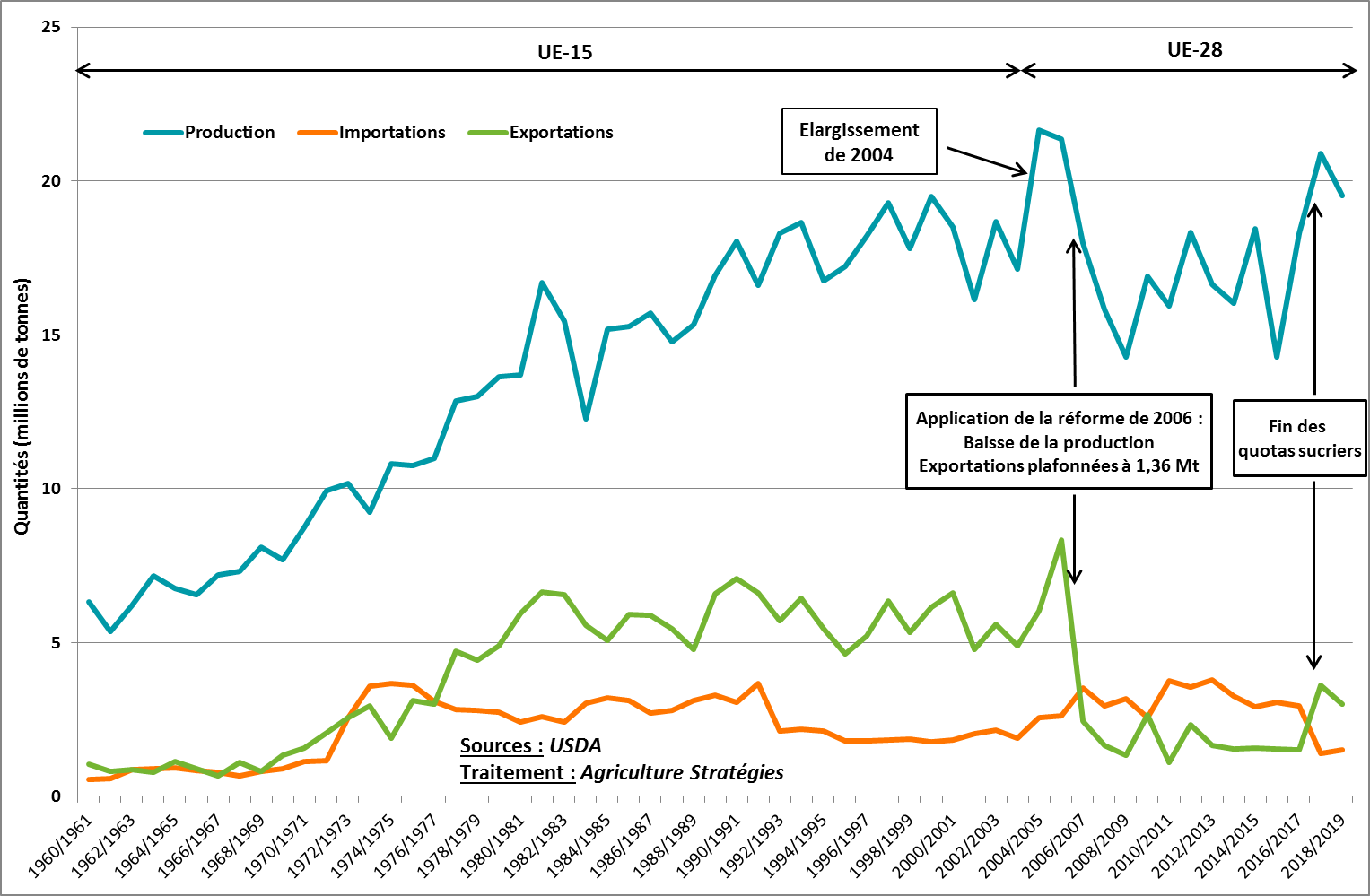

The abolition of the European sugar quota regime in 2017 did not have the expected results. The prospect of increasing European production to develop exports quickly turned into a drop in sugar prices and tensions in the governance of the sector, particularly in France. Heavy industry par excellence considering the transformation process, where the perishability and the heavy nature of the raw material explain the strong dependence between the links of the production and the first transformation, this sector also does not have important margins of maneuver to build a strategy of upmarket and “decommoditization”.

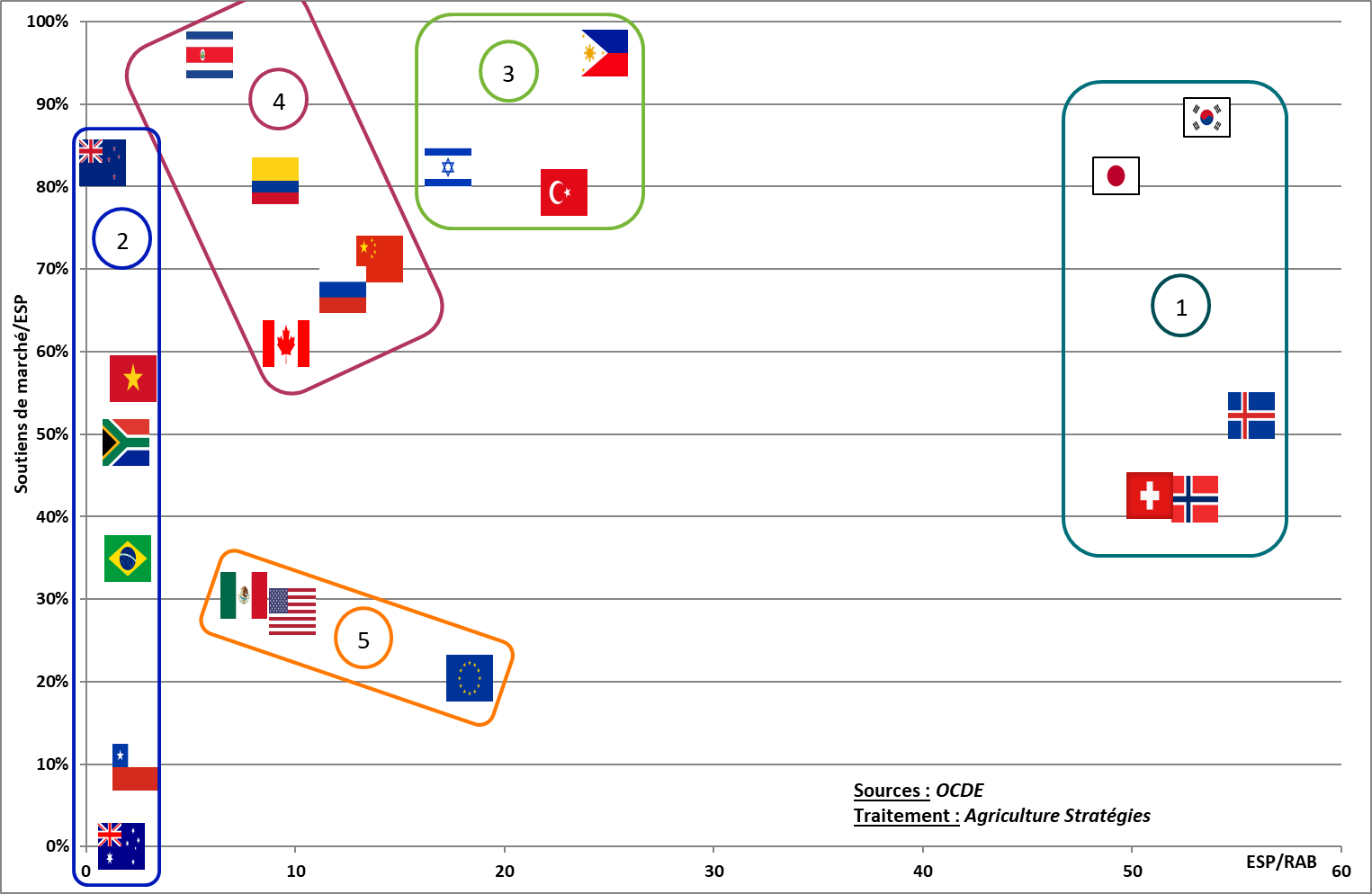

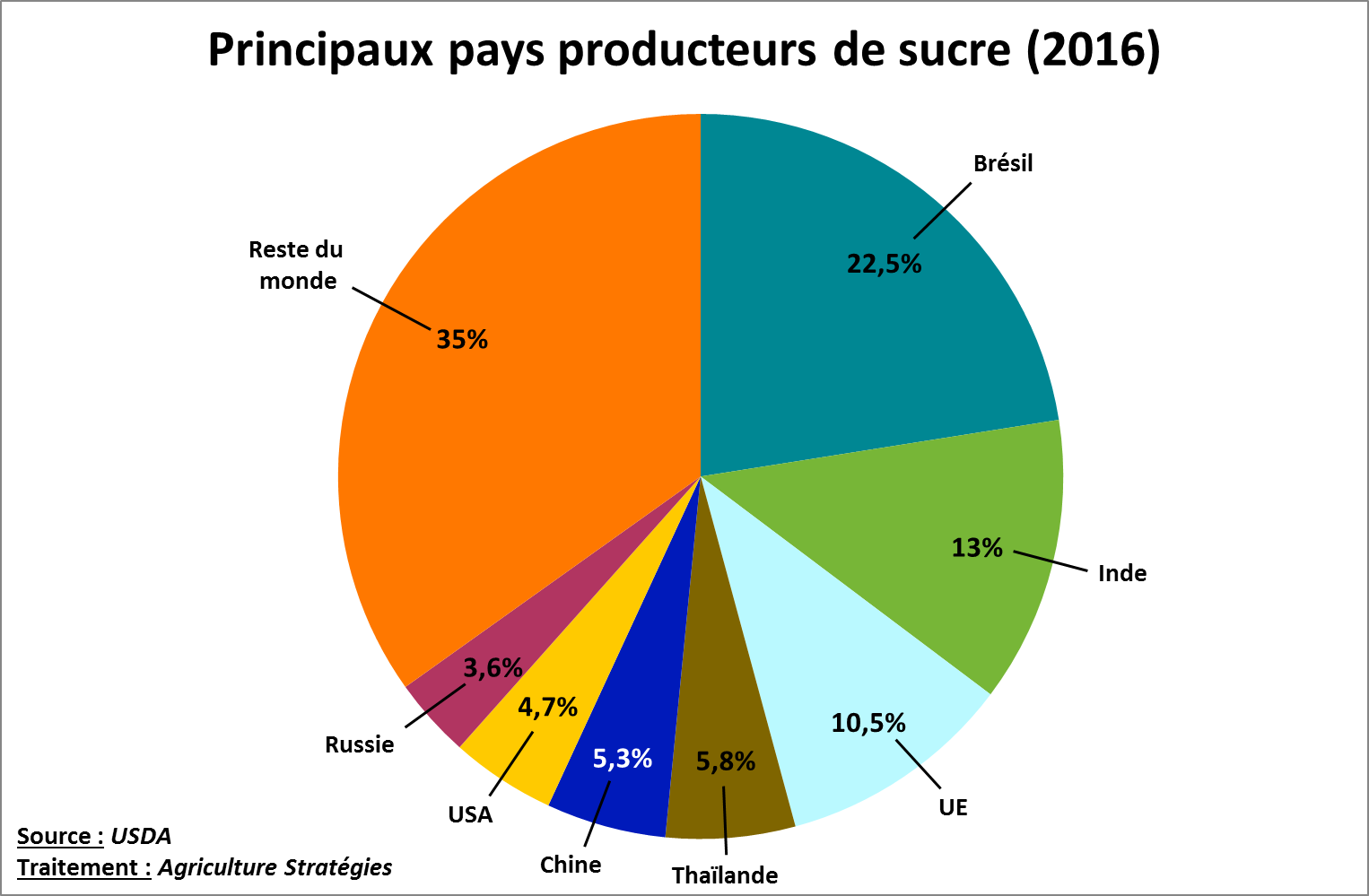

In these conditions, the exposure to the volatility of international markets, where the surpluses of the main producers are mainly exchanged, can undermine the entire sector because of a lack of strong public policy. In order to envisage a new regulatory framework for European sugar production, we propose a series of articles to study the different sugar policies of the main sugar producers. We will focus on Brazil, India, Thailand, China, the United States and Russia, which together with the European Union account for nearly two-thirds of world production (see Figure below). ). This panorama will allow us to conclude this series by constructing different scenarios of evolution of the European sugar policy.

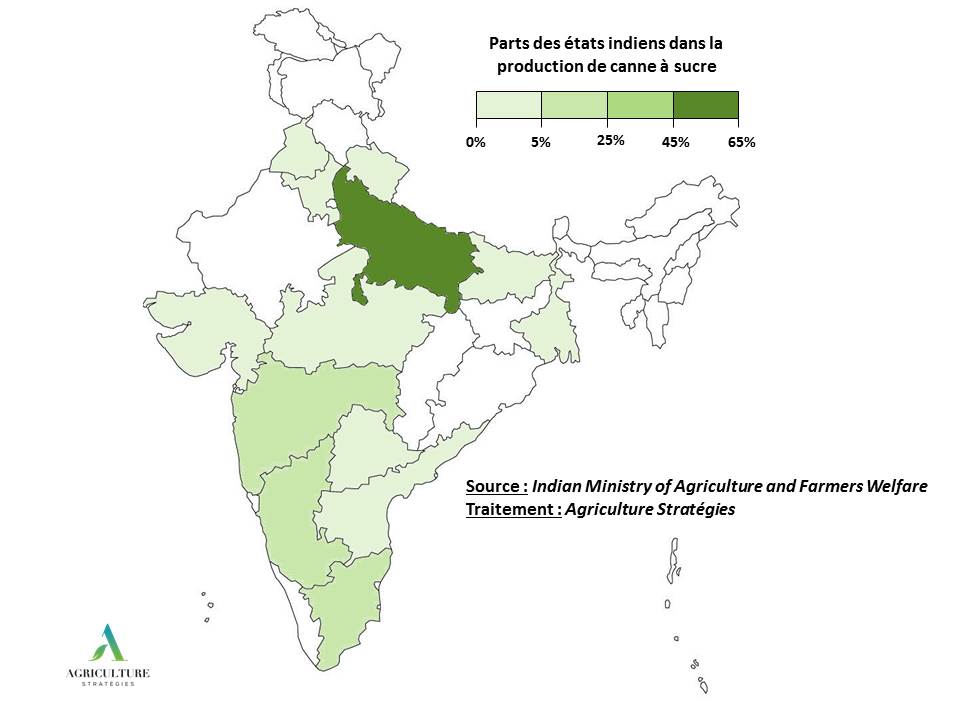

India is currently the world’s second-largest sugar producer with about 22 million tonnes or 13% of world production in 2016. This production comes from sugar cane, whose production is found throughout the country, but whose heart is located mainly in the state of Uttar Pradesh in northern India (46% of national production in 2016) (Figure 1). Commercial relations between farmers and sugar factories are highly regulated: producers are attached to a processing plant which is obliged to buy their cane at a minimum price set by the public authorities. In addition, the government regulates the opening of new sugar mills that can not be located less than 15km from an existing processing site.

Figure 1: Distribution of sugar cane production in India

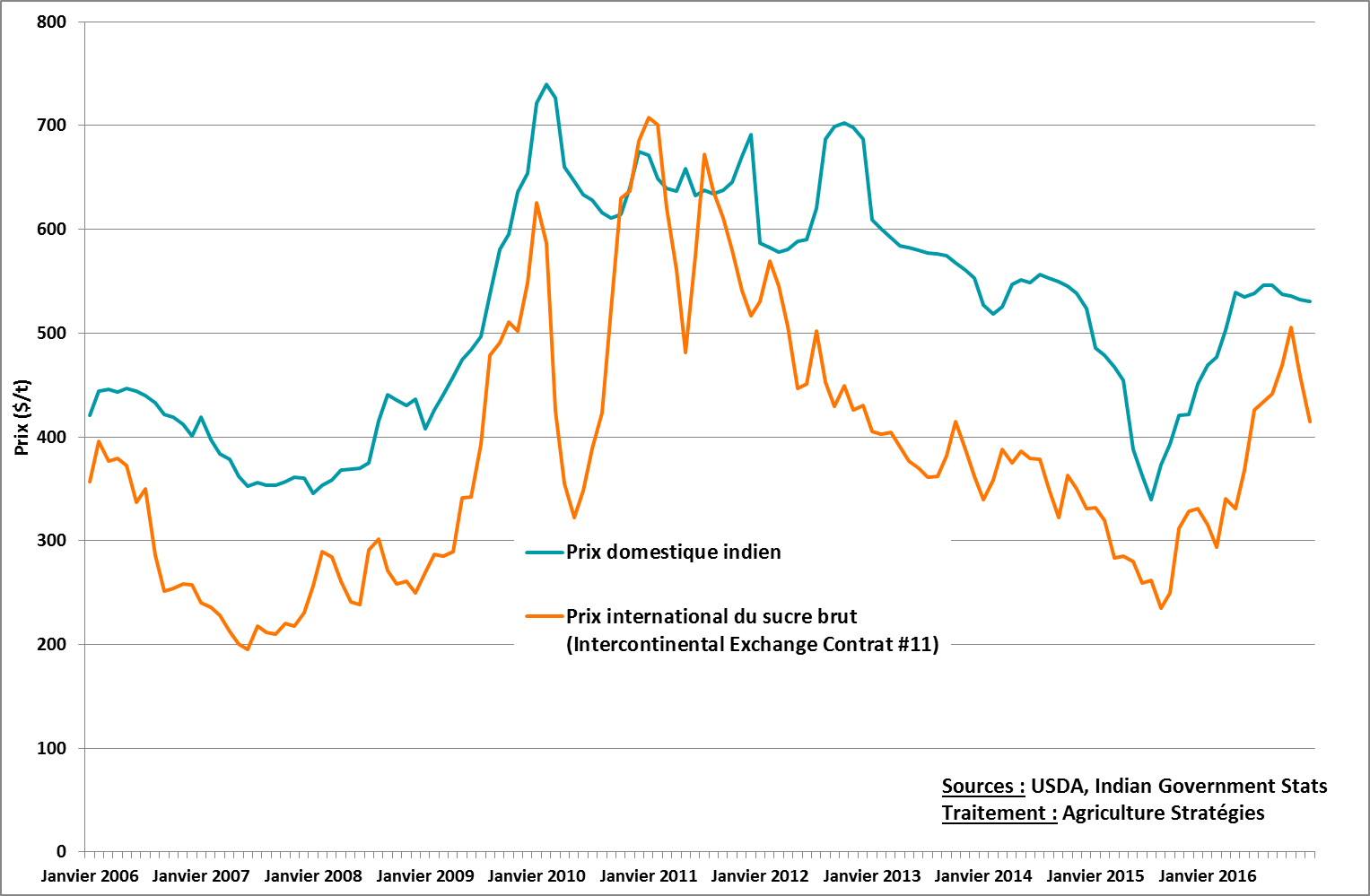

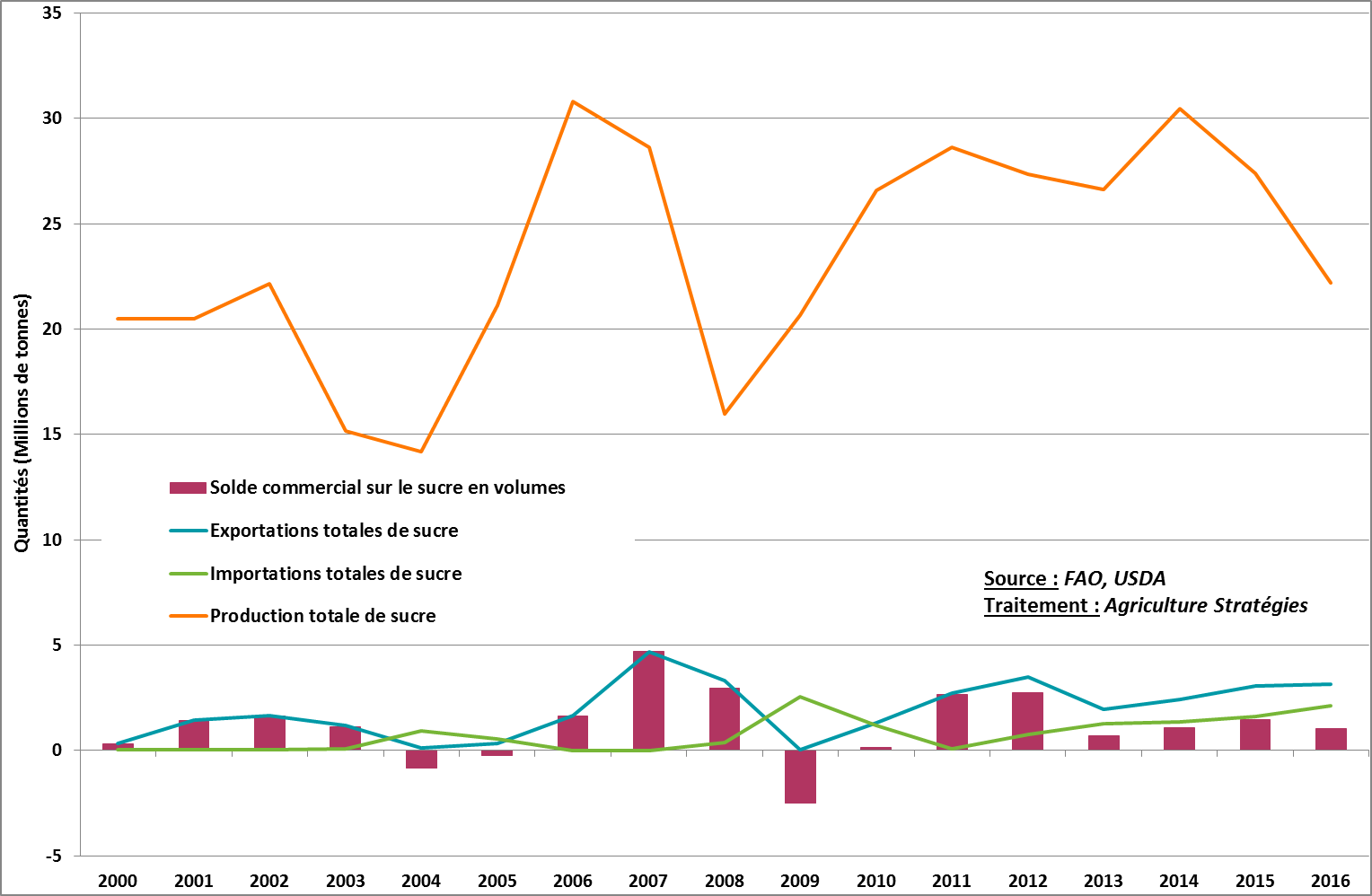

The sugar sector in India remained relatively marginal (less than 5% of world production) until the mid-1990s when production increased significantly. The variations in production are very strong and India has been oscillating for more than 25 years between the status of exporter and that of sugar importer. These import requirements in 2009 and 2010 had largely contributed to the rise in international prices. Since then, it has remained a net exporter (exporting more than it imports) and exported 3.2 million tonnes of sugar in 2016 (4.7% of world exports) (Figure 2).

Figure 2: India’s Imports, Exports and Trade Balance on Refined Sugar

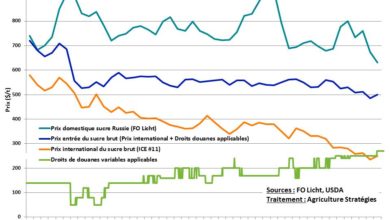

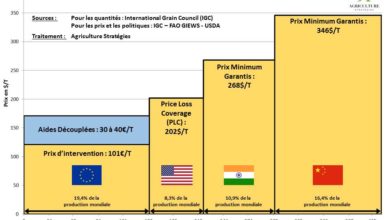

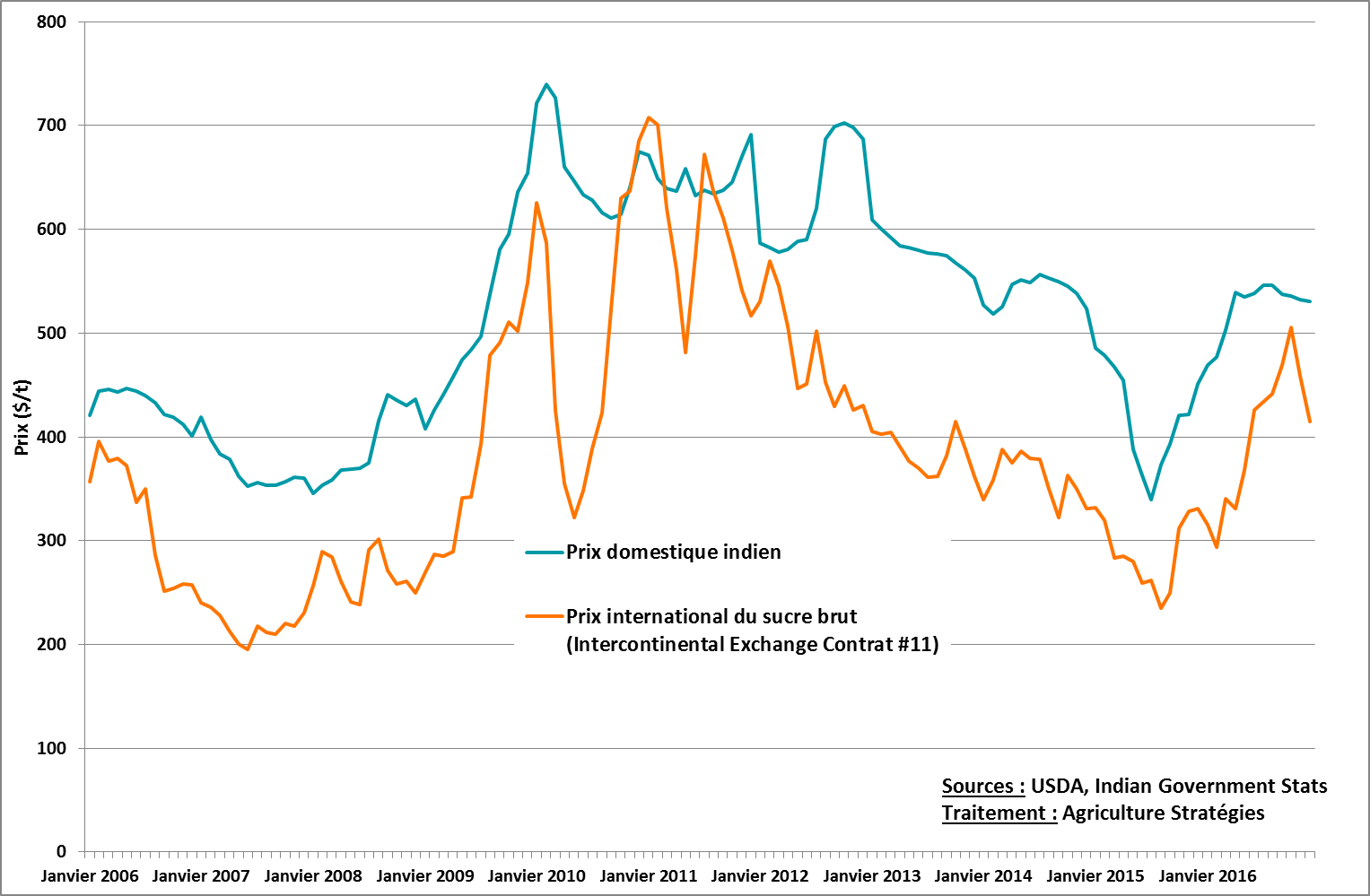

India’s agricultural policy has regulated sugar production since 1966 and the “Sugarcane Control Order” still in place today. This policy establishes a sugar cane pricing system governed by both the federal government and the governments of each state. A minimum price per state is also introduced, it is generally higher than the federal price: in the main cane producing region (Uttar Pradesh) this price was $ 41 / t against $ 34 / t at the federal level.

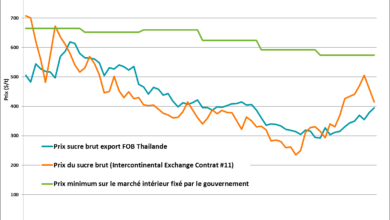

Figure 3: Sugar prices in India, domestic and international markets

Historically, processors also had constraints on their sugar sales. Part of the output (10% in 2012, but sometimes much more) was to be sold to the government at prices well below market prices in order to be redistributed to people living below the poverty line. Since 2013, these provisions have been abolished and processors can now freely sell their products on the domestic market. For its food aid program, the government buys sugar directly, which it wants to redistribute to the poorest at lower prices. These purchases of sugar by the government concerned more than 4 million tons in 2013, which gives the public authorities a certain power of orientation on the evolution of the domestic market.

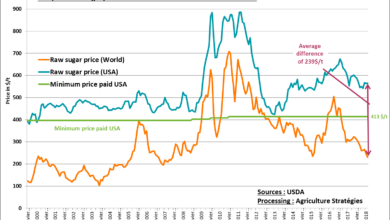

In order to stabilize its domestic market, India uses different levers. Average tariffs of 40% are applied on sugar. In case of deficit production, they can be reduced to zero (this was the case in the late 1990s and in 2008-2009), just as they can be increased in case of overproduction as early as 2018 when they were raised to 100 % to cope with falling prices.

To relieve its domestic market during the 2013/2014 and 2014/2015 marketing years, export subsidies were also used before being replaced by minimum export quotas imposed on processors from the 2015/2016 marketing year. . These quotas represent a very significant part of Indian exports.

All of these measures place a heavy burden on Indian processors. The latter ended up accumulating significant delays in payments to farmers (more than $ 3 billion cumulated in 2015). To remedy this, the government launched a plan in 2015 allowing processors to borrow at zero interest rates from banks (the government taking charge of the interest) which has since helped to repay a little more than half of late payments.[1].

By moving into a net exporter status, the Indian government has embarked on reorientations to diversify its domestic market opportunities. The production of renewable energy (ethanol, electricity) from biomass is promoted by the government, one of whose objectives is to support the sugar sector, as recently stated by the Minister of Petroleum: “We want our Sugar producers get support and the sugar industries are stabilized “)[2].

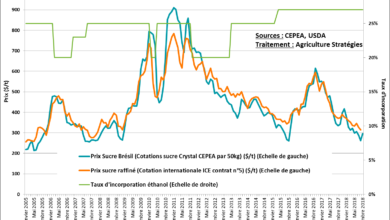

In 2009, the government set itself the target of having a compulsory ethanol incorporation rate of 20% for ethanol in 2017. In addition, a regulated price system for ethanol has been in place since 2014 to encourage to the consumption of this fuel. The incorporation target, far from being achieved with only 3.3% in 2016, has been renewed by 2030. To claim to reach it, producers have been allowed since 2018 to use cane juice directly whereas previously only the use of molasses was allowed. Investment in cogeneration structures from bagasses (the rest of the canes once the juice has been extracted) is also encouraged by the government.

Like other countries, India is seeking non-food valuations to find new markets and better manage its internal market without resorting to destabilizing measures for international trade. This new direction, if successful, will no doubt allow it to respond to Australia, which began WTO proceedings in November 2018 to denounce the effects of India’s sugar policy on international trade.[3].

[1] https://sugaralliance.org/wp-content/uploads/2013/10/Meriot-India-8-16.pdf

[2] https://www.theweek.in/news/biz-tech/2018/09/22/why-india-biofuel-policy-wont-work.html

[3] https://www.wto.org/english/news_e/news18_e/agri_26nov18_e.htm