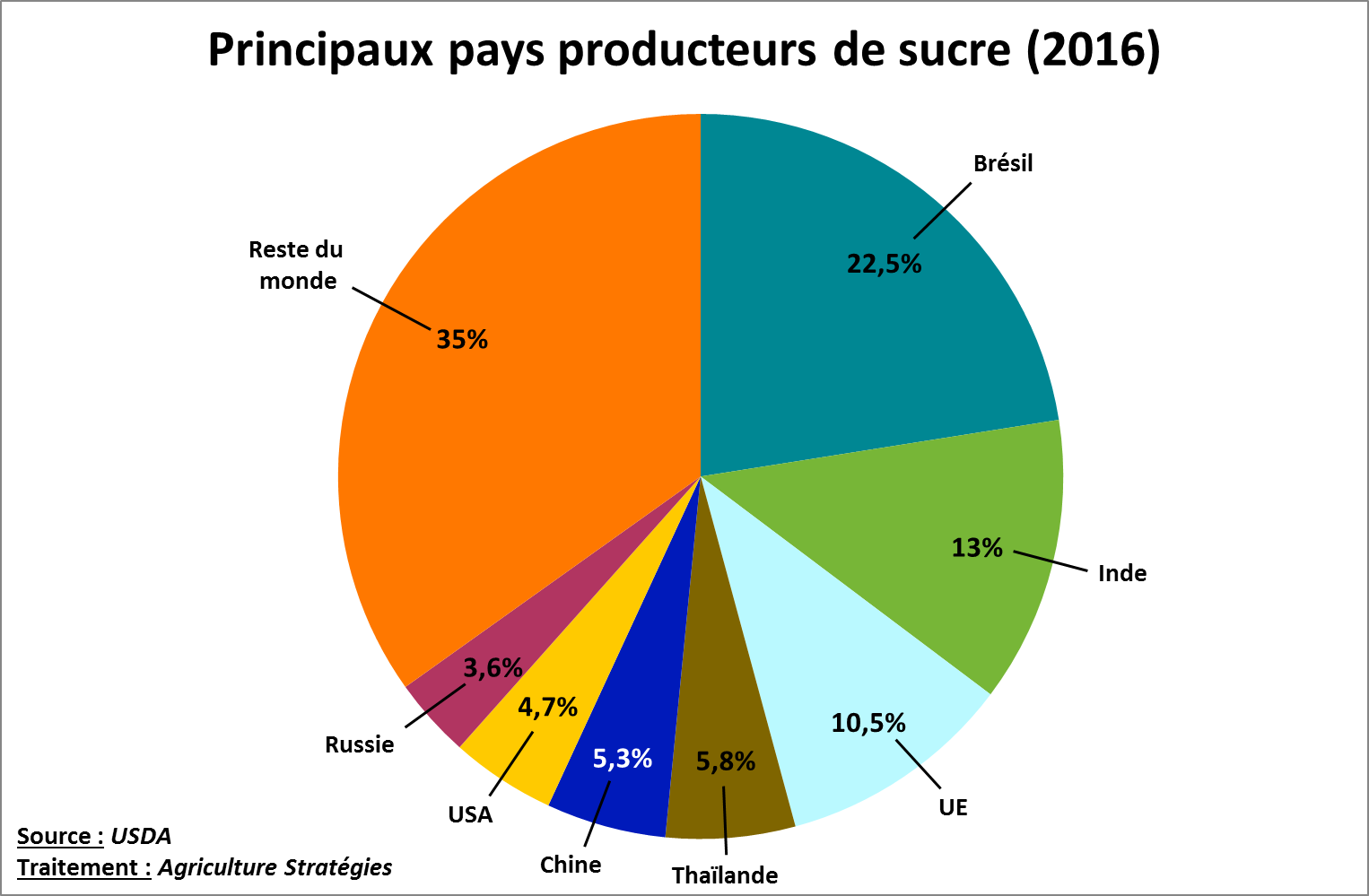

In these conditions, the exposure to the volatility of international markets, where the surpluses of the main producers are mainly exchanged, can undermine the entire sector because of a lack of strong public policy. In order to envisage a new regulatory framework for European sugar production, we propose a series of articles to study the different sugar policies of the main sugar producers. We will focus on Brazil, India, Thailand, China, the United States and Russia, which together with the European Union account for nearly two-thirds of world production (see Figure below). ). This panorama will allow us to conclude this series by constructing different scenarios of evolution of the European sugar policy.

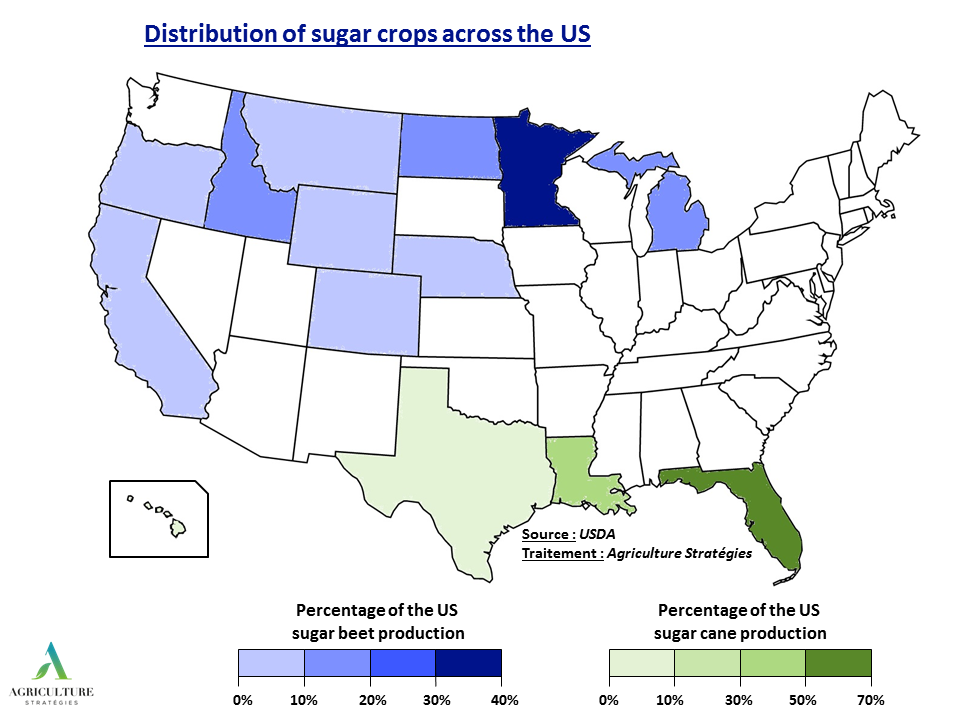

The United States currently rank 6th among sugar-producing countries with about 9 million tonnes or 4.7% of world production in 20161. One of the main features of the United States is to produce almost as much sugar from sugar beet (56%) than cane (44%). Sugar beets are found mainly in the north and west of the country (34% of beet production in Minnesota), while sugar cane has historically grown in the southern states (Florida, 54% of cane and Louisiana, 38%) as can be seen on the map below (Figure 1).

Figure 1: Distribution of sugar crop production in the United States

From the 1970s to the early 2000s, sugar factories became essentially the property of producers, grouped into cooperatives2. Aside from this movement of vertical integration controlled by farmers, the two US sugar sectors have not undergone any major changes since the reform of the 1981 Farm Bill, which lays the foundation for the current regulatory framework3. Since then, institutional stability has been in place, apart from a few changes to deal with the consequences of NAFTA – the North American trade agreement – and imports from Mexico that have gradually become royalty-free after a period of adjustment. years.

Having established the objective of covering 85% of their domestic sugar consumption, the two US sugar sectors are not in the situation of cereals and oilseed crops for which, as exporters, they are directly dependent on the volatility of international courses. This explains in particular why beet and cane surfaces are not concerned by counter-cyclical aid programs as for most other crops.

The American sugar policy is based on four pillars:

- A minimum sugar price via the repayable loan mechanism in kind (non recourse loan)

- Production quotas allocated to processors to control supply

- Import quotas and disincentive customs duties

- Two systems of release: one for the transformation of sugar into ethanol, the other for the re-export of refined sugar on the American territory.

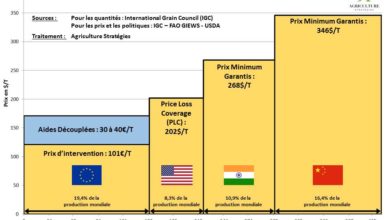

Minimum prices are set at $ 413 / t for raw cane sugar and $ 531 / t for refined beet sugar4, which is a price level rarely achieved by international trade quotations. Production quotas are distributed annually to processors and can not be less than 85% of US consumption. If the sugar factories exceed their quota, they must sell this surplus to another processor, store it at their expense or possibly export it.

The United States has a very responsive import protection system. Excluding the import quota, customs duties are prohibitive and amount to $ 338 / t for raw sugar and $ 357 / t for refined sugar. Import quotas have a low tariff (about $ 15 / t) and can be adjusted during the year based on US production prospects and imports from Mexico. The level of import quotas, however, can not fall below the US commitments to the WTO is 1.539 million tonnes.

Mexican production is thus followed with the greatest attention since import flows from this country constitute one of the main variables that were beyond the control of the regulator5. The rise of sugar production in Mexico motivated the US Congress in 2008 to allow the USDA to resell sugar stocks to biofuel processors in the event of market congestion, in addition to public which remains activable.

But it is especially from 2013 when the spirit of NAFTA and the free access to the American market began to be questioned. That year, Mexican exports peaked at 1.8 million tonnes, driving down prices until the feedstock flexibility program was activated6.

Negotiations between the two parties then led to the imposition of a revised export quota for Mexico each year to ensure a balanced US market. In addition, a system of minimum exit prices was established in Mexico following a dumping investigation, for a minimum price of $ 573 / t for refined sugar7. In 2017, adjustments were made to this agreement, the Mexican minimum prices were slightly raised, the portion of refined sugar in the Mexican annual quota increased from 53% to 30%8 and finally Mexico has a priority over access to additional imports granted during the year.

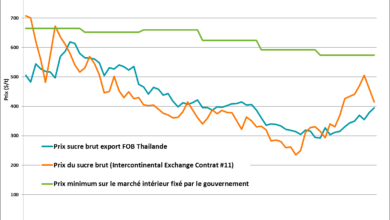

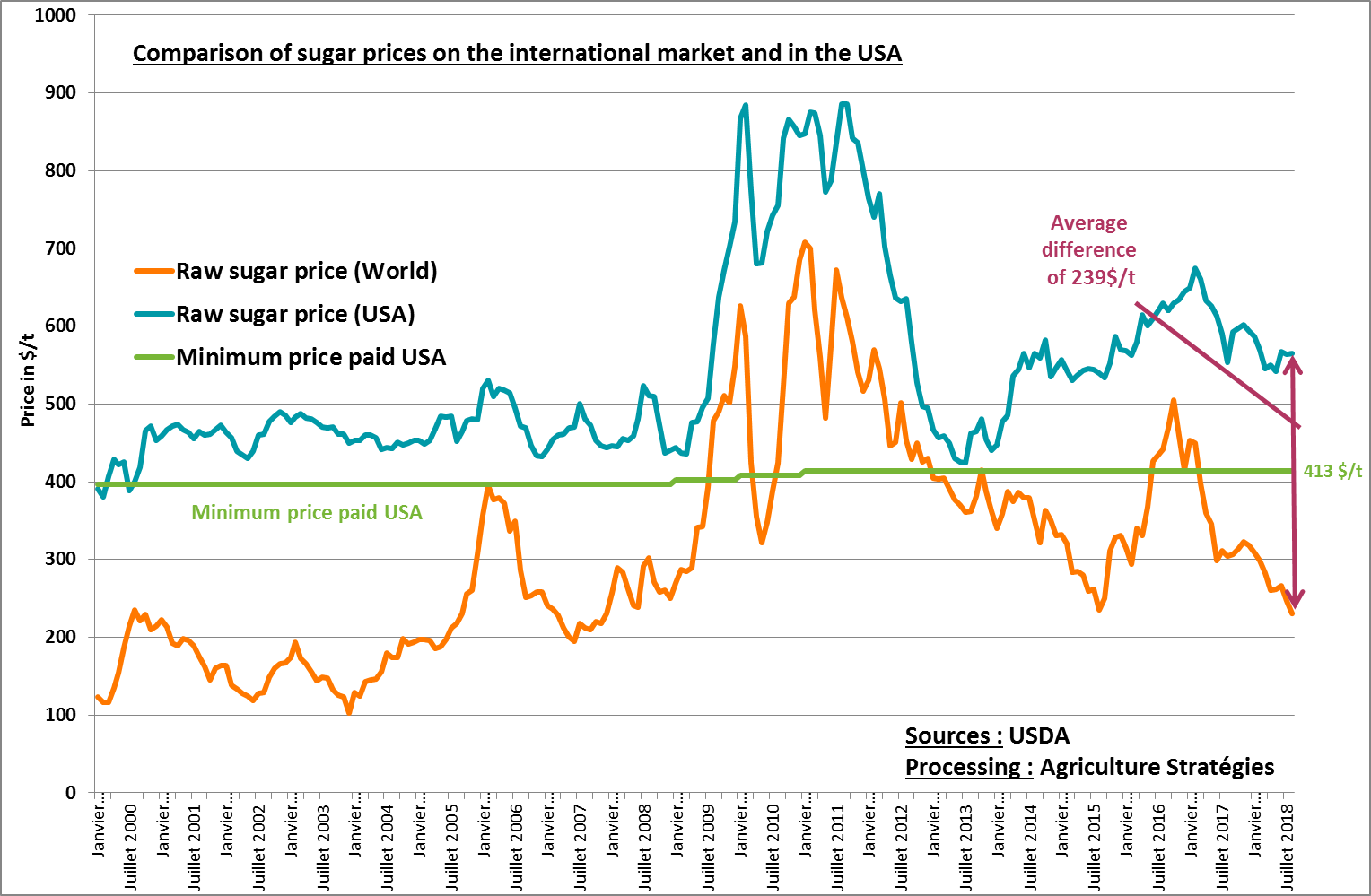

Figure 2: Evolution of sugar prices on the international market and in the USA

The evolution of domestic and international prices since 2000 (Figure 2) tends to show that these different tools are used effectively to ensure the equilibrium of supply and allow domestic prices to be above the minimum price. At more than $ 500 per tonne of raw sugar, US industries remain protected from the crisis of overproduction that currently affects international markets. On average since 2000, domestic prices in the United States were 66% higher than international prices, a differential of $ 239 / t. The control of Mexican imports also shows the American pragmatism in trade: included among the sensitive topics of NAFTA, an agreement was reached as of mid-2017, well before the announcement of a new agreement United States – Mexico in August 2018.

Christopher Gaudoin, Strategic analyst for Agriculture Strategies

2 https://americansugarbeet.org/who-we-are/sugarbeet-history/

3 https://opensiuc.lib.siu.edu/cgi/viewcontent.cgi?article=1944&context=gs_rp

4 https://www.ers.usda.gov/topics/crops/sugar-sweeteners/policy.aspx#price

5 Cf. USDA’s monthly reports https://www.ers.usda.gov/webdocs/publications/90150/sss-m-361.pdf?v=5178.8

6 https://www.ers.usda.gov/webdocs/publications/74632/60121_sssm-335-01.pdf?v=42593

7 https://enforcement.trade.gov/download/factsheets/factsheet-mexico-sugar-suspension-agreement-ad-cvd-121914.pdf

8 https://www.commerce.gov/news/press-releases/2017/06/us-and-mexico-strike-deal-sugar-protect-us-growers-and-refiners-ensure